1970s: overwhelmed with vertical integration and self-sufficiency

1980s: appreciation of the yen (1985 Plaza Accord)

1990s: collapse of the Bubble (1991), relocation of production to Asia, three excesses:

debt

facility

employment

2000s: lost 20 years

Going forward, Japan has the option of growth under new business models, or continue to stagnate with matured industries

While there is dramatic global market expansion in many business areas in the global electrical industry, e.g. for Lithium Ion Batteries, DVDs, Car navigation units, DRAM, Japan’s market shares are falling in most sectors. For example, Japanese market shares for LCD, DVD players, Lithium Ion batteries, or car navigation units have fallen from almost 100% global market share 5-10 years ago to 10%-20% today.

Restructuring mature industry can generate more economic benefit than innovating a new industry:

large established market, although low growth

reduced number of players in the market following consolidation

Revitalization of JVCKENWOOD

the current main business as the core – not new business

speed, like “fresh food”

eliminate hidden waste and loss costs

eliminate vested rights

Kenwood in 2002 was in a disastrous condition:

net income (loss): YEN -27 Billion (= US$ -270 million) losses

debt: YEN 110 Billion (= US$ 1.1 billion)

accumulated losses: YEN 45 Billion (= US$ 450 million)

net worth: YEN -17 Billion (= US$ -170 million)

Restructuring by March 2003:

Financial restructuring: Dept/equity swap. Moved from YEN 17 billion negative net worth to positive within 6 months

Business restructuring: focus on core business. Terminated cellular phone business.

Management restructuring: management consolidation. Eliminate huge wastes and losses in subsidiaries.

Restructuring in FY2003 achieved a V-shape recovery. Net income margin was improved from -8% in FY3/2002 to 2%-4% in recent years.

In mature markets, growth is achieved through M&A, reducing the number of players in the market. As the top player in the market, profitable growth improved:

Main four players in the car electronics after-market before Kenwood-JVC merger:

Pioneer

Kenwood

Sony

JVC

after the JVCKENWOOD merger, and restructure to minimize losses from the TV business:

JVCKENWOOD

…

…

JVC and KENWOOD formed a capital and business alliance in July 2007, followed by management integration in October 2008, and a full merger in October 2011. The business portfolio was restructured, and in particular big losses in the TV business were reduced. Fixed costs were reduced by 40% by selling off assets, reduction of production and sales sites, and 25% voluntary retirement.

This structural reform was completed in the FY3/2001, and led to another V-shaped recovery, and to profitable growth under the new medium term business plan.

The JVC-KENWOOD merger led to big jumps in market share in many markets, and thus to very much improved profitability.

How can Japan become competitive again?

Why did Japan’s mass production type electronics fail? Answer: Japanese management failed to deal with globalization and digitalization.

Other factors that contributed to Japan’s failure are vertical integration, technology leakage from exporting production facilities, insufficient added value compared to the high Japanese labor costs, and lack of money for investment, because Japanese companies largely relied on bank loans instead of equity.

Japan’s heavy electrical industry on the other hand is competitive – why?

Creative know-how in the heavy electrical industry is in human brains, therefore more difficult to leak to competitors under Japan’s employment circumstances.

huge capital investment is needed, and almost fully depreciated in Japan. Therefore the depreciation costs exceeds HR costs.

How can Japan become competitive again?

Japan needs to accelerate growth strategies in those areas, where Japan has competitive advantage, and where Japanese industries can differentiate themselves. Examples are industrial areas which depend on a long-term improvements and advanced technologies, and techniques of craftsmen, and in next generation technologies.

JVC KENWOOD takes action to innovate

JVCKENWOOD invested in a venture capital fund: the WiL Fund I, LP to reinforce alliances with potential ventures in Japan and overseas

JVCKENWOOD invested in ZMP Inc. to promote car telematics and car auto-control

Haruo Kawahara, Chairman of JVCKenwoodHaruo Kawahara, Chairman of JVCKenwood

Professor Kurokawa set the stage by describing the uncertain times, risks and unpredictabilities in which we live – while at the same time internet connects us all, all while the world’s population increased from about 1 billion people in 1750 to about 9 billion people today.

Major global risks in terms of impact and likelihood are (General Annual Conference 2013 of the World Economic Forum):

severe income disparity

chronic fiscal imbalances

rising greenhouse gas emissions

cyber attacks

water supply crisis

management of population aging

corruption

Top trends for 2014, ranked by global significance (World Economic Forum, Outlook on global agenda 2014):

rising social tensions in Middle East and North Africa

widening income disparity

persistent structural unemployment

intensifying cyber threats

diminishing confidence in economic policies

lack of values in leadership

the expanding middle class in Asia

This changing world needs a change of paradigm:

resilience instead of strength

risk instead of safety

Many recent “Black Swan events” bring home that:

accident happens

machine breaks

to err is human

Fukushima Nuclear Accident Investigation Commission NAIIC of the Japanese Parliament:

Professor Kiyoshi Kurokawa chaired the Fukushima Nuclear Accident Independent Investigation Commission (NAIIC) by the National Diet of Japan, which was active from December 8, 2011 to July 5, 2012. While Parliamentary commissions to investigate accidents, problems and disasters are quite frequent in most Western democracies, this was the first time ever in the history of Constitutional Democratic Japan, that a Parliamentary investigation commission was constituted.

Examples of Parliamentary commissions in other western democracies are:

Three Mile Island, USA 1979

Space Shuttle Challenger, USA 1986

9.11 Terrorist Attack, USA 2001 and many many many more in USA

Oslo’s shooting incident, Norway 2011

Mad Cow Disease, UK 1997-, and several Parliamentary commissions every year in UK

Fukushima Nuclear Accident Investigation Commission of the Japanese Parliament NAIIC key results: Fukushima nuclear disaster was caused by “regulatory capture”

The key result of the Parliamentary Commission is, that the Fukushima nuclear disaster was caused by “regulatory capture”, a phenomenon for which there are many examples all over the world and which is not specific to Japan. Regulatory capture was studied by Goerge J Stigler, who was awarded the Nobel Prize in 1982 for “for his seminal studies of industrial structures, functioning of markets and causes and effects of public regulation”.

Since the full report of the Independent Parliamentary Commission NAIIC is long and complex to read, few people are likely to read the full reports and watch the videos of all sessions.

Therefore short summary videos the key results of the Independent Parliamentary Commission NAIIC were prepared both in Japanese and in English.

The simplest explanation of The National Diet of Japan Fukushima Nuclear Accident Independent Investigation Commission NAIIC Report (English):

1. What is the NAIIC?

2. Was the nuclear accident preventable?

3. What happened inside the nuclear plant?

4. What should have been done after the accident?

5. Could the damage be contained?

6. What are the issues with nuclear energy?

わかりやすいプロジェクト 国会事故調編

1。国会事故調ってなに?

2。事故は防げなかったの?

3。原発の中でなにが起こっていたの?

4。事故の後対応をどうしたらよかったの?

5。被害を小さくとどめられなかったの?

6。原発をめぐる社会の仕組みの課題ってなに?

“Groupthink can kill”

We need leaders to be accountable, and we need to understand that “Groupthink” can lead to disasters.

We need the obligation to dissent instead of compliance.

The Nuclear Accident Independent Investigation Commission (NAIIC) was like a hole body CT scan of the Governance of Japan.

Richard Feynman when charing the Space Shuttle Accident investigation wrote in 1986: “for a successful technology, reality must take precedence over public relations, for nature cannot be fooled.

For his work chairing the Nuclear Accident Independent Investigation Commission (NAIIC) Professor Kurokawa was selected as one of “100 Top Global Thinkers 2012” by Foreign Policy “for daring to tell a complacent country that groupthink can kill”.

Professor Kurokawa was awarded the AAAS Scientific Freedom and Responsibility Award “for his courage in challenging some of the most ingrained conventions of Japanese governance and society.

“Japan is clearly living in denial, water keeps building up inside the plant, and debris keeps piling up outside of it. This is all just one big shell game aimed at pushing off the problem until the future”, New York Times, quotation of the day, September 4, 2013 Professor Kiyoshi Kurokawa

Professor Kiyoshi KurokawaProfessor Kiyoshi Kurokawa

(Gerhard Fasol, CEO of Eurotechnology Japan KK. Served as Associate Professor of Tokyo University, Lecturer at Cambridge University, and Manger of Hitachi Cambridge R&D Lab.)

Ludwig Boltzmann’s greatest contribution to science is that he linked the macroscopic definition of Entropy which came from optimizing steam engines at the source of the first industrial revolution to the microscopic motion of atoms or molecules in gases, this achievement is summarized by the equation S = k log W, linking entropy S with the probability W. k is the Boltzmann constant, one of the most important constants in nature, linked directly to temperature in the SI system of physical units. This monumental work is maybe Boltzmann’s most important creation but by far not the only one. He discovered many laws, and created many mathematical tools, for example Boltzmann’s Equations, which are used today as tools for numerical simulations of gas flow for the construction of jet engines, airplanes, automobiles, in semiconductor physics, information technology and many other areas. Although independently discovered, Shannon’s theory of noise in communication networks, and Shannon’s entropy in IT is also directly related to Boltzmann’s entropy work.

Ludwig Boltzmann, the leader

Ludwig Boltzmann was not only a monumental scientist, but also an exceptional leader, teacher, educator and promoter of exceptional talent, and he promoted many women.

One of the women Ludwig Boltzmann promoted was Henriette von Aigentler, who was refused permission to unofficially audit lectures at Graz University. Ludwig Boltzmann advised and helped her to appeal this decision, in 1874, Henriette von Aigentler passed her exams as a high-school teacher, and on July 17, 1876, Ludwig Boltzmann married Henriette von Aigentler, my great-grand mother.

Another woman Ludwig Boltzmann promoted was his student Lise Meitner (Nov 1878 – Oct 27, 1968), who later was part of the team that discovered nuclear fission, work for which Otto Hahn was awarded the Nobel Prize. Lise Meitner was also the second woman to earn a Doctorate degree in Physics from the University of Vienna. Element 109, Meitnerium, is named after Lise Meitner.

Nagaoka Hantaro, First President of the University of Osaka – Ludwig Boltzmann’s pupil

The first President of Osaka University (1931-1934), Nagaoka Hantaro (1865 – 1950) was Ludwig Boltzmann’s pupil around 1892 – 1893 at Muenchen University.

Ludwig Boltzmann, a leader of science

Ludwig Boltzmann was connected in intense discussions with all major scientists of his time, he travelled extensively including three trips to the USA in 1899, 1904 and 1905, about which he wrote the article “Die Reise eines deutschen Professors ins El Dorado”, published in the book “Populäre Schriften”.

Ludwig Boltzmann published his first scientific publication at the age of 21 years in 1865. He was appointed Full Professor of Mathematical Physics at the University of Graz in 1869 at the age of 25 years, later in 1887-1888 he was Rektor (President) of the University of Graz at the age of 43 years.

He spent periods of his professional work in Vienna, at Graz University (1869-1873 and 1876-1890), at Muenchen University (1890-1894). When working at Muenchen University, he discovered that neither he nor his family would not receive any pension from his employment at Muenchen University after an eventual retirement or in case he dies before retirement, and therefore decided to return to Vienna University in 1894, where he and his family were assured of an appropriate pension. During 1900-1902 he spent two years working in Leipzig, where he cooperated with the Nobel Prize winner Friedrich Wilhelm Ostwald.

Ludwig Boltzmann did not shy away from forceful arguments to argue for his thoughts and conclusions, even if his conclusions were opposite to the views of established colleagues, or when he felt that philosophers intruded into the field of physics, i.e. used methods of philosophy to attempt solving questions which needed to be solved with physics measurements, e.g. to determine whether our space is curved or not. Later in his life he was therefore also appointed to a parallel Chair in Philosophy of Science, and Ludwig Boltzmann’s work in Philosophy of Science is also very fundamentally important.

I discovered the unpublished manuscripts of Boltzmann’s lectures on the Philosophy of Science, stimulated and encouraged by myself, and with painstaking work my mother transcribed these and other unpublished manuscripts, and prepared them for publication, to make these works finally accessible to the world, many years after Ludwig Boltzmann’s death.

Ludwig Boltzmann was a down to earth man. He rejected the offer of Nobility by His Majesty, The Emperor of Austria, i.e. the privilege to be named Ludwig von Boltzmann (or a higher title) instead of commoner Ludwig Boltzmann. Ludwig Boltzmann said: “if our common name was good enough for my parents and ancestors, it will be good enough for my children and grand children…”

Summary: understanding Ludwig Boltzmann.

Boltzmann’s thoughts and ideas are a big part of our understanding of the world and the universe.

His mathematical tools are used every day by today’s engineers, bankers, IT people, physicists, chemists… and even may contribute to solve the world’s energy problems.

Ludwig Boltzmann stood up for his ideas and conclusions and did not give in to authority. He rejected authority for authority’s sake, and strongly pushed his convictions forward.

What can we learn from Ludwig Boltzmann?

empower young people, recognize and support talent early.

exceptional talent is not linear but exponential.

move around the world. Connect. Interact.

empower women.

don’t accept authority for authority’s sake.

science/physics/nature need to be treated with the methods of physics/science.

Boltzmann constant k, “What is temperature?” and the new definition of the SI system of physical units

(by Gerhard Fasol, CEO of Eurotechnology Japan KK. Served as Associate Professor of Tokyo University, Lecturer at Cambridge University, and Manger of Hitachi Cambridge R&D Lab.)

(in preparing this talk, I am very grateful for several email discussions and telephone conversations, and for unpublished presentations and documents, to Dr Michael de Podesta MBE CPhys MInstP, Principal Research Scientist at the National Physical Laboratory NPL in Teddington, UK, who has greatly assisted me in understanding the current status of work on reforming the SI system of units, and also his very important work on high-precision measurements of Boltzmann’s constant. Dr Michael de Podesta’s measurements of Boltzmann’s constant are arguable among the most precise, of not the most precise measurements of Boltzmann’s constant today, and therefore a very important contribution to our system of physical units).

Boltzmann constant k, the definition of the unit of temperature and energy

Temperature is one of the physics quantities we use most, and understanding all aspects of temperature is at the core of Ludwig Boltzmann’s work. People measured temperature long before anyone knew what temperature really is: temperature is a measurement of the average kinetic energy of the atoms of a substance. When we touch a body to “feel” its temperature, what we are really doing is to measure the “buzz”, the thermal vibrations of the atoms making up that body.

For an ideal gas, the kinetic energy per molecule is equal to 3/2 k.T, where k is Boltzmann’s constant. Therefore Boltzmann’s constant directly links energy and Temperature.

However, when we measure “Temperature” in real life, we are not really measuring the true thermodynamic temperature, what we are really measuring is T90, a temperature scale ITS-90 defined in 1990, which is anchored by the definition of temperature units in the System International, the SI system of defining a set of fundamental physical units. Our base units are of fundamental importance for example to transfer semiconductor production processes around the world. For example, when a semiconductor production process requires a temperature of 769.3 Kelvin or mass of 1.0000 Kilogram, then accurate definition and methods of measurement are necessary to achieve precisely the same temperature or mass in different laboratories or factories around the world.

second: The second is the duration of 9 192 631 770 periods of the radiation corresponding to the transition between the two hyperfine levels of the ground state of the cesium 133 atom.

metre: The meter is the length of the path travelled by light in vacuum during a time interval of 1/299 792 458 of a second.

kilogram: The kilogram is the unit of mass; it is equal to the mass of the international prototype of the kilogram.

Ampere: The ampere is that constant current which, if maintained in two straight parallel conductors of infinite length, of negligible circular cross-section, and placed 1 meter apart in vacuum, would produce between these conductors a force equal to 2 x 10-7 newton per meter of length.

Kelvin: The kelvin, unit of thermodynamic temperature, is the fraction 1/273.16 of the thermodynamic temperature of the triple point of water.

mole:

The mole is the amount of substance of a system which contains as many elementary entities as there are atoms in 0.012 kilogram of carbon 12

When the mole is used, the elementary entities must be specified and may be atoms, molecules, ions, electrons, other particles, or specified groups of such particles.

candela: The candela is the luminous intensity, in a given direction, of a source that emits monochromatic radiation of frequency 540 x 1012 hertz and that has a radiant intensity in that direction of 1/683 watt per steradian.

The definitions of base units has long history, and are evolving over time. Today several of the definitions are particularly problematic, among the most problematic are temperature and mass.

SI base units are closely linked to fundamental constants:

second:

metre: linked to c = speed of light in vacuum

kilogram: linked to h = Planck constant.

Ampere: linked to e = elementary charge (charge of an electron)

Kelvin: linked to k = Boltzmann constnt

mole: linked to N = Avogadro constant

candela:

Switch to a new framework for the SI base units:

Each fundamental constant Q is a product of a number {Q} and a base unit [Q]:

Q = {Q} x [Q],

for example Boltzmann’s constant is:

k = 1.380650 x 10-23 JK-1.

Thus we have two ways to define the SI system of SI base units:

we can fix the units [Q], and then measure the numerical values {Q} of fundamental constants in terms of these units (method valid today to define the SI system)

we can fix the numbers {Q} of fundamental constants, and then define the units [Q] thus that the fundamental constants have the numerical values {Q} (future method of defining the SI system)

Over the next few years the SI system of units will be switched from the today’s method (1.) where units are fixed and numerical values of fundamental constants are “variable”, i.e. determined experimentally, to the new method (2.) where the numerical values of the set of fundamental constants is fixed, and the units are defined such, that their definition results in the fixed numerical values of the set of fundamental constants. This switch to a new definition of the SI system requires international agreements, and decisions by international organizations, and this process is expected to be completed by 2018.

Today’s method (1.) above is problematic: The SI unit of temperature, Kelvin is defined as the fraction 1/273.16 of the thermodynamic temperature at the triple point of water. The problem is that the triple point depends on many factors including pressure, and the precise composition of water, in terms of isotopes and impurities. In the current definition the water to be used is determined as “VSNOW” = Vienna Standard Mean Ocean Water. Of course this is highly problematic, and the new method (2.) will not depend on VSNOW any longer.

In the new system (2.) the Kelvin will be defined as:

Kelvin is defined such, that the numerical value of the Boltzmann constant k is equal to exactly 1.380650 x 10-23 JK-1.

Measurement of the Boltzmann constant k:

In order to link the soon to be fixed numerical value of Boltzmann’s constant to currently valid definitions of the Kelvin, and in particular to determine the precision and errors, it is necessary to measure the value of Boltzmann’s current in terms of today’s units as accurately as possible, and also to understand and estimate all errors in the measurement. Several measurements of Boltzmann’s constants are being performed in laboratories around the world, particularly at several European and US laboratories. Arguably today’s best measurement has been performed by Dr Michael de Podesta MBE CPhys MInstP, Principal Research Scientist at the National Physical Laboratory NPL in Teddington, UK, who has kindly discussed his measurements and today’s status of the work on the system of SI units and its redefinition with me, and has greatly assisted in the preparation of this article. Dr Podesta’s measurements of Boltzmann’s constant have been published in:

Michael de Podesta et al. “A low-uncertainty measurement of the Boltzmann constant”, Metrologia 50 (2013) 354-376.

Dr Podesta’s measurements are extremely sophisticated, needed many years of work, and cooperations with several other laboratories. Dr. Podesta and collaborators constructed a highly precise resonant cavity filled with Argon gas. Dr. Podesta measured both the microwave resonance modes of the cavity to determine the precise radius and geometry, and determined the speed of sound in the Argon gas from acoustic resonance modes. Dr Podesta performed exceptionally accurate measurements of the speed of sound in this cavity, which can be said to be the most accurate thermometer globally today. The speed of sound can be directly related to 3/2 k.T, the mean molecular kinetic energy of the Argon molecules. In these measurements, Dr. Podesta very carefully considered many different types of influences on his measurements, such as surface gas layers, shape of microwave and acoustic sources and sensors etc. He achieved a relative standard uncertainty of 0.71. 10-6, which means that his measurements of Boltzmann’s constant are estimated to be accurate to within better than on millionth. Dr. Podesta’s measurements directly influences the precision with which we measure temperature in the new system of units.

Over the last 10 years there is intense effort in Europe and the USA to build rebuild the SI unit system. In particular NIST (USA), NPL (UK), several French institutions and Italian institutions, as well as the German PTB (Physikalische Technische Bundesanstalt) are undertaking this effort. To my knowledge there is only very small or no contribution from Japan to this effort, which was surprising for me.

What is today’s best value for the Boltzmann constant k:

VCSEL inventor Kenichi Iga: hv vs kT – Optoelectronics and Energy

(Former President and Emeritus Professor of Tokyo Institute of Technology. Inventor of VCSEL (vertical cavity surface emitting lasers), widely used in photonics systems)

VCSEL: how Kenichi Iga invented Vertical Cavity Surface Emitting Lasers

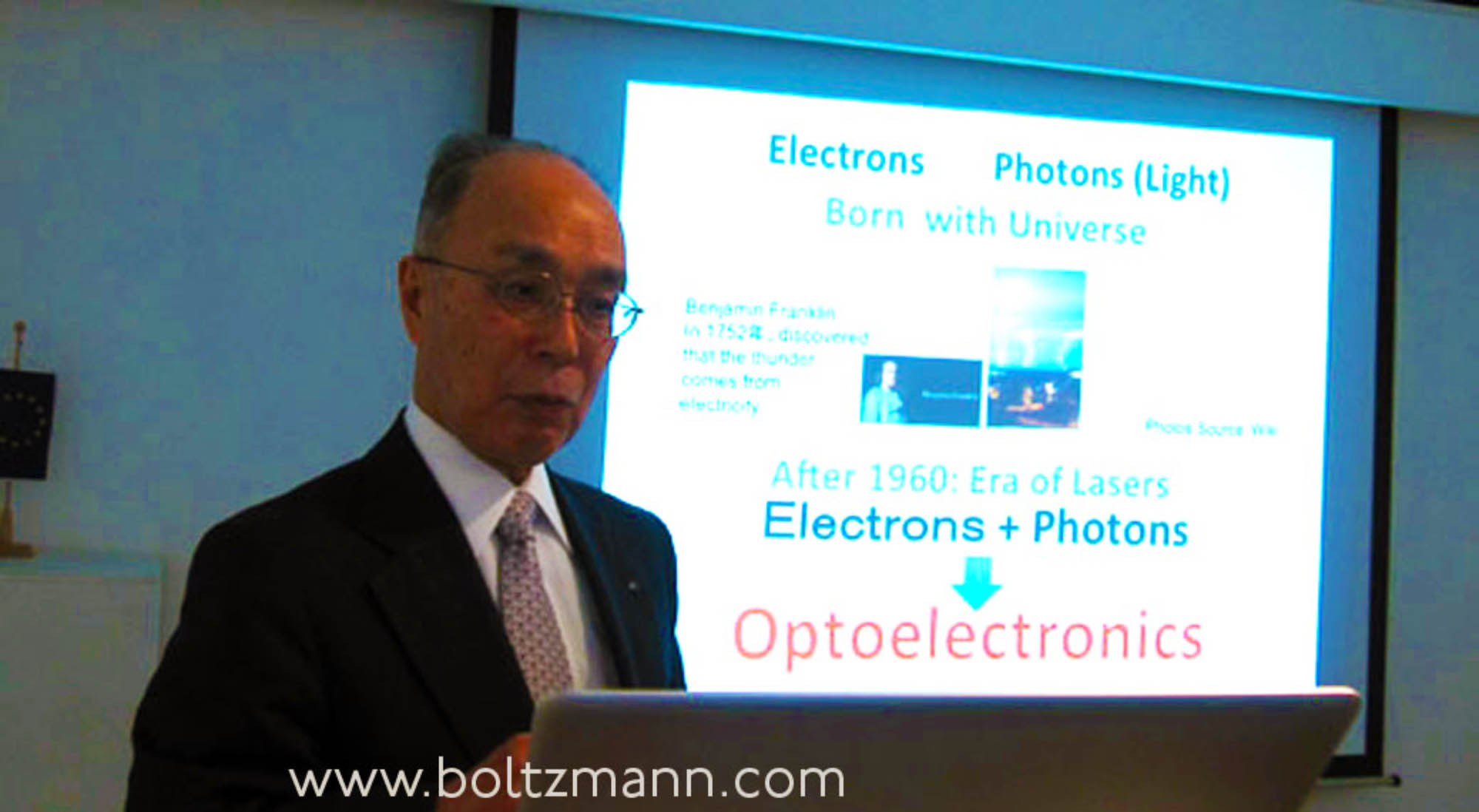

My invention of vertical cavity surface emitting lasers (VCSEL) dates back to March 22, 1977. Today VCSEL devices are used in many applications all over the world. I was awarded the 2013 Franklin Institute Award, the Bower Award and Prize for Achievement in Science, “for the conception and development of the vertical cavity surface emitting laser and its multiple applications in optoelectronics“. Benjamin Franklin’s work is linked to mine: Benjamin Franklin in 1752 discovered that thunder originates from electricity – he linked electronics (electricity) with photons (light). After 1960 the era of lasers began, we learnt how to combine and control electrons and photons, and the era of optoelectronics.

If you read Japanese, you may be interested to read an interview with Genichi Hatakoshi and myself, intitled “The treasure micro box of optoelectronics” which was recently published in the Japanese journal OplusE Magazine by Adcom-Media.

Electrons and photons

Who are electrons? Electrons are just like a cloud expressed by Schroedinger’s equation, which Schroedinger postulated in 1926. Electrons can also be seen as randomly moving particles, described by the particle version of Schroedinger’s equation (1931).

Where does light come from? Light is generated by the accelerated motion of charged particles.

Electrons also show interference patterns. For example, if we combine the 1s and 2p orbitals around a nucleus, we observe interference.

In a semiconductor, electrons are characterized by a band structure, filled valence bands and largely empty conduction bands. The population of hole states in the valence bands and of electrons in the conduction bands are determined by the Fermi-Dirac distribution. In typical III-V semiconductors, generation and absorption of light is by transitions between 4s anti-bonding orbitals (the bottom of the conduction band) and 4p bonding orbitals (the top of the valence band).

In Japan, we are good at inventing new types of vertical structures:

in 607, the Horyuji 5-Jyu-no Toh (5 story tower) was built in Nara, and today we have progressed to building the 634 meter high Tokyo Sky Tree Tower.

in 1893, Kubota Co. Ltd. developed the vertical molding of water pipes

in 1977 Shunichi Iwawaki invented vertical magnetic memory

in 1977 Tatsuo Izawa developed VAD (vapor-phase axial deposition) of silica fibers

in 1977 Kenichi Iga invented vertical cavity surface emitting lasers (VCSEL)

Communications and optical signal transmission

History of communications spans from 10,000 years BC with the invention of language, and 3000 BC with the invention of written characters and papyrus, to the invention of the internet in 1957, the realization of the laser in 1960, the realization of optical fiber communications in 1984, and now since 2008 we see Web 2.x and Cloud.

Optical telegraphy goes back to 200 BC, when optical beacons were used in China: digital signals using multi-color smoke. Around 600 AD we had optical beacons in China, Korea and Japan, and in 1200 BC also in Mongolia and India.

In the 18th and 19th century, optical semaphores were used in France.

In the 20th century, optical beam transmission using optical rods and optical fiber transmissions were developed, which combined with the development of lasers created today’s laser communications. Yasuharu Suematsu and his student showed the world’s first demonstration of optical fiber communications demonstration on May 26, 1963 at the Tokyo Institute of Technology, using a He-Ne laser, an electro-optic crystal for modulation of the laser light by the electrical signal from a microphone, and optical bundle fiber, and a photo-tube at the other end of the optical fiber bundle to revert the optical signals back into electrical signals and finally to drive a loud speaker. For his pioneering work, Yasuharu Suematsu was awarded the International Japan Prize in 2014.

VCSEL: I recorded my initial idea for the surface emitting laser on March 22, 1977 in my lab book.

Vertical Cavity Surface Emitting Lasers (VCSEL) have many advantages:

ultra-low power consumption: small volume

pure spectrum operation: short cavity

continuous spectrum tuning: single resonance

high speed modulation: wide response range

easy coupling to optical fibers: circular mode

monolithic fabrication like LSI

wafer level probe testing

2-dimensional array

vertical stack integration with micro-machine

physically small

VCSEL have found applications in many fields, including: data communications, sensing, printing, interconnects, displays.

As an example, the Tsubame-2 supercomputer, which in November 2011 was 5th of top-500 supercomputers, and on June 2, 2011 was greenest computer of Green500, uses 3500 optical fiber interconnects with a length of 100km. In 2012: Too500/Green500/Graph500

IBM Sequoia uses 330,000 VCSELs.

Fuji Xerox introduced the first demonstration of 2 dimensional 4×8 VCSEL printer array for high speed and ultra-fine resolution laser printing: 14 pages/minute and 2400 dots/inch.

VCSEL photonics started from minor reputation and generated big innovation. VCSELs feature:

low power consumption: good for green ICE

high speed modulation beyond 20 GBits/second

2D array

good productivity due to monolithic process

Future: will generate ideas never thought before.

em. President of Tokyo Institute of Technology, Professor Kenichi Iga, inventor of VCSELGerhard Fasol (left), em. President of Tokyo Institute of Technology, Professor Kenichi Iga (right)

Start-up Nation Israel 2014 – Israel Japan Investment Funds meeting on March 4, 2014 at the Hotel Okura in Tokyo

Israeli Venture funds introduce Israeli ventures to Japanese investors

Acquisition of Viber by Rakuten draws attention in Japan to Israeli ventures

The recent acquisition of the Israel-based OTT (over the top) communications company Viber by Rakuten for US$ 900 Million has drawn attention in Japan to Israel’s innovative power, however many Japanese companies are already cautiously investing in Israel while keeping a low profile, we learnt at the “Start-up Nation Israel 2014” Israel Japan Investment Funds meeting on March 4, 2014 at the Hotel Okura in Tokyo.

Most of the companies presented at the conference were highly sophisticated computer security, medical equipment, and similar “mono zukuri” type ventures, but also included a “selfie” app for auto-portrait or group photos using iPad or iPhone.

By the way: our company is currently working to sell an Israeli venture company to Japan as an exit for investors, and to accelerate business development in Japan for this company.

Her Excellency, Ambassador of Israel to Japan, Ms Ruth Kahanoff opened the conference:

Her Excellency, The Ambassador of Israel to Japan, Ms Ruth Kahanoff

Economic Minister of Israel to Japan, Mr Eitan Kuperstoch explained that while there is substantial investment in Israel’s ventures by many major Japanese corporations, there is much scope for increases. Japan’s investment added together are on the order of 1% of foreign direct investments to Israel:

Economic Minister to Japan of Israel, Eitan Kuperstoch

Pitches by Israeli Venture Funds

BRM Group: actually a privately held fund, strictly speaking not venture capital

CHIMA Ventures: medical devices, minimal invasive surgery tools.

TERRA Venture Partners: Terra invests in about 16-20 (4-5 per year) for a 1-2 year incubation period, followed by a “cherry picking” process. Terra VP invests in companies surviving the “cherry picking”. Veolia, GE, EDP, Clearweb, Enel are partners.

Giza Venture Capital: 5 funds, US$ 600 million under management, 102 investments, 20 active, 38 exits. Examples are: XtremIO, Actimize, Telegate, Precise, Plus, msystems, cyota, Olibit, Zoran, XTechnology. A particular success story is XtremIO: the team of 21 people (including secretary) turned US$ 6 million investment into a US$ 435 million cash sale to EMC.

StageOne Ventures: Early stage US$ 75 million fund, 17 investments.

Gillot Capital Partners: seed and early stage. Focus: cyber security.

SCP Vitalife Partners: 2 funds, US$ 230 capital under management.

Magma Venture Partners: focus on information and communications sector. Created over US$ 2 billion in acquired company value. Biggest success story: waze (crowd sourced location based services), return on capital investment: 171-times.

OrbiMed Healthcare Fund Management: largest global healthcare dedicated investment firm.

Nielsen Innovate:

Panel discussion of Israeli Venture Capital Fund Managers and the Vice-President of Japan’s Venture Capital Association

Presentations and Panel discussion

Arik Klienstein: Driving innovation in Israel – the 8200 impact

8200 is a unit within the Israeli Defence Forces similar to the US NSA – technology based intelligence collection. 8200 veterans lead many Israeli start-ups including NICE, Verint, Check Point, paloalto.

8200 and the start up culture:

Select the best people out of high school or college

Short first formal training. Most of training done on the job

Flexible dynamic organizational structure

Direct and constant relationship with the end user

“Think out the box” mentality – no assumptions. Hierarchy-less flat structure

Must win attitude!

Tal Slobodkin (Talpiot 18 Graduate): The Talpiot program

Talpiot is Israel’s elite Israel Defense Forces training program, dedicated to create leading research and development officers for the various branches of the Israeli Defence Forces. Program was created in 1979, about 1000 graduates today.

Selection process:

starts with 15,000++ high school seniors

100-150 attend next level of leadership assessment

50-75 reach final selection committee

30-40 enter the program

25-35 graduate

Training and assignment:

three full academic years

full dual degree in Maths and Physics, most graduate additionally in Computer Science or other subjects

military training

significant exposure to all cutting edge military and non-military innovation

develop management skills

graduates pick own final assignment

minimum assignment is additional 6 years, average tenure in Israeli Defense Forces is 10 years

Notable graduates:

Yoaf Freund: Professor at UC San Diego, Goedel Prize winner

Elon Lindenstrauss, Professor of Mathematics at the Hebrew University and winner or 2010 Fields Medal

Marius Nacht, co-founder of Check Point Software

Eli Mintz, Simchon Faigler, Amir Natan, founders of Compugen Ltd

Founders of XIV, sold to IBM for US$ 400 million

Eviatar Metanya, head of National Cyber Bureau

Ophier Shoham, head of Israel’s Defence R&D Agency (Israel’s DARPA)

Elchana Harel (Harel-Hertz Investment House): Japanese investments in Israel

94 Japanese investments in Israeli High-tech during 2000-2014:

ICT: 41 investments

Semiconductors: 25 investments

Life sciences: 11 investments

VC funds: 17 investments

Characteristics:

Most investments are strategic, not financial, not exit driven

Most investments are direct into target companies, and relatively small by global standards: up to US$ 3 million

In many cases “silent investments”: e.g a Japanese electronics company does not want their Japanese competitors to know that they invest in Israel

Japanese investors mostly follow Israeli or US lead investors. Japanese investors seldom lead.

Japanese acquisitions in Israel:

Nikken Sohonsha: NBT

Yasukawa Robotoics: Yasukawa Israel (Eshed), Argo Medical Robotics

David Heller: cooperation of Israeli investment funds with Japan

Israel’s venture capital fund industry was created by Israel’s Government creating the Yozma Fund of Funds: Israel’s Government invested a total of US$ 100 million in 10 VC funds (US$ 10 million per fund) under the condition that these funds had to attract much larger non-Government investment. In total the Yozma Fund of Funds invested US$ 100 million and resulted in a VC fund industry with a total of US$ 17 Billion of VC funds raised since 1993.

There is a relatively large number of Japanese investments in Israeli funds, however, the combined total investment is rather low, approximately 1% of all foreign investments in such funds. Thus there is much scope for increased Japanese investments in Israeli funds and ventures.

Steve Jobs and SONY: why 180 degrees opposite decisions?

Steve Jobs donates history to Stanford University in order to focus on the future

Steve Jobs and SONY – when Steve Jobs when returned to Apple in 1996, and now SONY are faced with the same question: what to do about corporate archives and the corporate history museum? Interestingly Steve Jobs, and SONY reach exactly 180 degrees opposite answers to the same question:

Steve Jobs donates Apple corporate archives and company museum to Stanford University

SONY sells headquarters building, and keeps SONY corporate archives and company museum

Why opposite answers to the same question? Could it be good advice for SONY, to learn from Steve Jobs, and donate SONY-Museum and SONY-Archives to a University, and focus much more on the future?

Apple donates history collection to Stanford University:

London Stock Exchange formed the Tokyo AIM market as a joint venture with Tokyo Stock Exchange and now withdraws from this venture and from Japan

Initially, London Stock Exchange and Tokyo Stock Exchange created Tokyo-AIM as a joint-venture company in order to create a jointly owned and jointly managed AIM Stock Market in Tokyo, modeled according to the very successful London-AIM model.

“Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own” NIKKEI on March 26, 2012

However, on March 26, 2012 NIKKEI reported that “Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own. TSE plans to improve the rules of its own new market, so that TSE can create a more welcoming market” (our translation of the original Japanese NIKKEI article to English).

London Stock Exchange withdraws from joint venture, and Tokyo Stock Exchange takes 100% control of Tokyo AIM

London Stock Exchange withdrew from the venture, and Tokyo Stock Exchange took over 100% of Tokyo-AIM. Essentially, London Stock Exchange AIM’s venture into Japan failed, while the stock market created by the venture continues without London Stock Exchange’s involvement. As explained in our blog here, these events are very very similar to what happened with NASDAQ about 10 years earlier!

Tokyo AIM name changed to TOKYO PRO Market and TOKYO PRO-BOND Market

In 2012, the name was changed from Tokyo-AIM, to TOKYO PRO Market and TOKYO PRO-BOND Market. Details can be found here:

AppAnnie showed that in terms of combined iOS AppStore + Google Play revenues, Japan is No. 1 globally, spending more than the USA. Therefore Japan is naturally the No. 1 target globally for many mobile game companies, and 10 out of 25 top grossing apps in Japan are of foreign origin!

Many foreign game companies have failed and given up. Foreign game companies that have recently given up in Japan include Zynga and Habbo Hotel. EA has given up twice, and is now undertaking the third entry to Japan. To understand some of the key mistakes foreign companies make in Japan, read our blog about why Vodafone failed in Japan.

Lets have a look at the list of top grossing games in the Apple iOS AppStore today. Out of the 25 top grossing games in the AppStore, 10 are by foreign originating companies. Can you guess which these are by reading the list below?

So Japan is certainly not a “closed market”. Actually, it is obvious that Apple does not discriminate in any way against foreign companies in Japan.

Interestingly, neither Nintendo, nor Rovio’s games, such as Angry Birds appear among the 200 “top grossing games” in Apple’s iOS Japan AppStore.

Apple iOS AppStore-Japan “Top Grossing” games ranking – 10 out of the 25 top grossing apps in Japan are by companies of foreign origin

Can you guess which 10 are by companies of foreign origin?

Flappy bird Angry Birds ultimate disruption: flappy bird effortlessly flaps to to the top of ranks, while Angry Birds are watching angrily from the sidelines

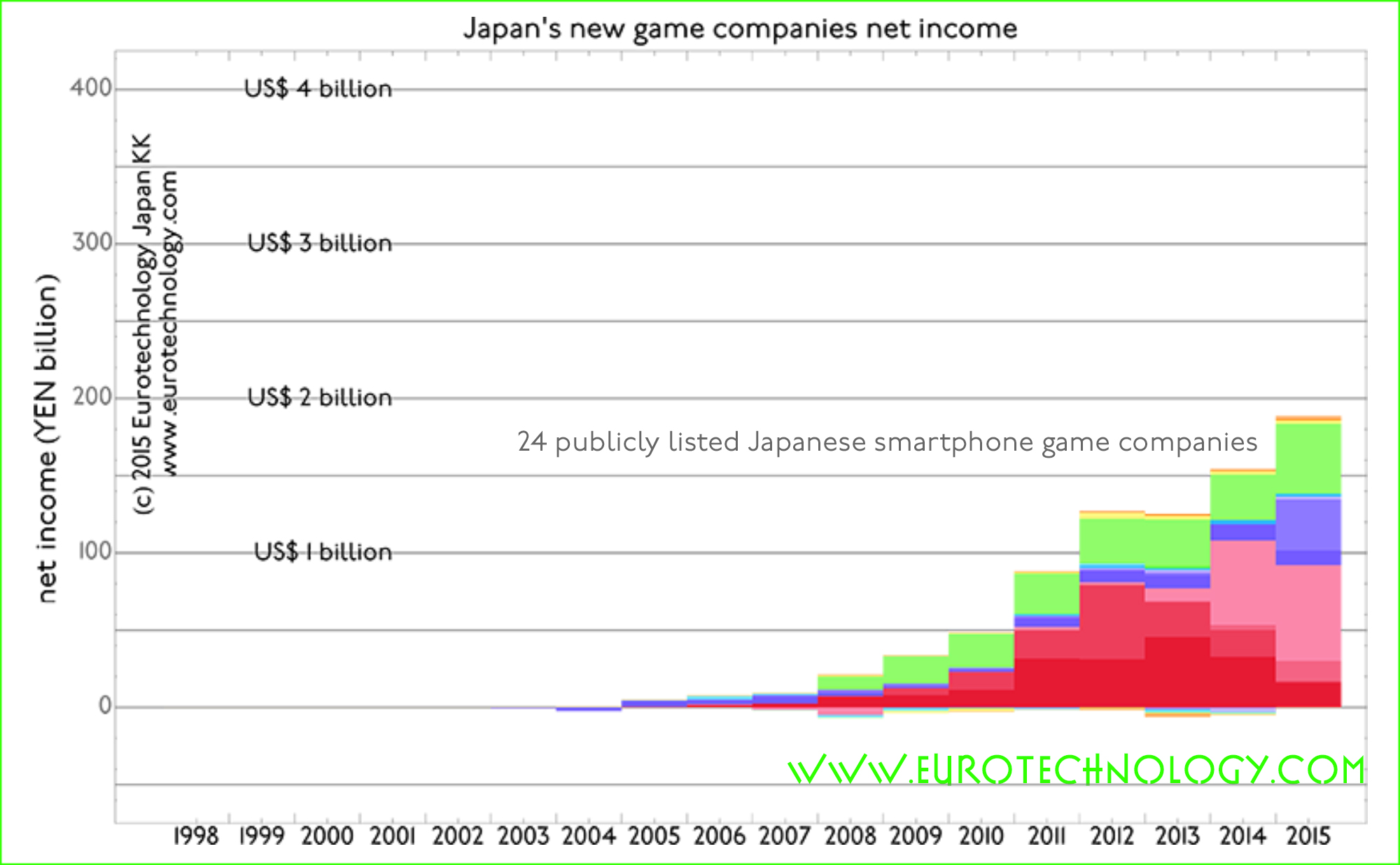

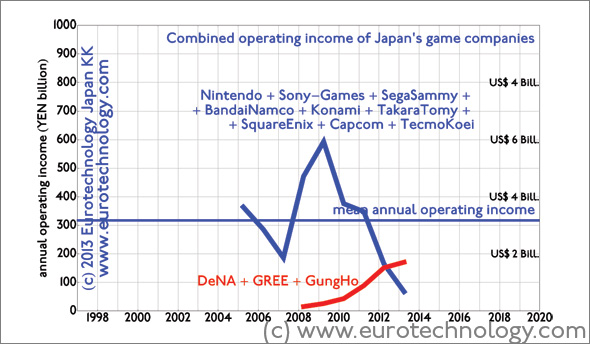

Disruption of Japan’s games sector: in a previous blog post we showed that just three newcomers (Gree + DeNA + Gungho) produce more profits than the top 9 traditional game companies combined.

Lets look at some more disruption from the perspective of Japan’s iPhone App store. Lets look at Flappy Bird vs Angry Birds…

Flappy bird Angry Birds ultimate disruption: iOS Japan AppStore “free” games ranking

February 3, 2014, in the “free” ranking in the games section of the iPhone AppStore, we find LINE dominating.

And newcomer Flappy Bird has overtaken Angry Birds by a long margin. Angry Birds Go! appears on rank No. 97 – which actually in Japan is not that bad, given the huge revenues in Japan – as App Annie has shown, Japan’s the world’s biggest grossing apps market both for iOS and Android – so No. 97 in the world’s biggest App market is not that bad.

In a subsequent article we analyze the top grossing 25 apps in the iOS AppStore.

Philip Rubel, CEO of Saatchi & Saatchi Fallon Tokyo KK gave a talk about “Lovemarks”, a concept in branding developed by Saatchi & Saatchi CEO Kevin Roberts.

To understand Japan’s media landscape read the “Japan’s media” report.

The argument is that traditional “brands” are losing relevance because in our advanced “post-industrial” societies, function and technology are given, and can usually be rapidly reproduced or overtaken by competitors. Therefore, advertising based on function or technology does not work anymore. Another factor is the shift from traditional one-way media such as TV and print, to social media and peer-to-peer interactions, where anyone can publish anything about “brands” and “brands” cannot do anything about it directly. Thus traditional brands are dead. So, how can we get people to attach irrationally, beyond reason? Lasting relationships are not based on rational thinking.

Japan brand management: Lovemarks create loyalty which goes beyond reason

“Lovemarks” counter these effects: the concept of Lovemarks is to “create loyalty which goes beyond reason”. To create love for the Lovemarks. To get there, Saatchi & Saatchi believes in the “unreasonable” power of creativity: creativity can create loyalty beyond reason.

Philip Rubel showed us several examples of campaigns, mainly in Japan, which were successful far beyond expectations. These campaigns are based on creativity, incorporate surprise, appeal to emotion, and aim to exploit viral sharing on social media such as facebook and YouTube. Creativity is used to replace expensive traditional top-down one-way media such as TV and print, by social media, internet, YouTube and viral sharing and engagement. Here are some examples:

BMW films by Fallon

The issue was to develop the BMW brand in USA with limited budgets. BMW Films was a series of films created by famous directors and famous actors, which was uploaded to the BMWfilms.com website for download. BMW Films became famous, actors volunteered to appear, and download figures were far beyond plan.

The Hire – Star (by BMW Films)

BMW Films – The Hire – Beat the Devil

SONY Bravia balls in San Francisco

SONY Bravia bouncy balls

Making of SONY Bravia bouncy balls

Making of SONY Bravia bouncy balls

SONY Bravia paint

SONY Bravia – Paint

Godiva Love & Hug project for Valentine’s day 2013

For Valentine’s day 2013, Saatchi & Saatchi built a hugging robot, which people could hug, and the hugs were measured, rated, and photographed, and the results could be displayed on social network sites etc. The campaign is explained here on Saatchi & Saatchi’s website.

Godiva Love & Hug project for Valentine’s day 2013

De’Longhi had the issue of competing with much more powerful Nestle’s campaign centered on George Clooney. De’Longhi decided to use Michelangelo’s David, who is immensely popular in Japan – and who does not require actor’s fees…

Reebok Rajio Taiso

Radio Taiso is a morning gymnastics series, which Japan’s national radio and TV system NHK started back in 1928. Saatchi & Saatchi created an imitation of Radio Taiso using professional acrobats, and relied on viral marketing. The advertised brand name appears only very briefly at the end of the video clip – enough to create response far beyond expectations:

Reebok Rajio Taiso

T-Mobile “Life’s for sharing” campaign

T-Mobile “Life’s for sharing” Royal Wedding episode currently has 27,539,402 views on YouTube:

T-Mobile “Life’s for sharing” campaign

Understand Japan’s media and advertising industries

Report on Japan’s Media (approx. 200 pages, pdf file)

EU Japan investment stock is expected to increase with the future Economic Partnership Agreement

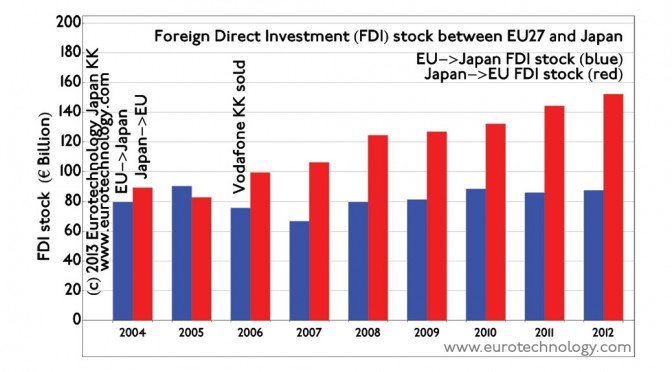

European direct investments into Japan, European acquisitions in Japan

EU investments in Japan have been relatively constant around EURO 80 billion. There has been a marked reduction in EU investment in Japan in 2006 due to the withdrawal of Vodafone from Japan with the sale of Vodafone KK to Softbank for approx. EURO 12 billion (find details of the Vodafone-SoftBank M&A transaction here). This reduction of EU investment stock in Japan is clearly visible in the graphics below in 2006 and 2007.

Japanese direct investment in Europe, Japanese acquisitions in Europe

Japanese investments in EU are steadily increasing, as Japanese companies are seeking to grow business outside Japan’s saturated market, and as Japanese companies acquire European companies for market access, technology and global business footprint. In 2012 the total investment stock of Japanese companies in the EU-27 has reached around EURO 150 billion.

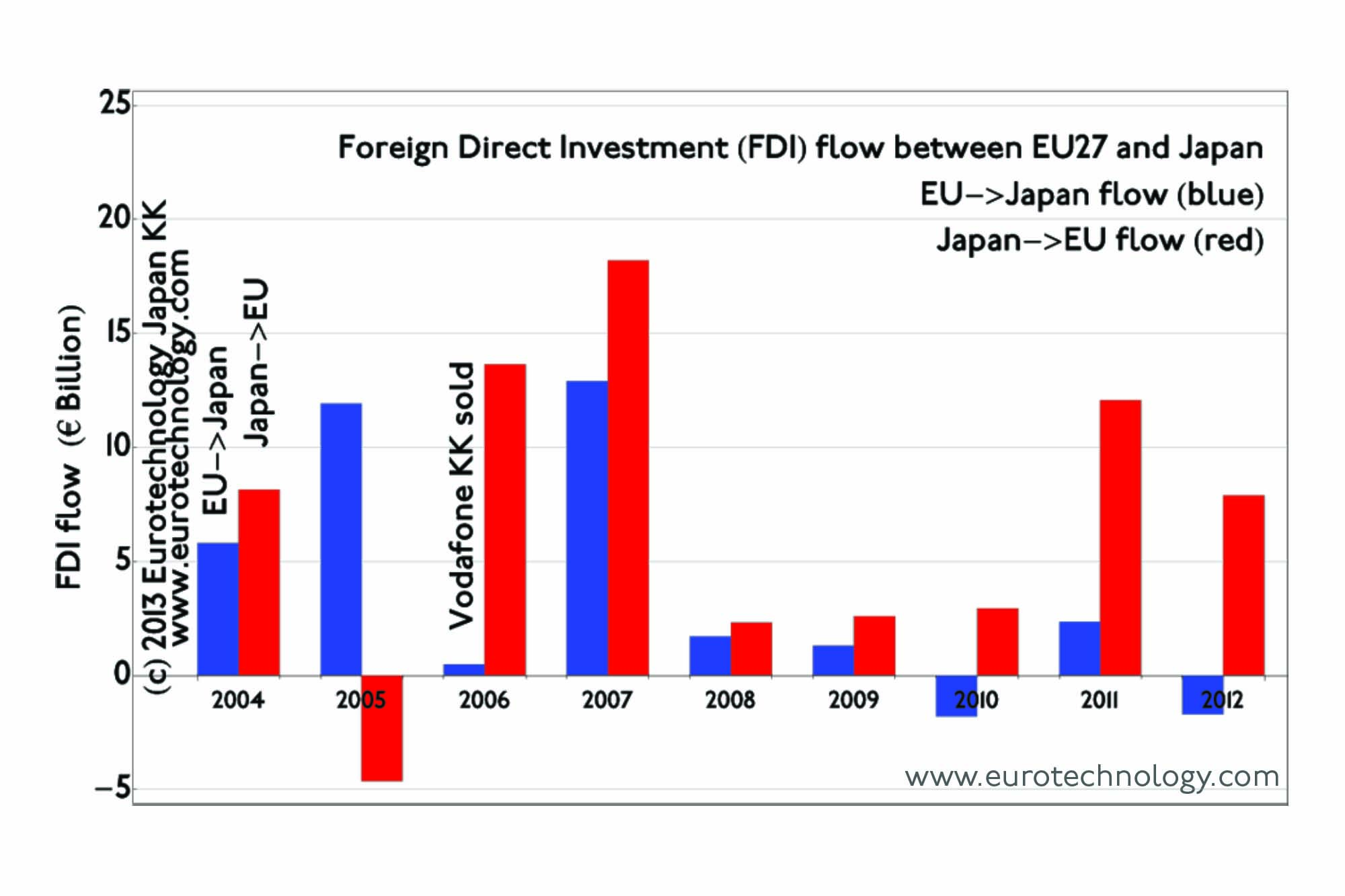

EU Japan investment flow is mainly from Japan to Europe and totals about EURO 10 billion per year

Investment flow between EU and Japan shows strong impact from the Lehmann shock economic downturn, and was very quiet between 2008 and 2010. In recent years, mainly Japanese investments to Europe have picked up, and currently about EURO 10 billion per year flow from Japan to Europe, Japanese companies acquiring European companies to globalize and also to pick up known-how and technologies.

Investment flow from EU to Japan remains at relatively low levels around EURO 1 billion annually, while investments by Japanese companies in the EU are on the order of EURO 10 billion per year currently.

Japan to Europe direct investment register:

Investment flow recently is almost one way from Japan into Europe.

EU Japan investment flow is mainly from Japan to Europe and totals about EURO 10 billion per year

With the expected Economic Partnership Agreement (EPA) we expect investment flows to increase in both directions.

The pressure to globalize, and saturation of Japan’s markets drives Japanese corporations to invest in Europe, therefore we expect the future Economic Partnership Agreement between Japan and EU to stimulate further Japanese investments in Europe more than in the Europe -> Japan direction.

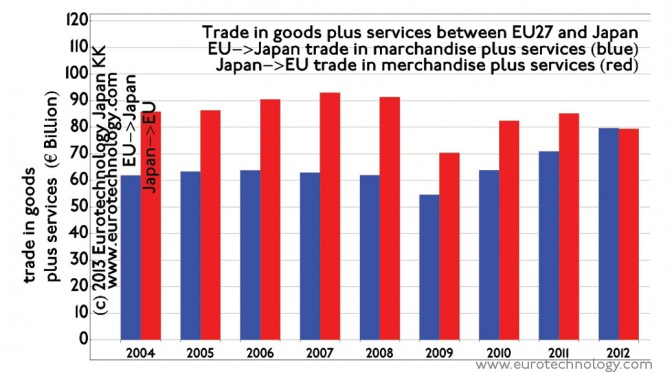

EU Japan trade adds up to about EURO 160 billion/year if both directions are added up

Combining the amounts of trade for merchandise and commercial services, EU exports to Japan and Japanese exports to EU have reached equal levels, so that the trade between EU and Japan is now balanced around EURO 80 billion in each direction, i.e. a combined trade of EURO 160 billion.

EU Japan trade: EU is traditionally stronger in the export of commercial services while Japan is stronger in the export of manufactured goods

Japan is traditionally stronger in the export of manufactured goods, while EU is stronger in the export of commercial services. Combining both merchandise and services, the trade between EU and Japan is now balanced.

EU Japan trade: the trade deficit is balanced out now

There used to be a trade deficit and trade friction: Japan used to export much more to Europe, than Europe exported to Japan. Recently, Europe has increased exports to Japan considerably, and the trade is now balanced in both directions.

SOMPO, a Japanese insurance company owned by NKSJ Holdings, acquired Canopius in order to globalize

In order to globalize, Japanese insurance company Sompo Japan (株式会社損害保険ジャパン), part of the insurance group NKSJ Holdings (NKSJホールディングス株式会社, TSE / JPX: No. 8630) announced yesterday the acquisition of 100% of the UK re-insurer Canopius Group Limited, operating on Lloyd’s for UKL 594 million (US$ 972 million), from the current owners. Current majority owner of Canopius is Bregal Capital.

Canopius will keep the brand, company name, and management team.

Canopius, is an insurance group, one of the top ten insurers in the Lloyd’s market, was founded in December 2003, almost exactly ten years ago, via a Management Buy-Out (MBO) with UKL 25 million capital, which grew about twenty-fold to about UKL 500 million today, and today has about 560 employees.

Canopius is named after Nathaniel Canopius, native of Crete, who studied at Balliol College, Oxford, apparently introduced coffee drinking to Oxford around 1637 (according to the Canopius website), and later became Archbishop of Smyrna (Source: “Anglicans and Orthodox, Unity and Subversion, 1559-1725”, by Judith Pinnington, 2003, ISBN 0-85244-577-6, page 15).

Japanese management – why is it not global? What should we do? Keynote speech by Masamoto Yashiro at brainstorming by President of Tokyo University

summary of Masamoto Yashiro’s talk written by Gerhard Fasol

Masamoto Yashiro is a legend in Japan’s banking and energy industry. He built Shinsei Bank from the ashes of the bankrupt Long Term Credit Bank of Japan, and served in leadership positions (Chairman, CEO, Board Member) in Esso, Exxon, Citibank, Shinsei Bank, and the China Construction Bank.

Tonight a small group of about 60 people were invited to join Masamoto Yashiro and the President of The University of Tokyo, Professor Junichi Hamada, for an evening workshop and brainstorming event about globalization of Japanese corporations at The University of Tokyo. Participating were a selected group of The University of Tokyo graduates, faculty, and selected alumni from several elite Universities associated with The University of Tokyo, and currently working at major Japanese trading companies, Ministry of Finance, financial firms, global consulting firms and other global firms.

After The University of Tokyo President Junichi Hamada’s introductory words, we heard Masamoto Yashiro’s fantastic overview of how he thinks Japanese companies need to change and why, followed by Q&A, then by a brainstorming session in the format of changing groups of four on about 15 separate tables between the participants, and then followed by buffet and drinks reception.

Topic of the evening was the globalization issues of Japanese corporations, also discussed in our work about Japan’s Galapagos issues:

Masamoto Yashiro graduated from Kyoto University (Law Faculty) in 1954 and The University of Tokyo Graduate School in 1958, and entered Standard Vacuum Oil Company. In 1964 he became Director of Esso, and later Special Assistant to the Chairman of Standard Oil New Jersey, and in 1986 President of Esso Sekyu KK. In 1989, Masamoto Yashiro moved to become Japan representative of Citibank NA, and Chairman of Citicorp Japan in 1997. IN 1999, Masamoto Yashiro became CEO of New LTCB Partners CV, the company emerging from the bankruptcy proceedings of the Long Term Credit Bank of Japan, and was in charge of the revival of LTCB as Chairman and CEO, with investment from Ripplewood Investment Fund, creating today’s Shinsei Bank. He resigned as CEO of Shinsei Bank in 2005, but returned as Chairman and CEO in 2008, from which he retired in 2010. In 2004, he was appointed Director of the China Construction Bank.

Masamoto Yashiro (former Chairman of Shinsei Bank, Chairman of Citicorp Japan and President of Esso Japan, Director of China Construction Bank)

Japanese management – why is it not global? What should we do? asks Masamoto Yashiro

Note: this record was reviewed personally by Masamoto Yashiro, who made some corrections.

Japanese management – why is it not global? Outline:

Some people may argue that Japanese companies need not be global. Why?

We must accept that English is an essential tool for international communication.

Some impediments that Japanese companies face:

The traditional approach is not effective in developing future leaders.

The Japanese-style board structure is not appropriate to ensure sound corporate governance.

Management structure needs to be changed to suit a global business.

The current limited role of foreign nationals in the management and board structure

What should be the most important corporate objective?

Concluding remarks

Masamoto Yashiro (standing at the podium on the right hand side) presenting and President of Tokyo University Junichi Hamada (sitting on the left) listening

Summary of Masamoto Yashiro’s talk:

Some people may argue that Japanese companies need not be global. Why?

Some superficial discussions about “Japanese companies” contrast “permanent employment” and excellent pensions in Japanese companies with job-hopping and bad pensions in other countries, however, Masamoto Yashiro points out that during his time at Esso and later Exxon, most employees stayed 20-30 years at Exxon, and received excellent pensions, so “permanent longterm employment” or pension system has nothing to do with globalization, and Japanese leading companies are no different than leading companies in other countries in these respects. We have to search elsewhere for the causes of current problems most Japanese companies are facing.

Around 1990, about 20 years ago, Japan was extremely self-satisfied by the successful reconstruction after the war and economic growth and success, and Japan felt that Japan does not have anything to learn from others. This time is now over, Japan is in stagnation, and many Japanese companies are not globally competitive, and Japan and Japanese companies must change to become competitive again.

We must accept that English is an essential tool for international communication.

Masamoto Yashiro is convinced that Japanese companies must globalize, and must make English a business tool. He feels it is a great disadvantage that Japanese political and corporate leaders, when participating in international conference, such as Davos, mostly need to use interpreters, and this reduces their global impact and exchange of ideas dramatically.

Some impediments that Japanese companies face:

1. The traditional approach is not effective in developing future leaders.

The traditional approach in Japan is to rotate career employees every two years between totally different functions, in order to “develop well-rounded managers”. The result of this process are non-experts, which are not expert in anything.

As an example, during his leadership at Shinsei Bank, Masamoto Yashiro once requested a meeting with the IT Department leadership. To his great surprise 60 people turned up for the meeting (he had expected 2 or 3). He asked the Department Chief for particular information, and he could not understand the question and could not answer, same result one management lower. Only at the third layer from the top, Masamoto Yashiro could get his question answered – the top two management layers could not answer his questions about the work of the IT Department. Quite generally there often far too many people at meetings at Japanese companies.

When at Exxon in the US as a relatively junior manager, Masamoto Yashiro, was asked about his opinion regarding the termination of a particular joint-venture relationship with a mid-size petroleum refining company in Japan known then as ゼネラル石油精製 who had financial trouble. Exxon had a 50% interest in this company and its relations goes back to very late 1950’s. In late 1985 at the Exxon Management Committee meeting in New York, all other managers favored to terminate the relationship with this joint venture partner in trouble in order to limit financial exposure, while Masamoto Yashiro argued that it was better to support the troubled partner and assist him with Exxon staff and expertise to return to profitability. To his great surprise the Chairman and his superiors at Exxon sided with his recommendation and changed their previous position following his advice. Generally he felt that in the USA his opinion as a Japanese manager was highly valued, because it provided a different view point.

In his experience in Japan the situation is totally opposite: Japanese senior management generally does not listen to junior employees, and particularly not to foreign nationals in the rare cases that there are any in Japanese companies. In fact, the most frequent question senior management at Japanese banks ask, is not for original ideas or creativity from junior staff, but instead: “What do other banks do?”

This deplorable Japanese situation even contrasts strongly with the situation in China, where Masamoto Yashiro was a Director of the China Construction Bank: in China leaders moved from Government agencies and Ministries to Banks, and to private industries and back.

Generally Masamoto Yashiro expressed the view, that the development of leaders is totally inadequate in Japan, and is better in China than in Japan.

In addition to the inadequate development of leaders in Japanese companies, the number of foreign nationals in management, Board and other leadership positions in Japanese companies is minute, there are no programs to attract and develop foreign nationals in leadership positions. On the contrary, when Shinsei Bank showed losses in the aftermath of the Lehman shock, Japan’s Financial Services Agencies ordered that Shinsei Bank must pay all foreign nationals on exactly the same pay levels as Japanese employees. Since foreign nationals typically have much higher schooling and other costs in Japan than Japanese staff, essentially all non-Japanese staff at Shinsei Bank left soon after.

Leaders can make a real difference.

How leaders are selected is of utmost importance.

At Exxon, senior management devote specially reserved time to identify suitable candidates for future leadership positions, “who can potentially be our CEO in the future”. The selected candidates are given special attention and special opportunities to train and develop their leadership abilities. Masamoto Yashiro has never heard about such special leadership development programs at Japanese companies.

2. The Japanese-style board structure is not appropriate to ensure sound corporate governance.

In Japan, Board Members are almost always managing employees of the company, so the question arises who’s interests they represent on the Board. Do they represent the interests of the institution (the company), the employees or the interests of the shareholders.

In Japan often the CEO of the company after his retirement remains as a Chairman for several years, keeps his office, secretary and company car, and creates large other expenses. Why? Probably because Japanese CEO pay is too low, so that the CEO does not wish to retire gracefully.

This is totally different in Western companies where retired CEOs leave the company and have no further role in the company in most cases. Masamoto Yashiro mentioned the retired Chairman of Exxon, who after his retirement naturally travelled by taxi. In Japanese it would be unthinkable according to Masamoto Yashiro that the retired Chairman of a major corporation would travel by ordinary taxi cab like ordinary people (Masamoto Yashiro did not mention subway or bus, or driving his own personal car….)

3. Management structure needs to be changed to suit a global business.

In non-Japanese companies in almost all cases have a thorough performance evaluation system. When performance is evaluated, the resulting distribution must be similar to a normal distribution, i.e. with considerable part of employees at the high end and substantial numbers at the low end of the performance curve. If this is not done, top performers cannot be sufficiently rewarded and will leave the company, while low performers would hold the whole company back.

In most Japanese companies on the other hand, if a thorough performance evaluation is done at all, in most cases a huge proportion of employees are just evaluated as average, satisfying performance, without clear distinctions between top and bottom performance.

Promotion and salary on the other hand in traditional Japanese companies is purely according to age, which leads to many problems, and causes under-performance of the whole company.

These problems are increased by the fact, that Japanese companies typically do not give the same evaluation or opportunities to non-Japanese nationals.

4. The current limited role of foreign nationals in management and board structure.

Even in the rare cases where foreign nationals are employed by Japanese companies in management or leadership positions e.g. in foreign subsidiaries, often junior Japanese employees which much lower rank and local knowledge do not respect and bypass non-Japanese management, and there is typically no fair evaluation system, evaluating Japanese and non-Japanese management according to the same standards of performance.

The change of this mindset (to keep non-Japanese out of management or leadership positions at Japanese corporations) is extremely important.

The change of mindset (to keep non-Japanese out of management or leadership positions at Japanese corporations) is not difficult at all and can be done quickly.

What should be the most important corporate objective?

When considering corporate governance it is important to develop a view on the objectives. When discussing the interest of shareholders, it is important to ask “which shareholders”? The interests of large shareholders who may own 10% or 20% of the corporation, or the interests of individual smaller shareholders? Other stake holders’ interests also need to be taken into account.

In general, Masamoto Yashiro expressed the view that both the institution’s (the company’s) and the shareholders interest are best served by stable long-term growth of the company. He mentioned as an example Exxon which showed triple-A rating and annual rate of growth of 15%-17% for over 100 years.

Concluding remarks.

Around 1990 Japan was self-satisfied with the economic success, and Japanese people thought that they have nothing to learn from anybody. This time is over now, and Japan and Japanese corporations much change to regain growth and to become competitive again.

Professor Junichi Hamada, President of The University of Tokyo, listening to Masamoto Yashiro’s talk

Japanese management – Q&A with Masamoto Yashiro (selected questions)

Q. You want Japanese companies to change. What are the good things you want Japanese companies to keep?

A. Loyalty. Consideration to stakeholders.

Q. Your work at Shinsei.

A. Communication was most important. When Masamoto Yashiro took over at Shinsei, the Bank has just gone through bankruptcy proceedings, so the moral was extremely low. Masamoto Yashiro had to reestablish optimism and moral. To do so, communication is most important. Masamoto Yashiro held weekly telephone conferences and every employee who wanted to could participate: from top management to cleaning staff/janitors. Everyone could come forward with his concerns.

Another fact was that there were so many traditions which made no sense. For example, female employees with University degrees would wear their own clothes, while female employees without University degrees would need to wear company uniform. There was an issue that lower paid staff had difficulty to afford appropriate clothing for bank work – so Masamoto Yashiro decided to award a clothing allowance to employees so that they could afford appropriate clothing.

Q. Many Japanese companies cannot hire young employees, because they cannot fire/discharge non-performing older employees.

A. Firing/discharge of non-performing employees can be done by paying adequate severance compensation. Considering that a non-performing employee who remains on the payroll for several years in addition to salary also creates a lot of secondary costs, it is typically cheaper to pay an appropriate severance package, and most people are happy to leave with an appropriate severance package, and often move to a more suitable position at a different company – this helps everyone. Of course some companies want to save money at all cost, and fire employees without adequate package and that can lead to problems.

Q. Having worked much of your career at global oil or energy companies, what to you think about Japanese oil companies?

A. Japanese oil companies are not really oil companies, because they do not invest enough upstream.

Q. Leadership?

A. Japanese companies must change. The mindset must change.

Q. University of Tokyo?

A. University of Tokyo at the moment I think is ranked on 30th or 40th position globally in most rankings, maybe top in Japan or in Asia, but that does not count, we need to look at the whole world, not just Japan or Asia. I think University of Tokyo should make the changes necessary be at least in the top ten globally. To get into the top ten globally, University of Tokyo needs to hire outstanding Professors where the best students from the whole world want to come and study. To get the best Researchers and Professors University of Tokyo has to pay what is necessary. Does not matter which language, English or Japanese or any other language. No outstanding student from other parts of the world wants to study Japanese first before studying at University of Tokyo. University of Tokyo should make the necessary changes so that the best students from top Universities globally also want to come to University of Tokyo.

Mr Masamoto Yashiro’s talk and Q&A were followed by a brainstorming session in groups among all participants of four about globalization, and global leadership development.

Social media revolutionize brand marketing: people don’t want to be told what to buy, but want to discover and share

Social media marketing: Consumers have now taken control of what they watch, read and listen to and so the messages they receive are the ones they chose to receive. Brands must now deserve that attention through appealing to their needs and feelings and not simply by buying airtime on television.

Ray Bremner, President & CEO of Unilever Japan gave a talk at Waseda University

To understand Japan’s media landscape read the “Japan’s media” report.

Social media marketing (Ray Bremner, President & CEO, Unilever Japan)

From Advertising to consumers to mattering to people

My key take-away is that social media have made the top-down “begin told” way of advertising obsolete, and replaced it by finding, sharing and engaging.

About Unilever:

Unilever was founded in 1929 by the merger of the British soap maker “Lever Brothers” (founded in 1885 by William Hesketh Lever, The Right Honourable The Viscount of Leverhulme), with the Dutch margarine producer “Naamloze Vennootschap Margarine Uni”, which was formed by the merger of several margarine companies, including those of Antonius Johannes Jurgens and Samuel van den Bergh. Soap brought hygiene to ordinary people, and margarine helped people who could not afford butter. Both companies, Lever and Margarine Uni had in common that they used palm oil as raw material.

The merger of Lever and Margarine Uni was decided over dinner in London in 1929, and written down in a 100 word merger agreement – unthinkable today for an M&A agreement.

About 50% of Japanese people have Unilever products at home

Unilever vision 2010 is: double the business, while reducing the environmental footprint. Execution of this vision is measured by 60 KPIs and the results are published.

Unilever vision:

We work to create a better future every day.

We help people feel good, look good, and get more out of life with brands and services that are good for them and good for others. We will inspire people to take small everyday actions that can add up to a big difference for the world.

We will develop new ways of doing business that will allow us to double the size of our company while reducing our environmental impact.

Unilever mission: building brands that improve people’s lives.

Ray Bremner, President & CEO of Unilever Japan: Social Media is revolutionizing the way we market brands

Ray Bremner: “social media are revolutionizing the way we market brands, and they are making people like me extinct”.

From 2001 to 2013, the average time Japanese consumers spend watching TV has decreased from about 3 1/2 hours/day to 3 hours/day, while the time spent with PC & mobile has tripled from 1/2 hour/day to 1 1/2 hours per day. Most Japanese age groups use social media, usage peaks at 35% for men in their 20s, and around 45% for women in their 20s, and around 30% in their 30s.

TV reaches about 88% of Japan’s population, and digital media (PC and mobile) reach about 73%.

From 2001 to 2012, advertising expenditure in Japan has decreased from about US$ 27 Billion/year to US$ 23 Billion/year, while expenditure for digital media has increased from zero to US$ 12 Billion/year. For an overview of Japan’s media markets – see “Japan’s Media“.

How to make marketing messages a pleasure rather than annoying?

How do we succeed? Crafting brands for life.

Put people first, not just consumers. Real people with real lives.

Build brand love.

Unlock the magic.

The brand love triangle

How do you create a conversation people want to participate in?

We use the “brand love triangle. “The people we serve” are in the center. The three edges of the brand love triangle are:

Purpose (brand point-of-view) <— brand history dive

Product truth <— product dive

Human truth <— people immersion

Ray Bremner, President & CEO of Unilever Japan: Real people with real lives

“Dove Real Beauty Sketches” by Steve Miles

Brands need a purpose, a point of view. Before 2002 Dove did not have a purpose.

Steve Miles talking about Dove and himself:

93% of women do not think they are beautiful – men are opposite: 93% of men think that they look just great. Dave Miles (and Dove’s) point of view is that everyone is beautiful. This point of view is expressed in “Dove Real Beauty Sketches”, which won the Titanium Grand Prize and 10 Gold Lions at Cannes 2013:

As of today, “Dove Real Beauty Sketches” has 61,767,827 views on YouTube, which is not as much as PSY’s Gangnam Style with 1,888,086,686 views, but still – pretty amazing.

Another example of brand communication is Harley Davidson, which signifies “Freedom of the Road”, independent character. Harley Davidson creates a bond to customers by presenting each customer with the “umbilical cord”, the belt with which the Harley Davidson motor bicycle was tied down during the transport from the factory to the customer.

Focus: In 2000, Unilever had 1600 brands and today 400 brands.

Q&A

Question: How many of your campaigns in Japan are global campaigns? How many are Japan-only?

Answer: practically all campaigns for all international brands of any company are made in Japan for Japan. That is not to say that global ideas do not work. In fact in most cases International Brands have the same brand and advertising positioning in Japan as elsewhere in the world. What does differ for Japan is that often Japanese consumers have different usage habits, have different views about the world and the cues within the advertising can leave different impressions on Japanese minds. The Japanese consumer is highly observant of small details in advertising ; much more so than the average European for example.

That means that we test Global campaigns but very often we have to create Japan only executions so that how we express the idea is done totally with the Japanese consumer in mind. This is more costly and time consuming but essential for success.

On Thursday January 16th, 2014, NTT Docomo announced the postponement of mobile phone handsets based on the TIZEN operating system. This is actually the second time that NTT Docomo has postponed the planned introduction of TIZEN handsets, so it might become doubtful whether NTT Docomo will ever introduce TIZEN handsets.

In the announcement NTT Docomo essentially said that with the current market situation in Japan, it makes no commercial sense for Docomo to introduce a third smartphone operating system to the market.

The French journal Les Echos interviewed me about Docomo’s repeated postponement of TIZEN OS handsets. Here some notes I wrote up to prepare for the interview:

Both for handset makers like HTC or Samsung and it would be a dream to become independent of OS owners/controllers like Microsoft or Google, and for mobile operators like Orange or Docomo, it would be a dream to have an OS they can control, and where they can introduce their own services like Docomo’s “iconcier” personal digital assistant, which is to some extent competing with Apple’s SIRI and with various Google services. Its a dream but realization is a different story. Its not enough to make and further develop and maintain the full OS stack including UI, create a development environment and SDKs as easy to use and competitive with Apple’s and Google’s, app stores, build a developer community who create lots of apps. Its also necessary to make a critical mass of attractive devices, gain a critical mass of market share, create global scale, and most importantly win over all the most important Apps like Facebook, LINE, etc.

With the dramatically increasing complexity and sheer size of software, it becomes harder to bring mobile services to market without global scaleability, or at least a major part of the world, which usually will need to include China. Docomo does not have this global scale, so it will become harder and harder for Docomo to introduce own software services, such as iMode or iConcier.

Docomo has continuously lost market share and recently even net subscribers, and in December for the first time in recent memory succeeded to gain top position in subscriber gains, surely because of the iPhone. In addition, rumors are that Apple demands very high minimum sales shares of operator partners. So Docomo is under double pressure:

to satisfy contract conditions with Apple

to maintain subscriber gains

in addition, Docomo still has a substantial part of “iMode-keitai”, also called “galake” (= “Galapagos keitai”). So Docomo already has a large variety of OS and handset styles, and has recently reduced the number of different handset it supports, so going to Tizen would go against this trend.

Its not the end of Tizen. Tizen can in addition to smartphones also go into embedded applications such as cars, elevators, washing mashines etc.

Stanford Economics Professor Takeo Hoshi thinks that there is a 10% chance that Abenomics will succeed to put Japan on a 2%-3% economic growth path, while the most likely outcome will be 1% economic growth. Read our notes of Professor Hoshi’s talk in detail here.

Can Japanese companies globalize?

“Globalization” of course is not an aim in itself. In Europe and USA there are plenty of companies which are very successful and not globalized. However, Japan could capture much more global value from technology and creativity by creating more global companies: the shining example is SoftBank.

Read legendary Masamoto Yashiro’s viewpoints about globalization at a recent Tokyo University brainstorming event by the President of Tokyo University (Masamoto Yashiro was Chairman of Exxon-Japan, of Citibank-Japan, and Shinsei-Bank, and Board Member of the Construction Bank of China). Masamoto Yashiro says that a change of mind-set is urgently needed.

Until March 11, 2011, Japan’s energy markets were essentially frozen in the structures created in 1952, which again resulted from the war-time nationalization of Japan’s electricity sector (see our Energy Report). Japan’s electricity markets alone are worth about US$ 200 million per year – and this market is now in disruption.

Recently I was invited to brief the Energy Minister of Canada, Mr Joe Oliver, and Sweden’s Trade Minister Dr. Ewa Björling about Japan’s energy markets. My briefings are based on our analysis, which you can find in our Energy Report, and Renewable Energy Report.

The liberalization of Japan’s energy markets will create winners and losers – comparing the financial performance of Japan’s electricity companies and gas companies is an indication of things to come. Actually, only Japan’s electricity markets are being liberalized currently, liberalization of Japan’s gas markets is still for the future.