NTT Docomo announced the start of i-Mode on February 22, 1999 at a press conference in Tokyo

Today, 18 years ago, on February 22, 1999, Mari Matsunaga, Takeshi Natsuno, and Keiichi Enoki announced the start of the world’s first successful mobile internet service to a small number of people who made it to NTT Docomo’s press conference in Tokyo.

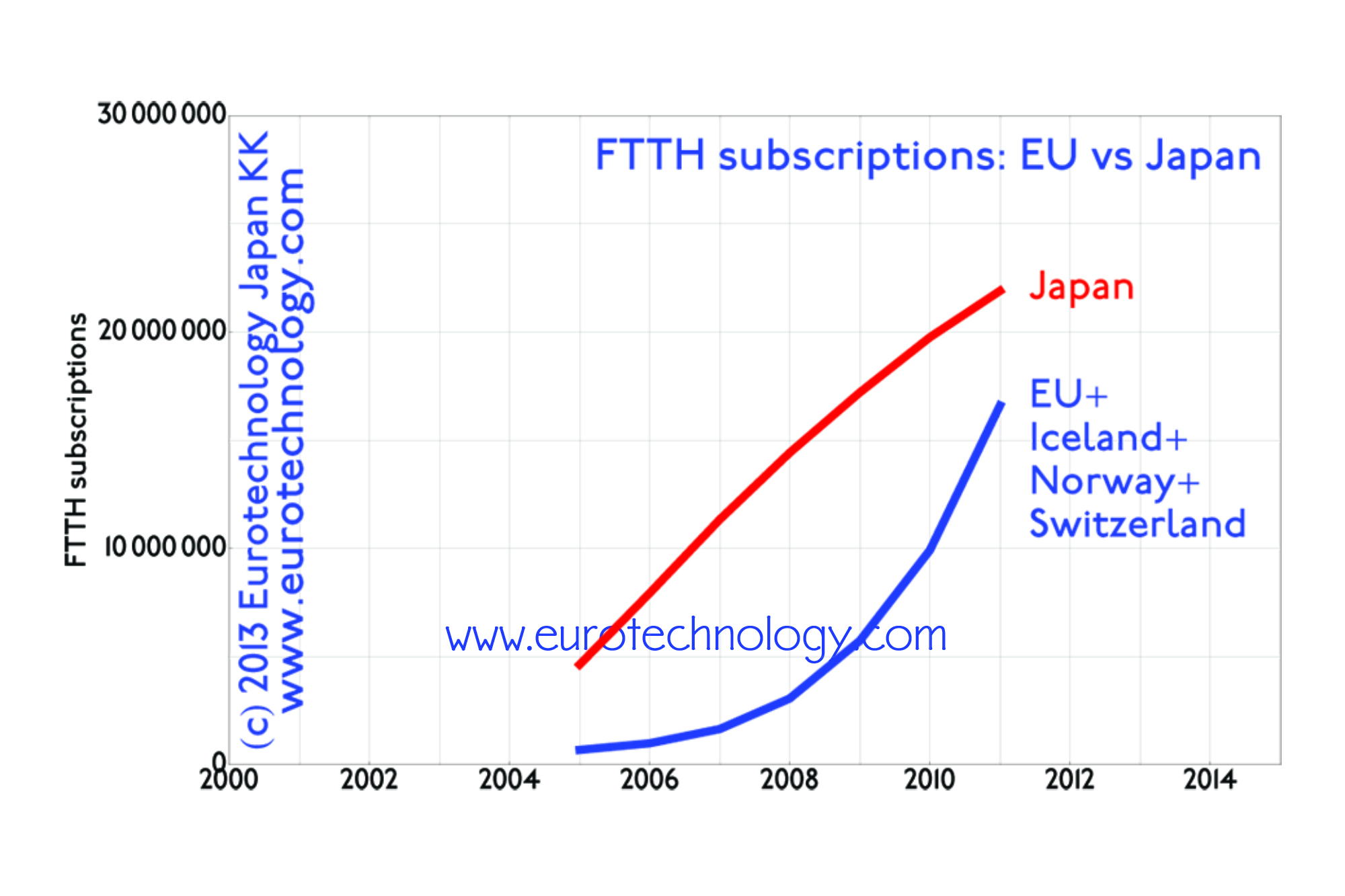

For many years, Japan was the global hotspot for mobile internet, mobile broadband, fixed net broadband (FTTH), there is a very long list of inventions, innovation, new services and products which were successfully brought to market in Japan, and in some cases it took 10 years or longer for these same services to succeed elsewhere in the world.

Examples of services and products which saw their invention, or first successful global mass market introduction in Japan include:

first successful mobile internet services (i-Mode, EZweb, and JSky)

Inventing the mobile internet vs capturing global value

Undoubtedly the biggest success story emerging from Japan’s pioneering mobile internet days is SoftBank

After Vodafone acquired a controlling stake in Japan Telecom, it took Vodafone at least one year to realize that instead of a far east backwater waiting for Vodafone, Japan’s mobile market was actually years ahead of Europe at that time. By the time Vodafone realized that instead of sailing into an easy market, they had actually entered the world’s most ferociously competitive market, it was too late, Vodafone sold its Japan operations to SoftBank, which turned out the failing Vodafone-Japan within a few months of intense efforts. SoftBank’s acquisition of Vodafone-Japan and the successful turn-round became the basis for SoftBank to implement Masayoshi Son’s plan to create one of the world’s most important companies.

Other Japanese success stories resulting from pioneering the mobile internet

Beyond games, Japan has created a vibrant sector of internet and mobile ventures, founded in the wave of Japan’s mobile internet and FTTH broadband adoption. However, because of Japan’s well known Galapagos syndrome, few have made it into global success stories yet. However, its not too late.

eMoji made it into MoMa, and the iPhone.

QR codes are all over China, however not monetized by Denso Wave, the Toyota family company which invented QR codes for automotive parts management.

On 18 July 2016 SoftBank announced to acquire ARM Holdings plc for £17 per share, corresponding to £24.0 billion (US$ 31.4 billion)

SoftBank acquires ARM: acquisition completed on 5 September 2016, following 10 years of “unreciprocated love” for ARM

On 18 July 2016 SoftBank announced a “Strategic Agreement”, that SoftBank plans to acquire ARM Holdings plc for £24.0 billion (US$ 31.4 billion, ¥ 3.3 trillion) paid as follows:

SoftBank’s start in telecoms via the acquisition of Tokyo Metallic, SoftBank’s acquisition of Vodafone Japan in combination with having developed YAHOO-Japan into the leading internet service company in Japan, were among the most important stepping stones for SoftBank to become a key global player in mobile communications.

Masayoshi Son: unreciprocated love for ARM for 10 years

In the Nikkei interview of 3 September 2016, Masayoshi Son explains that he had an “one-sided / unreciprocated love for ARM” for at least 10 years, but decided to acquire SPRINT first. After acquiring SPRINT he had to pay down debt before being able to acquire ARM now.

ARM was founded on 27 November 1990 as Advanced RISC Machines, however the abbreviation ARM was first used in 1983 and initially meant “Acorn RISC Machines”.

Acorn Computers Ltd was founded in 1978 in Cambridge (UK) by Hermann Hauser and Chris Curry to produce computers, and its most famous product was the BBC Micro Computer.

ARM has built an ecosystem of IC design systems and platforms which are at the core of low energy consumption ICs and CPUs for smartphones and many other electronic devices and cars. ARM may become or already is one of the core technology companies for the Internet of Things (IoT).

SoftBank’s ARM Business Department’s name changed to “New Business Department”

The global mobile internet revolution started with Docomo’s i-Mode on February 22, 1999

i-Mode, Happy Birthday!

i-mode menu NTT docomo

Today, exactly 17 years ago, on February 22, 1999, NTT-Docomo launched the world’s first mobile internet service, i-Mode, at a press conference attended only by a handful of people.

NTT-Docomo created the foundation of the global mobile internet revolution, and i-Mode is still a cash-cow for Docomo in Japan, but Docomo did not succeed to capture global value.

i-Mode pioneered many business models, which are today monetized by Apple and Google (mainly via Android).

i-Mode also contributed to make Japan the world’s biggest App market in terms of cash revenues, and helped Japanese app companies to be among the world’s largest and top grossing.

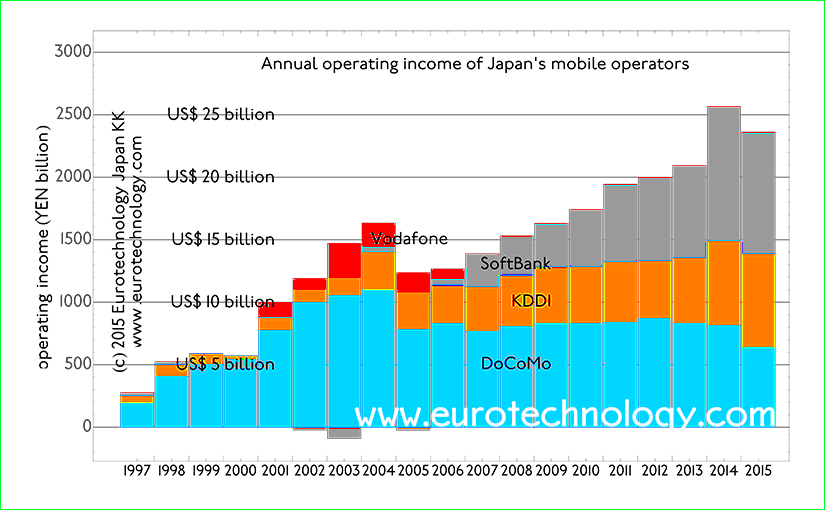

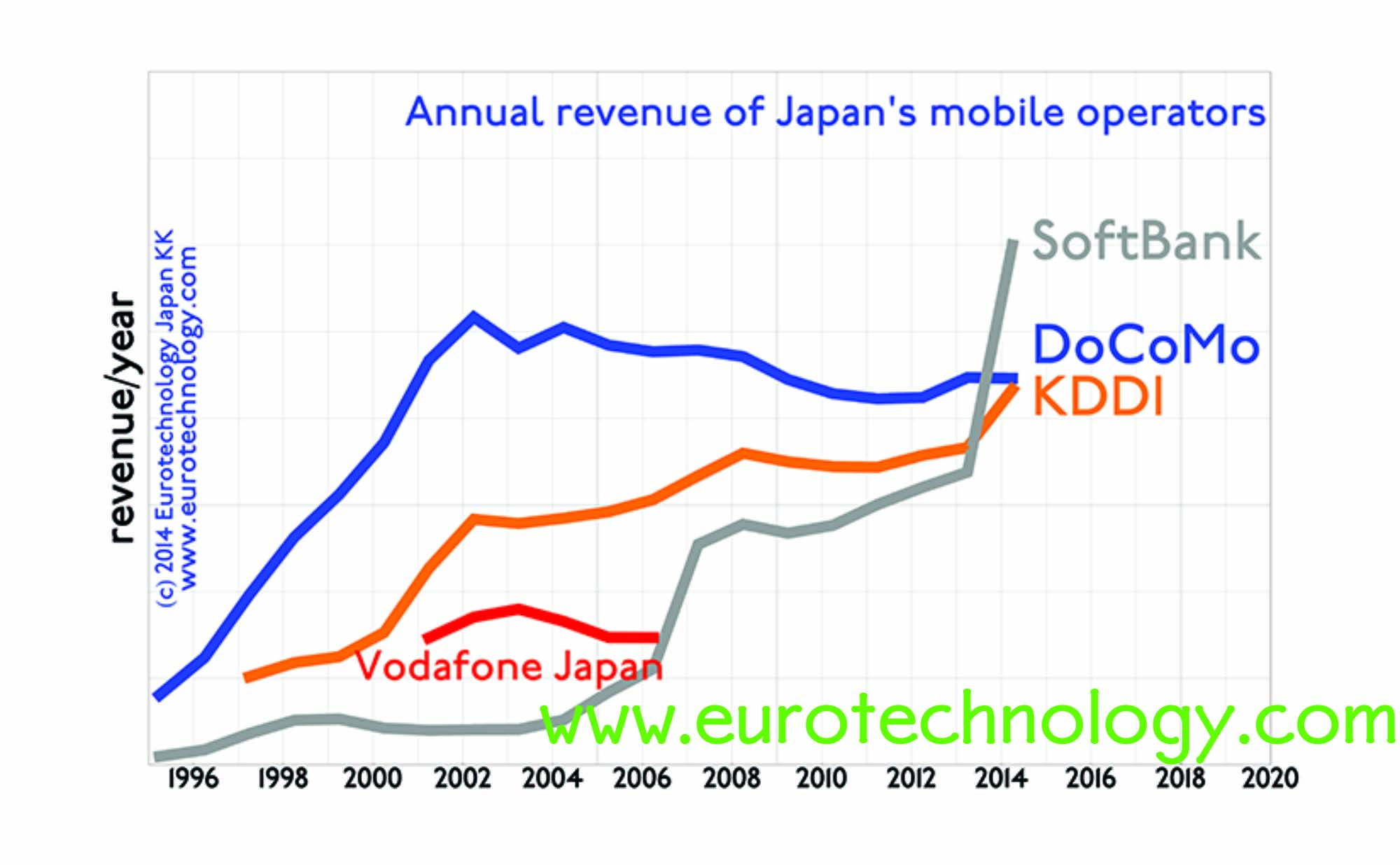

Japan’s mobile telecommunications sector continues to grow

The global mobile internet and smartphone revolution started in Japan in 1999, and Japan’s mobile telecommunications market is the world’s most advanced and most vibrant. Much mobile innovation and inventions, such as camera phones, color screens for mobile phones, mobile apps (i-Appli in Japan), and mobile payments were invented and first to market in Japan.

Globally the first mobile internet started in Japan in February 1999 when NTT-Docomo brought i-Mode to market. NTT-Docomo did not succeed to develop global business based on i-Mode, however, SoftBank took the lead, and is now building a global business built on Japan’s telecommunications sector’s strengths.

To understand Japan’s telecommunications market read our report:

Japan mobile operators grow revenues to over US$ 170 billion in FY2014

While former monopoly operator NTT-Docomo’s business continues to shrink since its peak in 2002, KDDI is growing its predominantly domestic Japanese business slowly but steadily.

SoftBank on the other hand drives rapid growth with domestic Japanese acquisitions (Vodafone-Japan, Japan Telecom, eMobile and Willcom) and overseas acquisitions, which include US operator SPRINT, US mobile phone retailer BrightStar, Finnish game company SuperCell and many others – not to mention SoftBank’s investment in Alibaba.

Japan’s top three mobile operators combined revenues grow to over US$ 170 billion

Operating profits rise to approx. US$ 25 billion in FY2014

Operating profits and net profits are steadily increasing for Japan’s three mobile operators combined.

Former monopoly operator NTT-Docomo’s operating profits peaked in 2002, and have been steadily decreasing since this peak.

Both challengers KDDI and SoftBank on the other hand are growing operating profits steadily: KDDI mainly domestically in Japan, with relatively small global business, while SoftBank has dramatically increased business outside Japan with a series of acquisitions and investments, including US operator Sprint, US mobile phone distributor BrightStar and Finnish game developer SuperCell.

Operating income of Japan’s three mobile operators combined increases to approx. US$ 25 billion

To understand Japan’s telecommunications market read our report:

The mobile internet was born 16 years ago in Japan

Galapagos-Syndrome: NTT Docomo failed to capture global value

On February 22, 1999, the mobile internet was born when Mari Matsunaga, Takeshi Natsuno and Keiichi Enoki launched Docomo’s i-Mode to a handful of people who had made the effort to the Press Conference introducing Docomo’s new i-Mode service. KDDI soon followed with EZweb, and J-Phone with Jsky (J-Phone was acquired by Vodafone, which was unable to manage J-Phone, Vodafone then sold the company to SoftBank).

i-Mode’s popularity soon exceeded any expectation: Docomo for some periods had to limit new subscriptions.

With Steve Jobs’ love for Japan, and Apple’s intense supplier relationships with Japan, its not farfetched to see connections between i-Mode and iPhone, in particular the i-Mode ecosystem and Java-based i-Appli’s are forerunners of today’s apps and apps-ecosystems.

At that time there was no Wikipedia, and Docomo had no English-language website at all, so our company Eurotechnology Japan KK’s information was more or less the only English language information openly available about i-Mode. We were bombarded by requests from many major semiconductor firms, telecom operators, investment banks, students and world-famous business schools for our i-Mode report and related business development and strategic work.

Today 5 of the global top-10 top-grossing Apps are Japanese

While Docomo never managed to capture global value from inventing and first introducing the mobile internet, the No. 1 top-grossing company globally, and five of the top-10 globally top-grossing Apps for iOS and Google-Play combined are Japanese (source: App-Annie).

Japan’s app market is the world’s largest in terms of cash revenues

Its also no coincidence that in terms of cash value, Japan’s is the world’s largest app-market for iOS and Google-Play combined, bigger than the US market and the Chinese market in terms of cash value. (source: App-Annie).

App-Annie’s data to our knowledge only cover the iOS and Google-Play app-stores, not the i-Mode and other mobile internet businesses, so Japan’s actual mobile app economy is even larger than App-Annie data show.

i-Mode is still alive and kicking – and a big business for Docomo

i-Mode is still today the mobile internet system for Docomo’s traditional flip-phones which are still an important part of the market, and recently made headlines since sales for traditional flip-phones were rising, while smartphone sales were (temporarly?) dropping.

i-Mode (and EZweb for KDDI, and Yahoo-mobile for SoftBank) will still be important business for some time to come in Japan.

In business the first-comer does not always win the game

Japan’s NTT-Docomo tested two types of wallet phones, manufactured by Panasonic and SONY with 5000 customers between December 2003 and June 2004, and introduced mobile payments and wallet phones on July 10, 2004 – over 10 years ago.

ApplePay therefore could be developed based on over 10 years of experience with mobile payments in Japan. ApplePay is expected to be introduced for the USA market in October 2014, and we can expect Apple to introduce ApplePay to other markets including Japan in due course.

It will be particularly interesting to see how ApplePay and the already established mobile payment and NFC payment ecosystems in Japan will integrate.

Japan’s Osaifu keitai mobile payments started on July 10, 2004, after public testing during December 2003 – June 2004

Two different types of Docomo‘s “Osaifu-Keitai“, manufactured by Panasonic and by SONY, were publicly tested by 5000 customers between December 2003 – June 2004. Docomo’s Oseifu keitai mobile payment system builds on SUICA NFC stored fare cards, which JR-East brought to market in Tokyo on November 18, 2001, after long years of development and public testing, where the author of this newsletter was one of the testers.

Apple-Pay was developed building on almost 15 years of NFC payments in high volumes in Japan

Therefore, those who wish to make predictions about how the Apple-Pay market is likely to develop can use the experience gained during 15 years in Japan.

There are also some open questions, which will probably be answered after we can all check out Apple-Pay after September 19, 2014. One point which is very important is the speed of transactions – especially in transport applications such as the London or Tokyo Subways – read about this in the next section of this newsletter below.

Read more below, and in our reports on mobile payments and electronic money in Japan:

The speed of NFC mobile payments – and why does it take 10 years to reinvent the wheel? and: what is the speed of Apple-Pay transactions? faster than 100 milliSeconds? or 500+ milliSeconds?

On July 17, 2012 The Wallstreet Journal reported, that as far as Transport for London is concerned, there is no viable mobile payment solution available at this time, because to the knowledge of Transport for London at that time, mobile payment transactions take longer than 500 milli-seconds, which is too slow for Transport for London requirements (e.g at Picadilly station during the rush hour).

Interestingly, in Japan “mobile SUICA” payments have been used in Tokyo successfully since January 28, 2006 at the world’s busiest railway stations including Shinjuku and Shibuya – arguably more busy than Piccadilly Circus in rush hour, with transaction speeds faster than 100 milli-seconds – according to The Wallstreet Journal, London Transport did not even know about this.

Therefore one obvious question we have about Apple-Pay is whether the speed of Apple-Pay transactions is in the 500+ milli-second range – unacceptable for Transport for London, or faster than 100 milli-seconds – as is Tokyo’s state of the art since January 28, 2006… I guess we will soon learn the answer to this question.

Why is it that Japan does not capture the global value which Apple and Apple-Developers will create and capture now?

Japan developed mobile payments, e-cash, credit cards in mobile phones and at least as much functionality as Apple-Pay and an open API and a mobile payment and e-cash developer ecosystem over the last 10-15 years.

Why does Japan leave all the global value on the table for Apple and Apple developers?

Actually, I personally had discussions over the last 15 years will all major players in Japan’s mobile payment and e-cash field, crowned by 1-1 discussions with Docomo’s CEO at that time – Dr. Tachikawa – I wrote about one of these meetings in The Wallstreet Journal, of course without mentioning the details: “Wallstreet Journal leadership question of the week – Japanese leadership“.

Essentially my conclusion at that time, and today is, that Japanese companies never showed any interest at all in developing global business to capture the global value of mobile payments, e-cash and the related businesses. Japanese companies did not even try, and were not even interested in discussing the globalization of mobile payment and e-cash technologies and business models.

All opportunities are not lost of course for Japanese companies in the mobile payments and e-cash fields, but most if not all of Japan’s early-mover advantage has evaporated with Apple-Pay.

In business, sometimes the second or third mover can be commercially more successful than the first mover, and it will be very very hard even for a united Japan Inc to stand up to Apple.

Nokia strengthens No. 1 market position in Japan’s mobile phone base station market!

Japan’s mobile phone base station market

Japan’s mobile phone base station market is about US$ 2.6 billion/year and for European companies Ericsson and Nokia the most important market globally, although certainly also the most difficult one.

Nokia is No. 1 with a 26% market share, and Panasonic is No. 5 with 9% market share.

European investments in Japan

Nokia acquiring Panasonic’s network division is one of many investments and acquisitions in Japan by European companies. For more details, see the EU-Japan M&A register.

Panasonic to focus on core business, Nokia to expand market share in Japan

Panasonic, after years of weak financial performance, is focusing on core business. Nikkei reports that Panasonic is planning to sell the base station division, Panasonic System Networks, to Nokia.

Succeeding in Japan at the second try, learning from initial failure:

We see a pattern here: after failing spectacularly trying to build a mobile phone business in Japan for almost 20 years without success, Nokia is now winning the second time round.

It can be hard for foreign companies to build a business in Japan, and many fail. Interestingly, there is a long list of famous companies that succeed on their second attempt after initial failure, this list includes:

IKEA: failed first time in 1974, succeeds now

DAIMLER: failed spectacularly first time with Mitsubishi Motors, now successful with Mitsubishi Fuso trucks – read the time line here

NOKIA: failed first time after trying for 20 years (1989-2008) to sell mobile phones in Japan, now successful with mobile phone base stations and network infrastructure

Our analysis of Japan’s mobile phone base station market shows, that Nokia became No. 1 in Japan’s base station market with the acquisition of Motorola’s base station division. Acquisition of Panasonic System Networks will expand Nokia’s NSN to expand market leadership in Japan’s mobile phone base station market.

I believe without success in Japan’s mobile phone base station market, there is a big chance Nokia as a company, or at least Nokia’s NSN division would not exist any more at all today.

With a market share of 26%, approx. US$ 700 annual sales in Japan, Nokia is No. 1 market leader in Japan followed by Ericsson on 2nd position. With the acquisition of Panasonic’s base station division, Nokia should be able to expand its market share beyond 26%+9% = 35% and expand its leadership, especially via Panasonic’s deep relationship with Docomo.

Because Docomo with its very deep pockets, is traditionally the first globally to develop and bring to market the most advanced radio technologies, a deeper relationship with Docomo will also help Nokia to develop and bring to market new communication and radio technologies. Thus I believe the impact on Nokia will be far more than an increase of the market share in Japan from 26% to 35%.

Panasonic System Networks

Panasonic System Network’s market share is estimated at around 9% of Japan’s mobile phone base station market, while international sales are essentially non-existent. Thus Panasonic System Network’s global market share is negligible, giving Panasonic little possibility for the scale necessary to operate a stable profitable longterm base station business.

Japan’s mobile phone handset makers and base station makers have for many years focused on serving Japan’s internal market only, and in particular have focused on Japan’s No. 1 mobile phone operators NTT Docomo. This gave Japan’s mobile phone base station makers a temporary home advantage, however with the value shift from hardware to software, they lack scale, and are subsequently uncompetitive globally. More about Japan’s Galapagos effect here.

Over the last 15 years since 1998, Panasonic has shown no growth in revenues, and average net losses of YEN 85 billion (US$ 0.85 billion) per year, as typical for most of Japan’s top 8 electronics companies and as we analyze in detail in our report on Japan’s Electronics Industries.

Panasonic is on 5th rank with about 9% market share in Japan’s mobile phone base station markets, and has little chance and not the capital to scale its base station and mobile phone businesses globally. For Panasonic in it’s current very limited financial situation, focus on core business areas is very prudent.

The context: EU investments in Japan

While Japanese investments in Europe are booming, recently European investments in Japan have been stagnating after Vodafone’s withdrawal from Japan, and there are very few new European investments in Japan. Could it be that Nokia’s investment in Japan starts a new trend of renewed European investments in Japan?

Understand Japan’s telecommunications markets

Report on Japan’s telecommunications industry

(approx. 270 pages, pdf file)

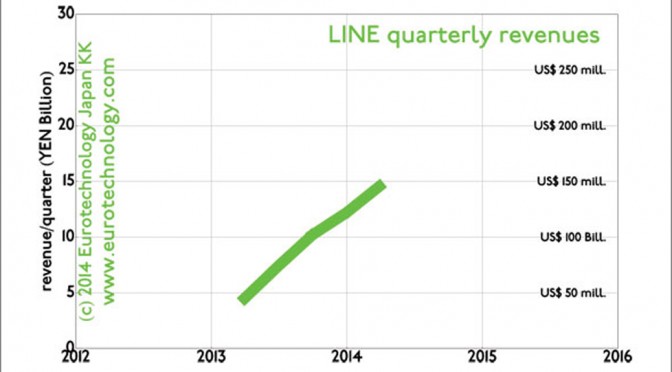

LINE announced quarterly revenues on their website, the revenue data are redrawn below, with approximate US$ amounts shown as well.

Extrapolating assuming continued linear growth, we can estimate expected annual LINE revenues of YEN 70 billion (US$ 700 million) for the full year 2014.

LINE quarterly revenues

Yesterday I was interviewed by Wall Street Journal about future prospects for SONY, and we discussed SONY‘s need for new “killer” products. Considering Facebook’s acquisition of WhatsUp, we thought SONY would need a “killer application” such as LINE. However, since SONY‘s current market cap with US$ 18 billion is of similar size as WhatsApp’s acquisition value, and presumably LINE’s value will be in a similar range. Thus purely theoretically, considering the growth rates of both companies, it would be more appropriate for LINE to acquire SONY than the other way round. Purely theoretically of course.

SoftBank overtakes Docomo and KDDI in all major KPIs

SoftBank presents annual results for the Financial Year which ended March 31, 2014 today, NTT-Docomo and KDDI presented their results a few days ago. Using projections published by SoftBank and using data found in the Japanese business press over the recent days, we have compared SoftBank, Docomo and KDDI financial results:

SoftBank overtook both Docomo and KDDI in all major KPIs: SoftBank’s annual revenues, operating profits and net after-tax profits are higher than NTT-Docomo’s and KDDIs.

The reason for SoftBank overtaking NTT-Docomo and KDDI are both excellent performance of SoftBank’s core businesses, mobile communications and media in Japan, and also a series of recent investments: SuperCell, GungHo, SPRINT, BrightStar, eMobile/eAccess, Willcom and more which all have been very successful investments sofa, not counting Alibaba, which of course is an amazing success story.

Going forward, of course the key questions now are the turn-round of SPRINT, and whether SoftBank can succeed with the much rumored acquisition of T-Mobile in the USA, and possibly also a major European acquisition.

We have today updated our Report on Japan’s telecommunications landscape, to include latest financial and subscriber data, and latest M&A activities: Japan’s telecommunications market is one of the world’s most active also regarding M&A and restructuring.

SoftBank overtakes Docomo and KDDI in Market cap (data for May 7, 2014):

Kaoru Kato, CEO of NTT-Docomo explaining NTT-Docomo’s annual results in Tokyo on April 25, 2014

On April 25, 2014 NTT-Docomo announced annual results for FY2013 (April 1, 2013 – March 31, 2014) and explained the way forward.

Annual revenues are YEN 4461.2 billion (US$ 33.6 billion),

operating income is YEN 819.2 billion (US$ 8.19 billion),

net income is YEN 464.7 billion (US$ 4.6 billion).

These figures are of course amazing results, and Docomo remains one of the most important mobile operators globally.

ensuring that Docomo will remain a leading edge mobile operator for the foreseeable future.

Docomo financial report – announces failure in India:

Still, there are some shadows on Docomo’s amazing success story:

Docomo announced withdrawal from the joint-venture with TATA-Teleservices in India, thus another of Docomo’s ventures to create growth outside Japan has failed. This is the last in a very long string of failures of NTT-Docomo outside Japan, after having lost about US$ 10 billion on investments in KPN-mobile, AT&T-Wireless, and Hutchinson, and the attempt to develop i-Mode mobile internet services in many countries.

NTT-Docomo has now been overtaken by SoftBank on most key performance indicators (KPIs). SoftBank has achieved higher overall subscriber numbers, higher revenues, higher operating income and higher net income than NTT-Docomo.

Kaoru Kato, CEO of NTT-Docomo, bathing the crowd and answering questions at the annual results meeting on April 25, 2014 in Tokyo

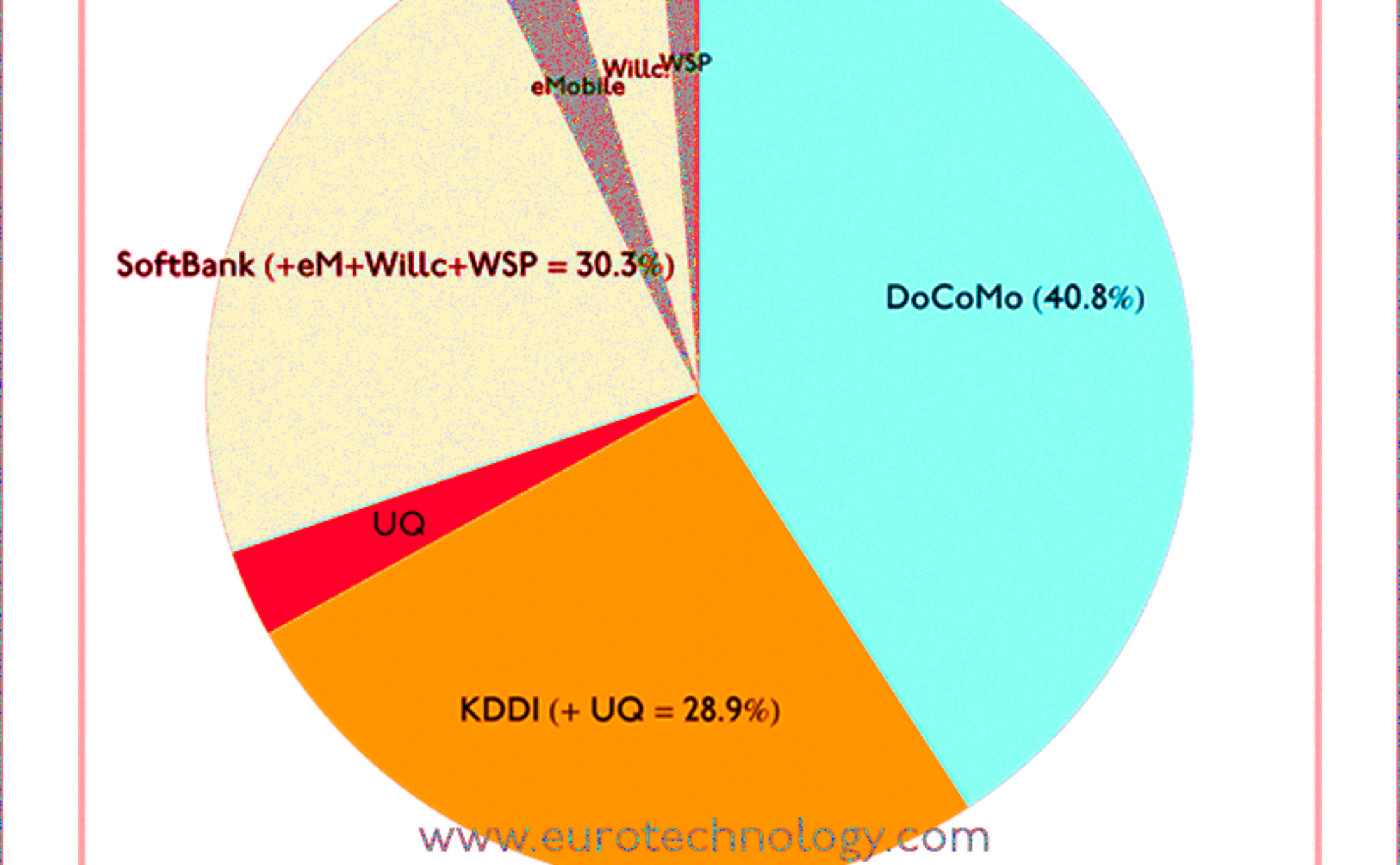

Many press articles get SoftBank market share in Japan wrong

With SoftBank‘s acquisition of US No. 3 mobile operators Sprint and the possibility that Softbank/Sprint will also acquire No. 4 T-Mobile-USA, SoftBank and Masayoshi Son are catching global headlines.

SoftBank market share in Japan: Many media articles report wrong data, because they forget to include group companies

These articles state SoftBank’s market share in Japan’s mobile market as 25% and say that KDDI Group has more subscribers than Softbank Group in Japan, but is this really true?

SoftBank recently acquired eMobile/eAccess, and has been the court-appointed reconstruction partner of Willcom, after Willcom’s financial failure. Therefore eMobile/eAccess and Willcom are also part of the SoftBank group, and SoftBank plans to merge both. In addition, Wireless City Planning (WCP) are also part of the SoftBank group. You will find these transactions, the logic and reasoning behind them explained in great detail in our reports on SoftBank and on eAccess/eMobile.

List of mobile operators on Japan’s market today:

We have the following mobile operators currently in Japan – subscription market shares are shown in brackets (subscriber numbers for Docomo, KDDI and Softbank are as of February 28, 2014, while for other operators the latest officially reported numbers are used):

eMobile/eAccess (note: eMobile, eAccess and Willcom are now combined into Ymobile)

Willcom (now merged into Ymobile)

Wireless City Planning (WCP)

fixed line and other businesses

several virtual mobile operators, e.g. Japan Communications Inc. who lease communications capacity e.g. from Docomo and retail this leased capacity to their own subscribers

The SoftBank group including eAccess/eMobile, Willcom and Wireless City Planning has actually more than 30% of Japan’s mobile subscriber market – not 25% as some articles write.

For detailed market data, statistics and analysis of Japan’s highly competitive mobile communications market, read our market report on Japan’s telecom markets, which includes analysis and data for Japan’s wireless, fixed, ADSL and FTTH markets, and detailed financial data, analysis, and comparison of the financial performance of NTT, NTT Docomo, SoftBank and KDDI.

We are also preparing reports on Japan’s cloud and data center markets –

Subscriber market shares in Japan’s wireless communications markets for each of the competing groups: Docomo, KDDI and SoftBank.

Learn more about SoftBank, Masayoshi Son, and his 30/300 year vision for SoftBank

VCSEL inventor Kenichi Iga: hv vs kT – Optoelectronics and Energy

(Former President and Emeritus Professor of Tokyo Institute of Technology. Inventor of VCSEL (vertical cavity surface emitting lasers), widely used in photonics systems)

VCSEL: how Kenichi Iga invented Vertical Cavity Surface Emitting Lasers

My invention of vertical cavity surface emitting lasers (VCSEL) dates back to March 22, 1977. Today VCSEL devices are used in many applications all over the world. I was awarded the 2013 Franklin Institute Award, the Bower Award and Prize for Achievement in Science, “for the conception and development of the vertical cavity surface emitting laser and its multiple applications in optoelectronics“. Benjamin Franklin’s work is linked to mine: Benjamin Franklin in 1752 discovered that thunder originates from electricity – he linked electronics (electricity) with photons (light). After 1960 the era of lasers began, we learnt how to combine and control electrons and photons, and the era of optoelectronics.

If you read Japanese, you may be interested to read an interview with Genichi Hatakoshi and myself, intitled “The treasure micro box of optoelectronics” which was recently published in the Japanese journal OplusE Magazine by Adcom-Media.

Electrons and photons

Who are electrons? Electrons are just like a cloud expressed by Schroedinger’s equation, which Schroedinger postulated in 1926. Electrons can also be seen as randomly moving particles, described by the particle version of Schroedinger’s equation (1931).

Where does light come from? Light is generated by the accelerated motion of charged particles.

Electrons also show interference patterns. For example, if we combine the 1s and 2p orbitals around a nucleus, we observe interference.

In a semiconductor, electrons are characterized by a band structure, filled valence bands and largely empty conduction bands. The population of hole states in the valence bands and of electrons in the conduction bands are determined by the Fermi-Dirac distribution. In typical III-V semiconductors, generation and absorption of light is by transitions between 4s anti-bonding orbitals (the bottom of the conduction band) and 4p bonding orbitals (the top of the valence band).

In Japan, we are good at inventing new types of vertical structures:

in 607, the Horyuji 5-Jyu-no Toh (5 story tower) was built in Nara, and today we have progressed to building the 634 meter high Tokyo Sky Tree Tower.

in 1893, Kubota Co. Ltd. developed the vertical molding of water pipes

in 1977 Shunichi Iwawaki invented vertical magnetic memory

in 1977 Tatsuo Izawa developed VAD (vapor-phase axial deposition) of silica fibers

in 1977 Kenichi Iga invented vertical cavity surface emitting lasers (VCSEL)

Communications and optical signal transmission

History of communications spans from 10,000 years BC with the invention of language, and 3000 BC with the invention of written characters and papyrus, to the invention of the internet in 1957, the realization of the laser in 1960, the realization of optical fiber communications in 1984, and now since 2008 we see Web 2.x and Cloud.

Optical telegraphy goes back to 200 BC, when optical beacons were used in China: digital signals using multi-color smoke. Around 600 AD we had optical beacons in China, Korea and Japan, and in 1200 BC also in Mongolia and India.

In the 18th and 19th century, optical semaphores were used in France.

In the 20th century, optical beam transmission using optical rods and optical fiber transmissions were developed, which combined with the development of lasers created today’s laser communications. Yasuharu Suematsu and his student showed the world’s first demonstration of optical fiber communications demonstration on May 26, 1963 at the Tokyo Institute of Technology, using a He-Ne laser, an electro-optic crystal for modulation of the laser light by the electrical signal from a microphone, and optical bundle fiber, and a photo-tube at the other end of the optical fiber bundle to revert the optical signals back into electrical signals and finally to drive a loud speaker. For his pioneering work, Yasuharu Suematsu was awarded the International Japan Prize in 2014.

VCSEL: I recorded my initial idea for the surface emitting laser on March 22, 1977 in my lab book.

Vertical Cavity Surface Emitting Lasers (VCSEL) have many advantages:

ultra-low power consumption: small volume

pure spectrum operation: short cavity

continuous spectrum tuning: single resonance

high speed modulation: wide response range

easy coupling to optical fibers: circular mode

monolithic fabrication like LSI

wafer level probe testing

2-dimensional array

vertical stack integration with micro-machine

physically small

VCSEL have found applications in many fields, including: data communications, sensing, printing, interconnects, displays.

As an example, the Tsubame-2 supercomputer, which in November 2011 was 5th of top-500 supercomputers, and on June 2, 2011 was greenest computer of Green500, uses 3500 optical fiber interconnects with a length of 100km. In 2012: Too500/Green500/Graph500

IBM Sequoia uses 330,000 VCSELs.

Fuji Xerox introduced the first demonstration of 2 dimensional 4×8 VCSEL printer array for high speed and ultra-fine resolution laser printing: 14 pages/minute and 2400 dots/inch.

VCSEL photonics started from minor reputation and generated big innovation. VCSELs feature:

low power consumption: good for green ICE

high speed modulation beyond 20 GBits/second

2D array

good productivity due to monolithic process

Future: will generate ideas never thought before.

em. President of Tokyo Institute of Technology, Professor Kenichi Iga, inventor of VCSELGerhard Fasol (left), em. President of Tokyo Institute of Technology, Professor Kenichi Iga (right)

AppAnnie showed that in terms of combined iOS AppStore + Google Play revenues, Japan is No. 1 globally, spending more than the USA. Therefore Japan is naturally the No. 1 target globally for many mobile game companies, and 10 out of 25 top grossing apps in Japan are of foreign origin!

Many foreign game companies have failed and given up. Foreign game companies that have recently given up in Japan include Zynga and Habbo Hotel. EA has given up twice, and is now undertaking the third entry to Japan. To understand some of the key mistakes foreign companies make in Japan, read our blog about why Vodafone failed in Japan.

Lets have a look at the list of top grossing games in the Apple iOS AppStore today. Out of the 25 top grossing games in the AppStore, 10 are by foreign originating companies. Can you guess which these are by reading the list below?

So Japan is certainly not a “closed market”. Actually, it is obvious that Apple does not discriminate in any way against foreign companies in Japan.

Interestingly, neither Nintendo, nor Rovio’s games, such as Angry Birds appear among the 200 “top grossing games” in Apple’s iOS Japan AppStore.

Apple iOS AppStore-Japan “Top Grossing” games ranking – 10 out of the 25 top grossing apps in Japan are by companies of foreign origin

Can you guess which 10 are by companies of foreign origin?

Social media revolutionize brand marketing: people don’t want to be told what to buy, but want to discover and share

Social media marketing: Consumers have now taken control of what they watch, read and listen to and so the messages they receive are the ones they chose to receive. Brands must now deserve that attention through appealing to their needs and feelings and not simply by buying airtime on television.

Ray Bremner, President & CEO of Unilever Japan gave a talk at Waseda University

To understand Japan’s media landscape read the “Japan’s media” report.

Social media marketing (Ray Bremner, President & CEO, Unilever Japan)

From Advertising to consumers to mattering to people

My key take-away is that social media have made the top-down “begin told” way of advertising obsolete, and replaced it by finding, sharing and engaging.

About Unilever:

Unilever was founded in 1929 by the merger of the British soap maker “Lever Brothers” (founded in 1885 by William Hesketh Lever, The Right Honourable The Viscount of Leverhulme), with the Dutch margarine producer “Naamloze Vennootschap Margarine Uni”, which was formed by the merger of several margarine companies, including those of Antonius Johannes Jurgens and Samuel van den Bergh. Soap brought hygiene to ordinary people, and margarine helped people who could not afford butter. Both companies, Lever and Margarine Uni had in common that they used palm oil as raw material.

The merger of Lever and Margarine Uni was decided over dinner in London in 1929, and written down in a 100 word merger agreement – unthinkable today for an M&A agreement.

About 50% of Japanese people have Unilever products at home

Unilever vision 2010 is: double the business, while reducing the environmental footprint. Execution of this vision is measured by 60 KPIs and the results are published.

Unilever vision:

We work to create a better future every day.

We help people feel good, look good, and get more out of life with brands and services that are good for them and good for others. We will inspire people to take small everyday actions that can add up to a big difference for the world.

We will develop new ways of doing business that will allow us to double the size of our company while reducing our environmental impact.

Unilever mission: building brands that improve people’s lives.

Ray Bremner, President & CEO of Unilever Japan: Social Media is revolutionizing the way we market brands

Ray Bremner: “social media are revolutionizing the way we market brands, and they are making people like me extinct”.

From 2001 to 2013, the average time Japanese consumers spend watching TV has decreased from about 3 1/2 hours/day to 3 hours/day, while the time spent with PC & mobile has tripled from 1/2 hour/day to 1 1/2 hours per day. Most Japanese age groups use social media, usage peaks at 35% for men in their 20s, and around 45% for women in their 20s, and around 30% in their 30s.

TV reaches about 88% of Japan’s population, and digital media (PC and mobile) reach about 73%.

From 2001 to 2012, advertising expenditure in Japan has decreased from about US$ 27 Billion/year to US$ 23 Billion/year, while expenditure for digital media has increased from zero to US$ 12 Billion/year. For an overview of Japan’s media markets – see “Japan’s Media“.

How to make marketing messages a pleasure rather than annoying?

How do we succeed? Crafting brands for life.

Put people first, not just consumers. Real people with real lives.

Build brand love.

Unlock the magic.

The brand love triangle

How do you create a conversation people want to participate in?

We use the “brand love triangle. “The people we serve” are in the center. The three edges of the brand love triangle are:

Purpose (brand point-of-view) <— brand history dive

Product truth <— product dive

Human truth <— people immersion

Ray Bremner, President & CEO of Unilever Japan: Real people with real lives

“Dove Real Beauty Sketches” by Steve Miles

Brands need a purpose, a point of view. Before 2002 Dove did not have a purpose.

Steve Miles talking about Dove and himself:

93% of women do not think they are beautiful – men are opposite: 93% of men think that they look just great. Dave Miles (and Dove’s) point of view is that everyone is beautiful. This point of view is expressed in “Dove Real Beauty Sketches”, which won the Titanium Grand Prize and 10 Gold Lions at Cannes 2013:

As of today, “Dove Real Beauty Sketches” has 61,767,827 views on YouTube, which is not as much as PSY’s Gangnam Style with 1,888,086,686 views, but still – pretty amazing.

Another example of brand communication is Harley Davidson, which signifies “Freedom of the Road”, independent character. Harley Davidson creates a bond to customers by presenting each customer with the “umbilical cord”, the belt with which the Harley Davidson motor bicycle was tied down during the transport from the factory to the customer.

Focus: In 2000, Unilever had 1600 brands and today 400 brands.

Q&A

Question: How many of your campaigns in Japan are global campaigns? How many are Japan-only?

Answer: practically all campaigns for all international brands of any company are made in Japan for Japan. That is not to say that global ideas do not work. In fact in most cases International Brands have the same brand and advertising positioning in Japan as elsewhere in the world. What does differ for Japan is that often Japanese consumers have different usage habits, have different views about the world and the cues within the advertising can leave different impressions on Japanese minds. The Japanese consumer is highly observant of small details in advertising ; much more so than the average European for example.

That means that we test Global campaigns but very often we have to create Japan only executions so that how we express the idea is done totally with the Japanese consumer in mind. This is more costly and time consuming but essential for success.

On Thursday January 16th, 2014, NTT Docomo announced the postponement of mobile phone handsets based on the TIZEN operating system. This is actually the second time that NTT Docomo has postponed the planned introduction of TIZEN handsets, so it might become doubtful whether NTT Docomo will ever introduce TIZEN handsets.

In the announcement NTT Docomo essentially said that with the current market situation in Japan, it makes no commercial sense for Docomo to introduce a third smartphone operating system to the market.

The French journal Les Echos interviewed me about Docomo’s repeated postponement of TIZEN OS handsets. Here some notes I wrote up to prepare for the interview:

Both for handset makers like HTC or Samsung and it would be a dream to become independent of OS owners/controllers like Microsoft or Google, and for mobile operators like Orange or Docomo, it would be a dream to have an OS they can control, and where they can introduce their own services like Docomo’s “iconcier” personal digital assistant, which is to some extent competing with Apple’s SIRI and with various Google services. Its a dream but realization is a different story. Its not enough to make and further develop and maintain the full OS stack including UI, create a development environment and SDKs as easy to use and competitive with Apple’s and Google’s, app stores, build a developer community who create lots of apps. Its also necessary to make a critical mass of attractive devices, gain a critical mass of market share, create global scale, and most importantly win over all the most important Apps like Facebook, LINE, etc.

With the dramatically increasing complexity and sheer size of software, it becomes harder to bring mobile services to market without global scaleability, or at least a major part of the world, which usually will need to include China. Docomo does not have this global scale, so it will become harder and harder for Docomo to introduce own software services, such as iMode or iConcier.

Docomo has continuously lost market share and recently even net subscribers, and in December for the first time in recent memory succeeded to gain top position in subscriber gains, surely because of the iPhone. In addition, rumors are that Apple demands very high minimum sales shares of operator partners. So Docomo is under double pressure:

to satisfy contract conditions with Apple

to maintain subscriber gains

in addition, Docomo still has a substantial part of “iMode-keitai”, also called “galake” (= “Galapagos keitai”). So Docomo already has a large variety of OS and handset styles, and has recently reduced the number of different handset it supports, so going to Tizen would go against this trend.

Its not the end of Tizen. Tizen can in addition to smartphones also go into embedded applications such as cars, elevators, washing mashines etc.

Ericsson held the Mobile Business Innovation Forum in the Roppongi Hills Tower in Tokyo on October 31 and November 1, 2013 delivering a great overview of the push and pull of the mobile communications industry: technology push, M2M and user pull, as well as how the mobile operators between technology and users can best make customers happy and at the same time monetize their investments, while “Over The Top” (OTT) new comers (Google, YouTube, Amazon.com, Facebook, Twitter and others) seek to disrupt the good old telecommunications world.

Here some key take-aways, read more below:

About 50% of global smartphone, mobile phone and mobile broadband subscriptions are in Asia-Pacific, making Asia-Pacific the most important region in the world, and Japan one of the most important LTE markets.

Switch from voice to data is a differentiator: forerunner telcos see rapid growth (10-12% CAGR) for both revenues and EBITDA over the period 2008-2013, while average telcos see stagnation. The key for telcos is to be a forerunner, rather than an average stagnating telco.

Many products such as XBOX or Apple’s SIRI are linked via networks to a data center. Networks and data centers are disruptive innovation for games and many other sectors. Maybe cars as well.

Open source is coming to software defined networks (SDN), the OpenDayLight community develops software for software defined networks.

Software defined networks create virtualized networks, SDN support “network slices” for different applications. API’s open SDNs to users.

Manufacturers and other industries have rationalized a long time ago, telcos have not yet rationalized, creating big opportunities.

LTE Markets – 5 out of 10 top LTE markets globally are in Asia-Pacific, and the top 3 are in Asia-Pacific (however this table shows the percentage penetration, does not reflect market size. In terms of market size, Japan is doubtlessly No.1:

Mobile communications will dwarf the PC-world. By 2018 we will expect to have:

PCS and tablets: 260 million in APAC (31%) vs 850 million globally

smartphone subscriptions: 2.2 billion in APAC (49%) vs 4.5 billion globally

mobile broadband subscriptions: 3.5 billion in APAC (50%) vs 7 billion globally

mobile phone subscriptions: 4.5 billion in APAC (50%) vs 9 billion globally

Katsuya Watanabe, Deputy Director General, Information and Communications Bureau, Japan’s Ministry for Internal Affairs and Communications (MIC)

Katsuya Watanabe (Charley K Watanabe): ICT Growth Strategy for Japan

Deputy Director-General, Information & Communications Bureau, Ministry of Internal Affairs and Communications (MIC), Japan

Government of Japan – IT Strategic Headquarters: The new internet world had a relatively slow start in Japan. In January 2001 the e-Japan Strategy was formed with the target for Japan to become the world’s most advanced IT nation by 2005, and the IT Strategic Headquarters where formed. In January 2006 the New IT Reform Strategy followed, and in July 2009, the i-Japan Strategy 2015.

The Ministry of Internal Affairs and Communications (MIC) formulated the u-Japan Policy in December 2004, followed by the x-ICT Vision in July 2008.

With the change of Government in September 2009, the New Strategy in Information and Communications Technology formulated.

With the advent of Prime Minister Abe’s Government in December 2012, in June 2013, the new IT Strategy was formulated: “The world’s most advanced IT nation creation”, by the Council on ICT Strategy and Policy for Growth, which was set up in February 2013.

The Ministry focuses on the following trends: Big Data, Sensor Networks, Cloud Computing, and smart phones.

Mission: to be the most active country in the world.

Vision:

Creating new value-added industries

Solving social problems

Improving and strengthening common ICT infrastructure

Issues: economic growth, employment, information transmission capacity, development of cities, super-aging society, resource problems, open innovation, cybersecurity, utilization of personal data

Prioritized projects are:

Creating new value-added industries:

data utilization

broadcast and contents

agriculture

local revitalization

Solving social problems:

Disaster prevention

Medical, nursing, health care

Resources

local revitalization

Mr Watanabe introduced several industry-academia-government collaboration projects addressing these priority issues. The economic effects by 2020 of creating new industries stimulated by these government programs are estimated as follows:

super-aging society sector: 23 trillion yen (US$ 230 billion)

geospace sector: 62 trillion yen (US$ 620 billion), from today’s 20 trillion yen (US$ 200 billion) market size

A further program is the creation of ICT Smart Towns in Japan, especially also to build towns resilient against disasters.

John Rossant: A people-centric vision for future cities

Founder and Chairman of New Cities Foundation

By 2050, around 70% of the world’s population is expected to reside in urban areas.

Mobile applications transform cities, and in the ideal case create “people centric cities”, an example: AppMyCity!

Panel “Society in transformation”(left to right): Mats Olsson (Ericsson), Katsuya Watanabe (MIC), John Rossant (New Cities Foundation), Douglas Gilstrap (Ericsson)

Business in transformation

Jan Signell, Head of North East Asia and member of Ericsson Global Leadership Team

Jan Signell: Ericsson in Japan, China, S-Korea

Head of North East Asia Region, President of Ericsson-Japan

The first Ericsson distributor travelled to Japan in 1894 – more than 100 years ago.

Super high smartphone penetration and usage in Japan+China+S-Korea: Japan has 76% smartphone penetration, 49% of Chinese make purchases on their smartphone every week, networks have to be prepared.

Hiroyasu Asami, Managing Director of Smart-Life Business Division, NTT-DOCOMO

Managing Director of Smart-Life Business Division, NTT-DOCOMO

NTT-DOCOMO aims to be the customer’s partner for smart-life.

In the transition from traditional feature phones to smartphones including tablets, NTT-DOCOMO sees a new potential market emerging: video, shopping, books, services and contents are booming.

The center of the mobile eco-system (and value creation) is shifting to higher layers.

NTT-DOCOMO seeks effective utilization of its business assets:

Postpaid subscriptions (99.7% postpaid)

VAS sales at mobile shops: DOCOMO has 2,400 carrier DOCOMO branded shops

Handset control: DOCOMO sells handsets with value added services (VAS)

DOCOMO seeks to create new markets in 8 business areas:

Commerce

Finance/payment

Health care/education

M2M

Safety/security

Environment/ecology

Aggregation/platform

Media/content

The basic concept is to bring smart life into reality, and to become a smart life partner. To improve customer satisfaction and to improve corporate value.

DOCOMO is in the process to transition from the traditional i-Mode and i-Menu services on feature phones, to d-market and d-menu for the multi-OS environment (with Google/Android, Tizen, iOS and other OS).

Revenues from new business of DOCOMO increased from US$ 4 billion (FY2011), to US$ 6 billion (FY2012) and is expected to increase to US$ 11 billion by FY2015.

About 300 parties participate in Japan’s ITS programs, lead by the ITS Promotion in the Cabinet office of Japan.

Major cooperative projects are:

ASV-5 (V2V, V2P) by the Ministry for Land and Infrastructure and Transport MLIT

Joint research (V21) by MLIT and NILIM

DSSS/Green wave (V21) by the Nation Police Agency

Key issues are:

Standardization

Common hardware

hybrid communication

sustainable business model

positioning technology

Key targets are to achieve fatality rates below 2500 by 2018, and to reduce traffic congestions to one-half by 2020 compared to 2010.

Honda develops autonomous driving with the aim to realize “the joy of mobility” with safety and freedom.

The vision: As Japan aiming for the safest transportation in the world, we hope to deploy cooperation system in collaboration with government and car OEMs, in four phases. Phase 1: basic services Phase 2: advanced services Phase 3: integrated services Phase 4: autonomous services

Panel (left to right): Akira Yamaguchi (Orient Corporation), Hiroyasu Asami (NTT-DOCOMO),Masashi Satomura (Honda), Jan Signell (Ericsson)(Ulf Ewaldsson, CTO, Ericsson

Ulf Ewaldsson

CTO, Ericsson

A perfect storm:

Network coverage and quality is good enough

Business models make data affordable

App-centric services become mainstream

Smartphone penetration is reaching critical mass

however, for mobile operators there is a HUGE difference between the frontrunner’s revenue and EBITDA growth compared with stagnant revenue/EBITDA for average operators. Key for mobile operators is to be strongly growing frontrunner – not a stagnating average operator.

To move from an average no-growth operator to a fast-growing frontrunner, a mindshift is needed from:

problem focus to opportunity focus

maximizing old revenues to innovating new revenues

connectivity as a commodity (“dumb pipe”) to connectivity as differentiator

from tech silos to tech synergies

Ericsson uses six growth codes:

“Streetwise metrics”, experience centric KPIs

“Show casing”: quality led marketing

Redefine subscription: “unboxing”

Open-ended innovation: “ecosystematic

Visionary collaboration: “co-partnering”

Visionary investing: “gap minding”

Yung-Ha Ji, Head of Network Strategy Dept., KT Corporation

Yung-Ha Ji: How to migrate to future ICT network

Head of Network Strategy Department, KT Corporation

In the IDI/ICT Global Development index ranking, S-Korea ranks 1st globally for broadband, while the Scandinavian countries rank 2nd, 3rd, 4th and 5th, and Japan ranks 8th, followed by UK on place 9.

kt will cover 99% of S-Korea’s population with LTE network based on 20MHz Bandwidth in the 1.8GHz band. With the BenchBee speed test, download speeds of 44 Mbps are achieved with a Category 4 LTE-A phone.

kt saw explosive growth of data traffic: 350 times increase over the 4 years from January 2009 to September 2013. Monthly data usage is 2.2Gb for LTE and 1.2Gb for 3G phones. Total data traffic is about 20,000 TeraBit/Month in September 2013.

kt has the world-first LTE network using virtualization cloud technology.

kt introduced a series of services including Web-enabled IPTV, Giga-Internet FTTH premium services, olleh TV mobile, LTE broadcast, “Total Advertising Open Community” (TAOC) – using targeting of advertisements to differentiate from OTT operators.

Example of an innovative service: if you click an advertisement and watch an ad, you are rewarded with increased transmission speed.

Akira Yamaguchi: Mobile payment systems in Japan

Exec Officer Retail finance and credit cards, Orient Corporation

Jakob Navok, Director of Business Development, Square Enix

Jacob Navok: Games over the network

Director of Business Development, Square-Enix

Games are the ultimate application! Worldwide game industry revenues are US$77.4 billion in 2013, adding all segments from retail hardware to software and services.

Hardware used to be the driver in the past, but today the network drives everything, and networks bring disruption to game design, business models (“free-to-play” is a marketing model – not a business model). Business models include: micro transactions, subscriptions, advertisements and digital pricing.

Marketing disruption include: “free-to-play”, cross-promotional networks, and app-stores.

Video had a dramatic impact on networks, but games have not.

Interactive media bring the next revolution: SONY acquired Gaikai (US$ 400 million), and Microsoft announced Xbox Cloud services (US$ 700 million).

Server side rendering and developer innovation will create game demand on many devices.

Speed is key!

Dan Simmons, Reporter and Producer, CLICK, BBC

Dan Simmons

Reporter and Producer, CLICK, BBC

Dan Simmons showed how smart phones are a second screen accompanying movies, PCs and TV. 60-80% of Americans use a second screen, and 46% use a smart phone.

Eyeballs move to iPads… the question is: who owns the second screen!

CBS made US$ 10 million off advertising, but advertising ads during superball on the internet – not on TV!

TV is about raising emotions, and feedback at the moment, immediate feedback is incredibly valuable. A 2nd screen can give a 360 degrees view.

Dan mentioned the APP-movie, where visitors to the movie theatre downloaded an App to their smartphone and received message to their App during the movie. The messages need to be frame-accurate, and today’s networks are not good enough to ensure frame-accuracy. People with smartphones and using the App knew who the murderer was at 65 minutes into the movie, while visitors without smartphone and App had to wait until 80 minutes into the movie before they know who the murderer was. Initially it was thought that this could be a problem, but it turned out to be a positive part of the enjoyment for the audience. A further attraction was, that visitors could keep the App on their smartphone, and the movie owner could reach viewers long after the performance was over, and they had long left the movie theatre, keep the contact, and potentially create follow-on business.

Panel (left to right): Dan Simmons (BBC), Jacob Navok (Square-Enix), Ulf Ewaldsson (Ericsson), Yung-Ha Ji (KT Corporation)Adrian Ionel, CEO, Mirantis

Shoji Nemoto: Our mission is to fulfill & inspire the desires of users

Question: 3D-TV failed. How can we know that 4k-TV will be successful?

Shoji Nemoto: 3D is not only a consumer product. 4k-TV also has industrial applications, such as telemedicine and other medical applications. SONY cooperates with Olympus for medical applications.

Adrian Ionel

CEO, Mirantis

Today for every new product you need a network and a data center:

SIRI: Apple invested US$ 1 billion in a data center

X-BOX: Microsoft built a data center

Open source is extremely powerful vs closed systems:

opensource is created by users, users are involved from the beginning and users are extremely powerful

Open: anybody can contribute

Closed source vs open source:

closed source: traditional hierarchical industrial structure, waterfall model, top-down

open source: works like nature, social network, meritocracy and transparency, very different to traditional industrial structure

Examples for open source: Linux, JAVA, Big data.

Open source creates new business models. Facebook, Google, Amazon.com are only possible with open source. Gigantic data centers are only possible with open source.

Most major players invest in open source.

Taro Kodama, Country Growth Manager, Facebook Japan

Taro Kodama

Country Growth Manager, Facebook Japan

No. 1 Facebook employee in Japan.

“We can’t just copy what we did in Japan – we must reinvent in Japan”

Facebook’s complacency about mobile is surprising. Its this kind of complacency that kills companies (Forbes.com, February 2012)

Facebook’s future is in mobile. Mobile is THE strategy for Facebook (Forbes.com, May 2013)

Facebook: over 874 million users on mobile, 49% of revenue is now generated from mobile, up from 0% last year.

Internet traffic is shifting to mobile: 13% of global internet traffic is on mobile.

Panel (left to right): Ulf Ewaldsson (Ericsson), Adrian Ionel (Mirantis), Taro Kodama (Facebook)

Innovation and technology evolution

Ulf Ewaldsson, CTO, Ericsson

Ulf Ewaldsson: “Transforming networks

CTO, Ericsson

We see cities as organisms.

Trendspotting:

scarce spectrum

simplicity and automation

continued traffic growth

from nodes to systems

mobile entreprise

blurring of IT and telecom

Concept of “Network slices”:

Network performance needs depend on industry, beyond just smartphones.

A matrix of industry needs covering the following industries: cars, processing, utilities, transport, media, and NSPS, healthcare etc. Which have different needs for: throughput, latency, QoS, volumes, coverage, capacity, security and location.

A common network platform includes dynamic and secure “network slices” with different specifications for different industries and applications.

Three new products:

Ericsson Radio Dot System

SDN on a chip: SNP 4000

Cloud on a blade: Ericsson Cloud System

Technology in-depth sessions

Erik Ekudden, Head of Technology Strategies, Ericsson

Network Slices: Service Provider (SP) Software Defined Networks (SDN), Network Functions Virtualization (NFV) and Cloud

Erik Ekudden

Head of Technology Strategies, Ericsson

Service Provider based Software Defined Networks (SP SDN) are on the way to deployment. The path to deployment includes: technology, business model development and operations. Currently we are still midway in the technology development phase, business model development is in the early phase, and we are just before operations and deployment.

Network functions are virtualized in the DC/cloud infrastructure. Functional layers of the network are virtualized, and networks become open to developers.

Networks are elastic and we have “network slices” for different applications.

OpenDayLight

Ericsson is leading participant/founder in the open source “OpenDaylight” LINUX community, the first release of the Hydrogen Code was on September 13, 2013. OpenDayLight is an open source community developing software-defined networking (SDN).

Daniel Ehrenstrahle, Head of Strategy & Portfolio, BU Networks, Ericsson

Connecting the dots in the Networked Society

Daniel Ehrenstrahle

Head of Strategy & Portfolio, BU Networks, Ericsson

Business cases and clear rationale why technology is introduced is necessary.

We need to redefine how network performance is defined: “app coverage” defines network performance not in terms of technical data alone, but in terms of usability of each app. App coverage for video will be different than for voice, or low intensity data applications.

70% of usage is indoors, therefore we need indoor coverage, and Ericsson does not believe in Femto-technology, and introduces the Radio Dot System. Launch will be in 2H 2014 for 3G and 4G and for WiFi later. Up to 4 channels per unit.

Component based architecture: AIR = antenna integrated unit SSR = Edge router

Ericsson “DOT”Ericsson Radio “DOT” System: RJ45 Antenna Mounting Unit and Active Antenna Element taken apartEricsson “DOT” system, RJ45 connector socket

Monetizing the network assets

Beau Atwater

Head of Strategy and Business Intelligence, BU Support Solutions, Ericsson

Tomas Ageskog, Head of Consulting and Systems Integration, BU Global Services, Ericsson

Business Transformation – Ericsson Consulting and System Integration (SI)

Tomas Ageskog

Head of SI Core, IP & Media, Ericsson

Manufacturing and other industries have rationalized decades ago. Telcos are not yet rationalized.

OSS/BSS need to be good and fast to make money.

A revolution will happen in the broadcast space when processes are being rationalized.

In Australia, Telstra spent US$ 1.1 billion for a billing system.

As another example, a Tier-1 European telco operator had 62 different billing systems.

Challenges:

Business agility,

time to market,

from network centric to customer centric,

Next generation networks, mobile broadband and cloud computing

Roles in new business models and eco-systems

Ericsson Global Services division grew from SEK 29 billion and 8000 people in 2003 to SEK 97 billion and 60,000 people in 2012.

SIM free iphone japan finally arrive in Japan – directly sold by Apple.

SIM-lock free iPhone 5s and iPhone 5c are now officially sold via the Japanese section of the official Apple.com webstore.

It has been official policy recommendation (not regulation) by Japan’s General Affairs Ministry (総務省) for Japan’s mobile operators to sell SIM-free mobile phones, or to remove the SIM-lock of phones when requested by customers. However, Japan’s mobile operators have been very shy to follow the Ministry’s recommendation, and particularly Japan’s operators did not follow this recommendation for the iPhone.

Apple has now taken the step to offer SIM-free iPhones (model 5s and 5c) officially via the apple.com webstore in Japan.

This is a further step on the way of disruptive innovation sweeping through Japan’s mobile phone sector, which evolved from NTT monopoly and leased phones, via step-wise liberalization, entry of newcomers, and now domination by three groups NTT-DoCoMo, KDDI/AU and Softbank.

SIM-free iPhone sales in Japan- What will be the implications?

For customers, it will be much easier now to switch operators in Japan under the Mobile Number Portability (MNP) program keeping their iPhone. It will be seen, whether operators follow up with their number portability procedures to include the iPhone, which was not the case until recently.

For customers, roaming and international travel will be easier, customers will be able to use their Japan-bought SIM-free iPhone on foreign networks inserting local foreign operators’ SIM cards. Japanese operators might lose some limited amount of roaming income (which has never been very high, unlike in Europe).

For operators, churn under the Number Portability Program is likely to increase, increasing competitive pressure on operators to differentiate via radio connectivity, customer service, and innovative services.

How to get and use a SIM-free iPhone in Japan?

We have not yet done this ourselves, but what we hear is:

Buy a SIM-free iPhone from the Apple online Apple-store (apparently SIM-free iPhones are not available from operator stores or physical Apple stores). Take care, the models may differ depending on which operator you want to use the iPhone on, i.e. Docomo or KDDI/AU or Softbank. Better check with the operator about prices and conditions before you purchase the SIM-free iPhone, just to be sure.

Take the iPhone to a mobile operator store (i.e. Docomo, KDDI/AU or Softbank, depending on which type of iPhone you have bought), subscribe for service and get a SIM-card for the iPhone.

There are also some mobile virtual operators (MVOs) in Japan, i.e. operators which purchase capacity from Docomo, Softbank or KDDI, and then retail this capacity to end users. Check their conditions, service speed, bandwidth etc before you buy.

Supercell investment leverages paradigm shift, time shift and market disconnects

Smartphones and the “freemium” business models are bringing a dual paradigm shift to games and create a new truly global market. To take advantage of this global paradigm shift, its necessary to overcome the cultural disconnects between markets. SoftBank and GungHo‘s investment in the Finnish smartphone/tablet game maker Supercell, announced on Oct. 15, will help to overcome the disconnect between Japan’s and other game markets for both Supercell and GungHo.

One of SoftBank‘s aspects is it’s “time-shift” investment model, another is SoftBank‘s 30/300 year vision – both are important factors to understand the Supercell investment.

Comparing Supercell’s US$ 3 billion valuation with Japanese game companies (note that the market cap for the full SONY Group is shown here)

This Figure contrasts the market caps of new mobile and smartphone centric game companies (GungHo, Supercell, DeNA and GREE) with traditional console, video game and arcade game companies.

SoftBank announced that because of the majority investment, Supercell will become a subsidiary of SoftBank, and GungHo will account for Supercell’s profit/loss under the equity method.

Comparing Supercell’s US$ 3 billion valuation with Japanese game companies (note that the market cap for the full SONY Group is shown here) and SoftBank

GungHo and Supercell both are top-ranking mobile game companies: GungHo inside Japan with “Puzzle and Dragons”, and Supercell outside Japan with “Hay Day” and “Clash of Clans”. Expect both to leverage each other’s resources.

Both GungHo and Supercell show explosive growth:

GungHo’s operating profits increased 4050% (x 40) for Jan-June 2013 compared to the same period one year earlier.

Supercell’s revenues (mainly in-game purchases) jumped 500x from EURO 151,000 in 2011 to EURO 78 million in 2012.

Culture can be an issue between Japan and other countries, however, SoftBank has invested in more than 1000 comparable companies, and many of SoftBank’s investments have been outstandingly successful including Alibaba and Yahoo.

However, investment and management support by SoftBank does not automatically guarantee success in Japan – despite SoftBank’s investment and support, Zynga closed operations in Japan earlier this year. Success in Japan will remain Supercell’s responsibility, despite SoftBank’s and GungHo’s help and investment – as Zynga can tell.

SoftBank aims for global No. 1 position: Learn more about SoftBank, Masayoshi Son, and his 30/300 year vision for SoftBank

Report on “SoftBank today and 300 year vision” (approx 120 page, pdf file)

How do you see Yahoo KK’s latest move to reduce or eliminate merchant’s fees? Do you see this as an attack by SoftBank/Yahoo on Rakuten?

SoftBank and Rakuten are clearly two very different companies – they don’t compete on the same ground. SoftBank is a telecom company with a Government spectrum license – a quasi-monopoly on a certain wavelength spectrum. Rakuten has no such monopoly, but is an internet based ecommerce company.

How do you see the future of Rakuten now?

Rakuten is clearly squeezed between SoftBank/Yahoo on one side and Amazon.com on the other side.

Amazon.com’s Jeff Bezos, SoftBank/Yahoo-KK’s Masayoshi Son and Rakuten’s Hiroshi Mikitani are clearly some of the most brilliant minds on this planet earth, so any battle between these three is phenomenal.

You ask about Hiroshi Mikitani/Rakuten – he clearly has his job cut out to compete with Masayoshi Son and Jeff Bezos – that’s not easy at all.

In particular, Amazon.com has a lot of strengths in areas, where Rakuten does not compete, e.g. AWS – Amazon Web Services, which is a very important cloud services company.

In terms of globalization, I also see challenges ahead for Rakuten. Even though Rakuten has recently decided to train staff in English conversation, its not a trivial job for an essentially Japanese company to globalize.

How do you see globalization of Rakuten and Softbank?

SoftBank clearly has taken a big step in acquiring Sprint in USA. SoftBank’s very big challenge is now to make Sprint a very big success and this will take some time. Rakuten also has a huge challenge to globalize, and it will be interesting to see if Rakuten can become a global company

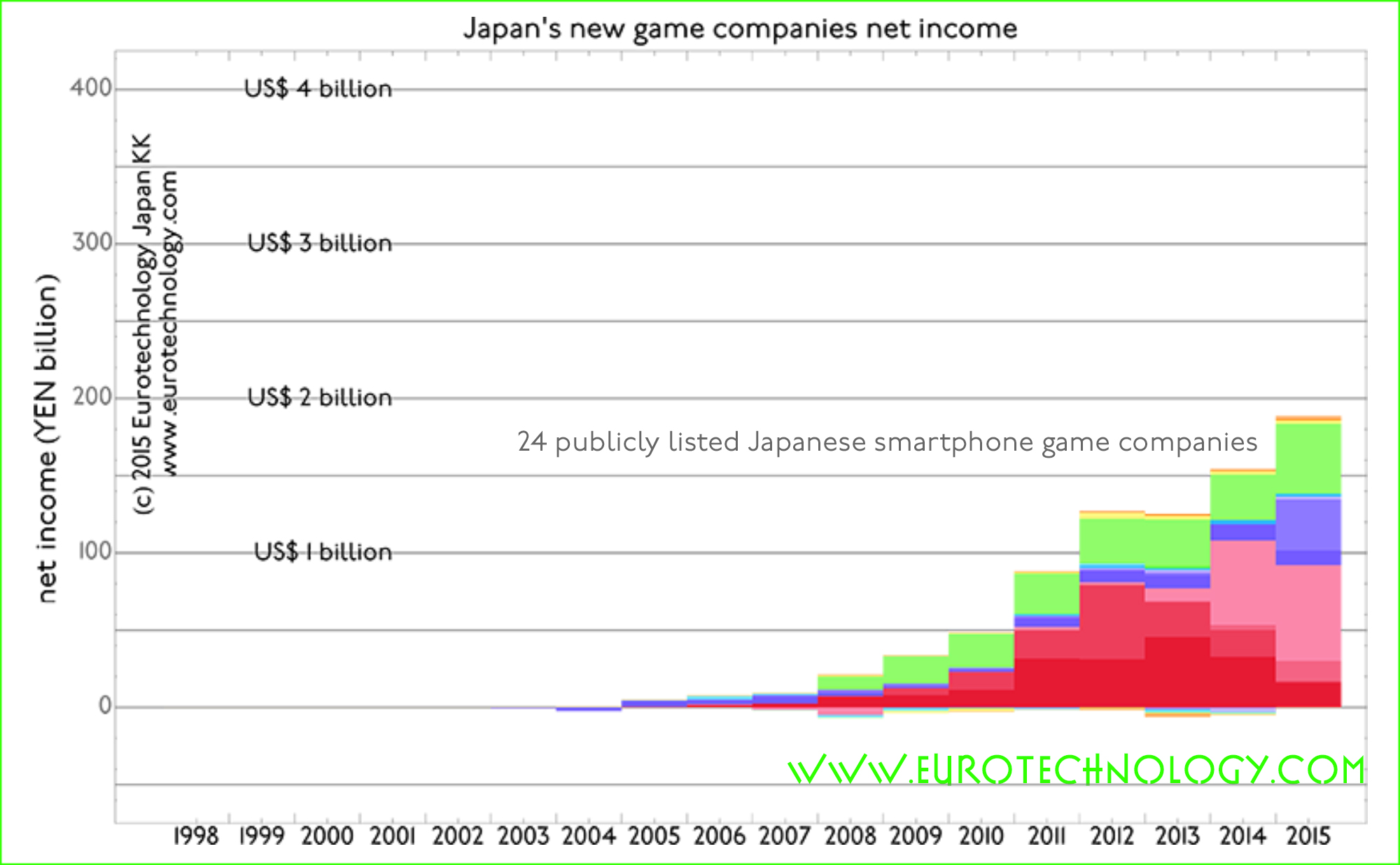

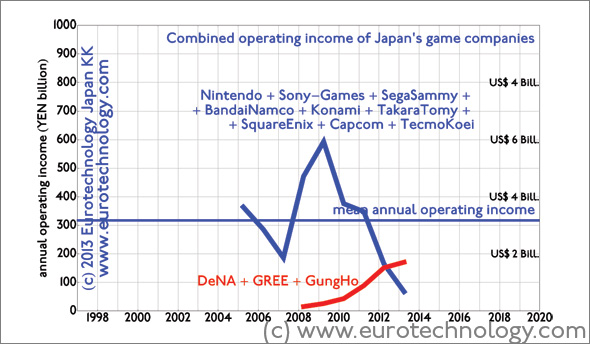

Since last financial year (ended March 31, 2013), three newcomers (GungHo, DeNA, and GREE) combined achieved higher operating income and higher net income than all 9 iconic Japanese game companies (Nintendo + SONY-Games + SegaSammy + BandaiNamco + Konami + TakaraTomy + SquareEnix + Capcom + TecmoKoei) combined.

While the newcomer’s revenues are increasing (except for GREE), the traditional 9 game companies’ revenues peaked in 2008, and have been falling rapidly ever since.

Clearly Japan’s the 2003-2005 mergers in Japan’s game sector did not make the sector “future proof” – more dramatic changes will be either initiated by the iconic incumbents, or imposed on them from newcomers such as GungHo.

Note that the position of foreign entrants remain weak in Japan’s game market overall.

Three new game companies (GungHo, DeNA, GREE) overtake Japan’s 9 iconic game companies in operating profits (note that the last data point for 2013 for GungHo is only for the first 6 months, i.e. full year results will show that the “new” game companies are doing even better compared to the “old” game companies than visible in this figure) Source: https://www.eurotechnology.com/store/jgames/Three newcomers (GungHo, DeNA, GREE) achieve higher net profits than all 9 Japanese game icons combined (note that the last data point for 2013 for GungHo is only for the first 6 months, i.e. full year results will show that the “new” game companies are doing even better compared to the “old” game companies than visible in this figure) source: https://www.eurotechnology.com/store/jgames/

Japan game market disruption: online and smartphone came company GungHo with Puzzle and Dragons

GungHo started as OnSale KK, a joint-venture between SoftBank and the US company OnSale Inc., the purpose of this JV was Japan market entry for this US company, an ecommerce company. OnSale KK pivoted from ecommerce to games and started to distribute the Korean game Ragnarok and others, and changed its name to GungHo. GungHo’s breakthrough came with “Puzzle and Dragons” – Jan-June 2013 operating profits increased 4050.1% (four thousand fifty percent) compared to the same period one year ago. GungHo is part of the SoftBank group. More in our report on “Japan’s game makers and markets”

Japan game market disruption: GREE

GREE on the other hand – although a successful new venture in Japan’s game sector – is not doing so well currently: reported revenues and income have both been falling. Essentially, GREE has difficulties to implement the plan to build a global business based on their Japanese methods and business models. The factors are both “hard” and “soft”, i.e. business models, and human factors. Details on GREE’s performance, and reasons for GREE’s current issues in our report:

Japan’s iconic game companies (Nintendo, Sony, Sega-Sammy, Bandai-Namco, Konami, Takara-Tomy, Square-Enix, Capcom, Tecmo-Koei) see brutal disruption by smart phone games

Japan game sector disruption: Three newcomers (GREE, DeNA and GungHo) achieve higher operating income than all top 9 incumbent game companies combined

Japan’s top 9 iconic game companies, Nintendo, Sony, Sega-Sammy, Bandai-Namco, Konami, Takara-Tomy, Square-Enix, Capcom, Tecmo-Koei created much of the world’s games markets, and many of the world’s most loved game characters.

They are now seeing brutal disruption.

Japan game sector disruption

With the Financial Year ending March 31, 2013, for the first time, just three Japanese newcomers (GREE, DeNA and GungHo) achieved higher operating income than all top 9 Japanese iconic incumbent game makers:

In FY2012 combined operating income of all 9 incumbent game companies was YEN 67.6 billion (US$ 700 million), combined operating income of the 3 newcomers was YEN 174 billion (US$ 1.8 billion) – even though for GungHo only the first 6 months of 2013 are included in the calculation.

Operating income of Japan’s top 9 games companies declined steadily since 2009 – combined operating income for FY2012 was YEN 67.6 billion (US$ 700 million)In 2013, three newcomers (GREE, DeNA, GungHo) achieved higher operating income than all nine established Japanese game makers. Combined operating income for FY2012 was YEN 174 billion (US$ 1.8 billion)

Because of its size, Nintendo has the greatest weight in the overall performance of Japan’s traditional game sector. Nintendo has been dramatically affected by the shift from traditional game consoles to smartphones. Still, Nintendo (as all other Japanese iconic game companies) has tremendous resources, tremendous creativity, globally loved characters and brands, and huge cash reserves. I don’t think that Nintendo (and other Japanese game companies) risk as much to follow Nokia and RIM/BlackBerry’s fate, but may be more resilient. However, there has been substantial consolidation in Japan’s games sector of recent years, and the current challenges could lead to more M&A in Japan’s games sector.

The disruptors

We have only picked three important new market entrants – there are many more in Japan’s vibrant mobile game venture scene.

DeNA

DeNA initially started as a mobile auction group, and sees continuous strong growth and high margins.

GREE

Of these three, GREE is currently suffering some set-backs originating from GREE’s business model. GREE started as a SNS and social game platform on Japan’s “galake” (Galapagos Keitai) relying on Japan’s mobile internet services i-Mode, EZweb and Yahoo-Mobile, where operators traditionally take 9% commissions. Initially GREE tried to transfer this “platform on platform” business model to other countries, but this does not seem to work out. So GREE is now pivoting to original games, and has seen setbacks.

GungHo

GungHo started as a joint-venture with a US company, the purpose of this JV was Japan market entry for this US company. GungHo then pivoted away from this joint-venture to become a games company, and produced a series of games, which all did well, but not extraordinarily well. That is, until GungHo created “Puzzle and Dragons”, which is growing spectacularly well: Jan-June 2013 operating profits increased 4050.1% (four thousand fifty percent) compared to the same period one year ago, and net profits increased 2507.8% (two thousand seven percent) compared to Jan-June one year ago.

The disruption

The shift to smartphones is hitting Japanese traditional iconic game makers from all sides:

the shift from TV to tablets and mobile phones

the shift from dedicated game consoles to smart phones and tablets

the shift from Japan’s “galake” feature phones to smart phones

the shift in business model from traditional US$ 40-60 game cassettes-type to free game downloads with in-game purchases and advertising

…and more

Japan’s game sector report

Learn more: read our report on Japan’s game makers and markets (approx. 400 pages, pdf file)

Masayoshi Son threatened to set himself on fire in Japan’s Post and Telecommunications Ministry? Is it really true?

by Gerhard Fasol

Masayoshi Son is known for his unbreakable will to achieve his and his companies’ business goals, and the will to take risks.

Masayoshi Son threatened to set himself on fire in the Ministry?!? Spectrum allocations for KDDI and SoftBank:

Currently Masayoshi Son, Founder of Softbank, is battling for a revision of a decision by Japan’s Ministry of General Affairs (Soumu-Sho) to award a new tranche of radio wave spectrum to KDDI’s subsidiary UQ, rather than sharing the spectrum equally with SoftBank‘s subsidiary Wireless City Planning.

Masayoshi Son threatened to set himself on fire in Japan’s Post and Telecommunications Ministry? Asking Masayoshi Son directly:

For a long time, I knew of a story about Masayoshi Son threatening to set himself on fire inside Japan’s Postal and Telecommunications Ministry (now merged into Japan’s Ministry of General Affairs (Soumu-Sho) since administrative reforms some years ago) in order to underline his request for a particular telecommunications license, or access to NTT exchanges, or similar matters Masayoshi Son was applying for at the time. I was long puzzled whether this story is true or not, so some years I go I had the chance to check this story out directly with Masayoshi Son, via the Chief- Editor of BusinessWeek, Mr David Rocks.