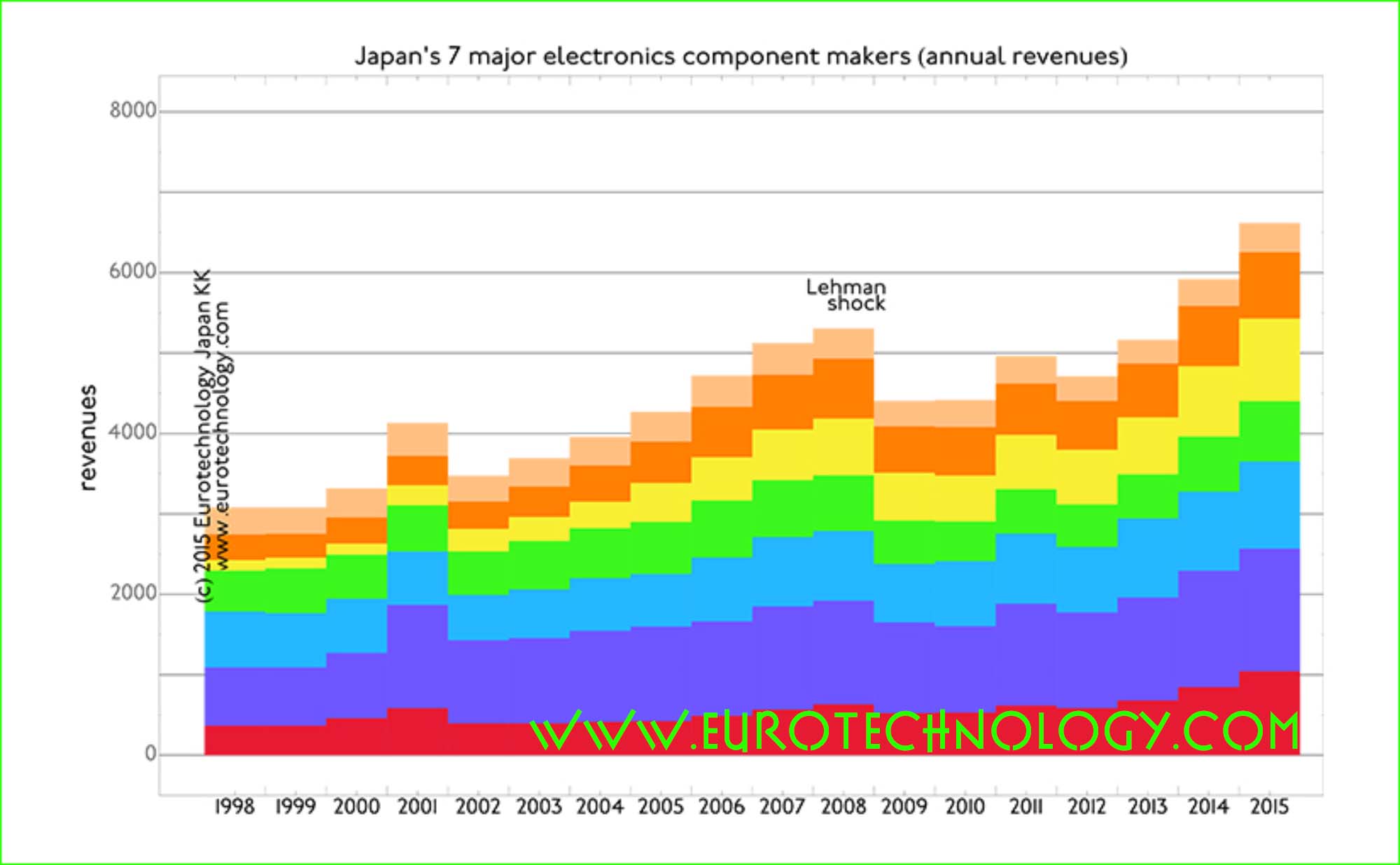

Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

The mobile internet was born 16 years ago in Japan

Galapagos-Syndrome: NTT Docomo failed to capture global value

On February 22, 1999, the mobile internet was born when Mari Matsunaga, Takeshi Natsuno and Keiichi Enoki launched Docomo’s i-Mode to a handful of people who had made the effort to the Press Conference introducing Docomo’s new i-Mode service. KDDI soon followed with EZweb, and J-Phone with Jsky (J-Phone was acquired by Vodafone, which was unable to manage J-Phone, Vodafone then sold the company to SoftBank).

i-Mode’s popularity soon exceeded any expectation: Docomo for some periods had to limit new subscriptions.

With Steve Jobs’ love for Japan, and Apple’s intense supplier relationships with Japan, its not farfetched to see connections between i-Mode and iPhone, in particular the i-Mode ecosystem and Java-based i-Appli’s are forerunners of today’s apps and apps-ecosystems.

At that time there was no Wikipedia, and Docomo had no English-language website at all, so our company Eurotechnology Japan KK’s information was more or less the only English language information openly available about i-Mode. We were bombarded by requests from many major semiconductor firms, telecom operators, investment banks, students and world-famous business schools for our i-Mode report and related business development and strategic work.

Today 5 of the global top-10 top-grossing Apps are Japanese

While Docomo never managed to capture global value from inventing and first introducing the mobile internet, the No. 1 top-grossing company globally, and five of the top-10 globally top-grossing Apps for iOS and Google-Play combined are Japanese (source: App-Annie).

Japan’s app market is the world’s largest in terms of cash revenues

Its also no coincidence that in terms of cash value, Japan’s is the world’s largest app-market for iOS and Google-Play combined, bigger than the US market and the Chinese market in terms of cash value. (source: App-Annie).

App-Annie’s data to our knowledge only cover the iOS and Google-Play app-stores, not the i-Mode and other mobile internet businesses, so Japan’s actual mobile app economy is even larger than App-Annie data show.

i-Mode is still alive and kicking – and a big business for Docomo

i-Mode is still today the mobile internet system for Docomo’s traditional flip-phones which are still an important part of the market, and recently made headlines since sales for traditional flip-phones were rising, while smartphone sales were (temporarly?) dropping.

i-Mode (and EZweb for KDDI, and Yahoo-mobile for SoftBank) will still be important business for some time to come in Japan.

Murata introduced their newest Cheerleader robots in a press event on September 25, 2014 in Tokyo. Purpose of the robots is brand building and advertising of the company’s components and capabilities.

Watch the Cheerleader robots dance synchronously here:

Murata Manufacturing (村田製作所)

While Japan’s eight electronics conglomerates stagnate in both revenues and income for the last 15 years, many of Japan’s electronic component manufacturers are thriving, as explained in detail in our report on Japan’s Electronics industries.

It is maybe not a coincidence, that many of the most successful electronics manufacturers are located in Kyoto, including Murata Manufacturing (村田製作所) – away from the politics of Tokyo.

Ceramic capacitors are at the core

At the core of the business are monolithic ceramic capacitors with a 35% market share globally. A single typical smartphone includes about 700 such ceramic capacitors, a laptop computer about 800, and a tablet computer or TV set about 600, and a car about 200.

Overcoming commoditization and maintaining pricing power by achieving overwhelming global market shares

For most manufactured electronic components, Murata is able to achieve overwhelming global market shares, e.g. 35% for monolithic ceramic capacitors, 70% for ceramic filters and resonators, 60% for radio connectivity modules and 95% for shock sensors.

Globalization

While company culture is strongly determined by Kyoto entrepreneurial traditions, Murata has 14 companies in USA, 13 companies in Europe, 27 companies in Greater China, 17 companies in the rest of Asia, and 30 companies in Japan. For our detailed analysis and comparison with other Japanese electronics companies, read our report on Japan’s Electronics industries.

Cheerleader robots highlight components and communication modules and “3S” competence: Stabilization, Sensing and Synchronization

Cheerleaders robots are a group of robots, bodies are balancing on rolling balls, and their bodies are equipped with motors to drive the balls, position and balance sensors and communication modules to synchronize the robots’ motion.

Murata “3S”: Stabilization, Sensing and Synchronization

Murata cheerleader robots dance in syncYuichi Kojima, Senior Vice-President and Deputy Director of Technology and Business Development Unit, and Koichi Yoshikawa, Senior Manager, Corporate Communications present the robotsMurata Boy (ムラタセイサク君 = Muratseisaku-kun), the Murata Cheerleaders, and Murata Girl (ムラタセイコちゃん= Murataseiko-chan) (left to right)Yuichi Kojima (Senior Vice-President and Deputy Director of Technology and Business Development Unit) and Koichi Yoshikawa (Senior Manager, Corporate Communications) present Murata Boy (ムラタセイサク君 = Murataseisaku-kun), the Murata Cheerleaders, and Murata Girl (ムラタセイコちゃん= Murataseiko-chan) (left to right)

The bigger picture: Murata’s robots, the big wide world, and open innovation

As presented by Murata today, the cheerleader robots, Murata Boy and Murata Girl, are closed stand-alone systems, essentially for advertising and branding the company’s products.

SoftBank, on the other hand, is working to create a developer community around its Pepper robot, and SoftBank’s SPRINT subsidiary is planning to sell Pepper in the USA from 2015. Pepper has been developed for SoftBank by the company Aldebaran, founded by Bruno Maisonnier.

Google has acquired a range of robot companies, and is developing self driving cars.

LEGO switched from a closed “waterfall” model for developing the LEGO Mindstorms system to an open innovation model with huge success.

There is a huge contrast between these robotics programs which are community based, aim to create developer communities, develop API’s (application develop interfaces) and in some cases use open source software – and on the other hand the Murata robotics program, which seems to be a closed program creating one-off closed robot systems.

I believe that Murata’s robots could create much more global impact, if they would move from a corporate branding exercise to a platform for developer communities. In my view, Murata’s Cheerleaders – if they could talk – might shout out for being opened up. Imagine the creativity which could emerge from school classes or students programming the Cheerleaders via their APIs or SDKs.

VCSEL inventor Kenichi Iga: hv vs kT – Optoelectronics and Energy

(Former President and Emeritus Professor of Tokyo Institute of Technology. Inventor of VCSEL (vertical cavity surface emitting lasers), widely used in photonics systems)

VCSEL: how Kenichi Iga invented Vertical Cavity Surface Emitting Lasers

My invention of vertical cavity surface emitting lasers (VCSEL) dates back to March 22, 1977. Today VCSEL devices are used in many applications all over the world. I was awarded the 2013 Franklin Institute Award, the Bower Award and Prize for Achievement in Science, “for the conception and development of the vertical cavity surface emitting laser and its multiple applications in optoelectronics“. Benjamin Franklin’s work is linked to mine: Benjamin Franklin in 1752 discovered that thunder originates from electricity – he linked electronics (electricity) with photons (light). After 1960 the era of lasers began, we learnt how to combine and control electrons and photons, and the era of optoelectronics.

If you read Japanese, you may be interested to read an interview with Genichi Hatakoshi and myself, intitled “The treasure micro box of optoelectronics” which was recently published in the Japanese journal OplusE Magazine by Adcom-Media.

Electrons and photons

Who are electrons? Electrons are just like a cloud expressed by Schroedinger’s equation, which Schroedinger postulated in 1926. Electrons can also be seen as randomly moving particles, described by the particle version of Schroedinger’s equation (1931).

Where does light come from? Light is generated by the accelerated motion of charged particles.

Electrons also show interference patterns. For example, if we combine the 1s and 2p orbitals around a nucleus, we observe interference.

In a semiconductor, electrons are characterized by a band structure, filled valence bands and largely empty conduction bands. The population of hole states in the valence bands and of electrons in the conduction bands are determined by the Fermi-Dirac distribution. In typical III-V semiconductors, generation and absorption of light is by transitions between 4s anti-bonding orbitals (the bottom of the conduction band) and 4p bonding orbitals (the top of the valence band).

In Japan, we are good at inventing new types of vertical structures:

in 607, the Horyuji 5-Jyu-no Toh (5 story tower) was built in Nara, and today we have progressed to building the 634 meter high Tokyo Sky Tree Tower.

in 1893, Kubota Co. Ltd. developed the vertical molding of water pipes

in 1977 Shunichi Iwawaki invented vertical magnetic memory

in 1977 Tatsuo Izawa developed VAD (vapor-phase axial deposition) of silica fibers

in 1977 Kenichi Iga invented vertical cavity surface emitting lasers (VCSEL)

Communications and optical signal transmission

History of communications spans from 10,000 years BC with the invention of language, and 3000 BC with the invention of written characters and papyrus, to the invention of the internet in 1957, the realization of the laser in 1960, the realization of optical fiber communications in 1984, and now since 2008 we see Web 2.x and Cloud.

Optical telegraphy goes back to 200 BC, when optical beacons were used in China: digital signals using multi-color smoke. Around 600 AD we had optical beacons in China, Korea and Japan, and in 1200 BC also in Mongolia and India.

In the 18th and 19th century, optical semaphores were used in France.

In the 20th century, optical beam transmission using optical rods and optical fiber transmissions were developed, which combined with the development of lasers created today’s laser communications. Yasuharu Suematsu and his student showed the world’s first demonstration of optical fiber communications demonstration on May 26, 1963 at the Tokyo Institute of Technology, using a He-Ne laser, an electro-optic crystal for modulation of the laser light by the electrical signal from a microphone, and optical bundle fiber, and a photo-tube at the other end of the optical fiber bundle to revert the optical signals back into electrical signals and finally to drive a loud speaker. For his pioneering work, Yasuharu Suematsu was awarded the International Japan Prize in 2014.

VCSEL: I recorded my initial idea for the surface emitting laser on March 22, 1977 in my lab book.

Vertical Cavity Surface Emitting Lasers (VCSEL) have many advantages:

ultra-low power consumption: small volume

pure spectrum operation: short cavity

continuous spectrum tuning: single resonance

high speed modulation: wide response range

easy coupling to optical fibers: circular mode

monolithic fabrication like LSI

wafer level probe testing

2-dimensional array

vertical stack integration with micro-machine

physically small

VCSEL have found applications in many fields, including: data communications, sensing, printing, interconnects, displays.

As an example, the Tsubame-2 supercomputer, which in November 2011 was 5th of top-500 supercomputers, and on June 2, 2011 was greenest computer of Green500, uses 3500 optical fiber interconnects with a length of 100km. In 2012: Too500/Green500/Graph500

IBM Sequoia uses 330,000 VCSELs.

Fuji Xerox introduced the first demonstration of 2 dimensional 4×8 VCSEL printer array for high speed and ultra-fine resolution laser printing: 14 pages/minute and 2400 dots/inch.

VCSEL photonics started from minor reputation and generated big innovation. VCSELs feature:

low power consumption: good for green ICE

high speed modulation beyond 20 GBits/second

2D array

good productivity due to monolithic process

Future: will generate ideas never thought before.

em. President of Tokyo Institute of Technology, Professor Kenichi Iga, inventor of VCSELGerhard Fasol (left), em. President of Tokyo Institute of Technology, Professor Kenichi Iga (right)

In this newsletter David Uze, President for Japan & Korea of the global semiconductor electronics company Freescale, shares his success story in Japan, and his perspectives on Japan’s electronics industry sector….

Perspectives on Japan’s electronics sector by Freescale’s President for Japan & Korea, David Uze

Question (Gerhard Fasol): I have read several of your articles and interviews, and see that you express much optimism about Japan’s semiconductor industry. On the other hand, the retired Elpida-CEO Yukio Sakamoto said in an interview on Sept 5 in Nikkei, that the sale of Elpida to Micron was the best option for Elpida, while Renesas is also in a period of reconstruction.

How do you see Japan’s semiconductor sector, and where do you see its future?

Answer (David Uze): Japan’s semiconductor players have incredible IP portfolios. To not leverage such assets would clearly be missed opportunity for the Japanese economy.

Despite the pain and complexity of consolidation and restructuring, such actions usually force evolution. This leads to better product portfolios and the operational scale necessary to make the critical investments that fuel innovation. In the words of Friedrich Nietzsche, “What doesn’t kill you makes you stronger.” Similarly, in Japanese, “雨降って、地が固まる.” (in English: Rain makes the ground stronger).

Clearly, Japan will continue to be a chip design leader. Whether Japan returns to a prominent position in semiconductor manufacturing, relies largely on the priorities of the Japanese government and “Japan Inc.”

Question (Gerhard Fasol): At least until “Abenomics” and now the Olympic fever, a lot of companies globally are quite pessimistic about Japan’s growth. How do you see growth for your company in Japan? What do you feel about the future economic growth in the Japanese electronics sector?

Answer (David Uze): Freescale is working very hard to meet and exceed our Japanese customer’s expectation. Our belief and commitment to Japan is best embodied by the Japanese concept of being a “死に物狂い” partner to our customers (translation: a partner who never gives up, fights until death if necessary). Not a vendor. Our customers repeatedly tell me they want less “vendors” and more “true partners”. We are seeing business benefit from taking this path.

Japanese ingenuity and a technology savvy customer base has been and will continue to drive product innovation and ensure that Japan will remain a prominent player in the global marketplace.

Question (Gerhard Fasol): In my opinion, Japan has some incredible creativity – for example mobile internet which today is a major global growth industry, essentially was invented in Japan in 1999 by DoCoMo, KDDI and J-Phone, and Shuji Nakamura invented almost single handedly the GaN LED revolution which is revolutionizing the global lighting industry. How much R&D does Freescale do in Japan?

Answer (David Uze): In Japan, we have partnered with global technology leaders like Fuji Electric, Alps Electric and most recently Rohm Semiconductor. We continue to develop new technologies and solutions with these great companies and will expand our R&D partnerships in Japan.

Freescale is partnering with Tokyo University, software/hardware ecosystem partners and our customers in the automotive industry to develop solutions for next generation collision avoidance and other active safety applications.

Question (Gerhard Fasol): Tell us a bit more about your company Freescale if you like. What are your most exciting products now? Where would you like to drive your company in the future?

Answer (David Uze): Automotive makers/system suppliers and end-users are keenly interested in ADAS (advanced driver assistance systems), especially radar- and vision-based safety solutions. Freescale provides radar and logic chips for the most advanced safety solutions in the market. If your car has collision warning or parking assist features, they are likely based on Freescale technology.

Freescale has an intensely competitive culture. We won’t stop innovating and working to satisfy our customers until we are #1 in all market segments in which we participate. Of course, we won’t stop there.

Question (Gerhard Fasol): How big is your company in Japan now?

Answer (David Uze): Geographically, Freescale has offices in Tokyo, Nagoya and Sendai. Furthermore, we have extensive nationwide coverage via our excellent team of distribution partners including Avnet Internix, Marubun Corporation, Tokyo Electron Device and Toyota Tsusho Electronics as well as Chip-One-Stop as an e-tailer.

From a business scale perspective, Japan is one of Freescale’s largest and fastest growing markets. We have strong positions in Automotive and Digital Networking and are quickly expanding our footprint in Industrial and Consumer Electronics.

Question (Gerhard Fasol): Several times a week technology, software, energy, semiconductor companies approach my company with plans to enter Japan’s market, or to grow faster in Japan. What would be your most important advice to foreign technology companies thinking of entering Japan’s high-tech markets, or seeking to accelerate growth in Japan?

Answer (David Uze): Be sincere. Honor your commitments. Work hard.

Invitation to the races: The Asia Le Mans @ Fuji Speedway – international car racing event on September 20-22, 2013 free admission for all pre-registered Freescale guests

Question (Gerhard Fasol): You are holding a very interesting event at the Fuji Speedway on September 20-22. I know that you and Freescale are heavily engaged in R&D car racing. This sounds like a lot of fun, but there must be a very serious side also. Can you tell us why Freescale invests in car races, and what Freescale and Freescale customer get out of the car races?

Answer (David Uze): We are involved in Japan’s SuperGT racing series primarily to drive innovative R&D outcomes in automotive safety. Our focus is on contributing to a “Zero Fatality” vehicular future. Racing provides the most challenging environment for automotive systems due to the speed, vibration, g-forces and other environmental factors. Many revolutionary technologies have been borne from auto racing including; industrial utilization of the carbon fiber material, anti-lock brake systems, traction control, active suspension, seat belts and many other safety advancements.

Racing also provides a rallying point for our employees, partners and customers to work together as One Great Team (OGT!). We host 100’s of customers and partners during each race weekend where we have the opportunity to share ideas while fostering camaraderie. Off the track, our guests compete fiercely with one another. While at the track, they collaborate. This truly makes our Freescale OGT! Racing Program unique in both the racing industry and semiconductors.

Question (Gerhard Fasol): I heard you would like to invite our subscribers and readers to your Fuji Speedway event on Sept 20-22. Can you tell us a bit about what participants can expect, and how they can register?

Answer (David Uze): We’ll be offering very unique experiences to a broad range of people including current and future customers/partners, race fans, their families and even students. It is a combination of

David Uze invites our readers and subscribers to join the team for an exciting weekend of car racing at the legendary Fuji Speedway on September 20-22, 2013. You can have fun watching the races, attend a dance party hosted by musician & DJ Suzuki Ami and enjoy many fun family activities. This is also an opportunity to learn hands-on about the future of automotive technology and car electronics.

Details about the event and registration here: http://www.freescale.com/TheFreescaleExperience (日本語) http://www.freescale.com/webapp/sps/site/overview.jsp?code=DWF_TFE (English)

NEC is one of NTT’s traditional four equipment suppliers

NEC is one of NTT’s traditional suppliers of telecom equipment, and one of Japan’s flagship electronics companies. In the early days of the PC age, NEC dominated Japan’s PC market with the 98 series of PC, which had a NEC-proprietary variation of MicroSoft’s MS-DOS operating system.

NEC was the first ever Japanese joint-venture company with foreign capital: NEC started as a joint-venture with Western Electric Company

Interestingly NEC originally started as a joint-venture with Western Electric Company of the United States – NEC was the first Japanese joint-venture company with foreign capital.

NEC revenues and income overview

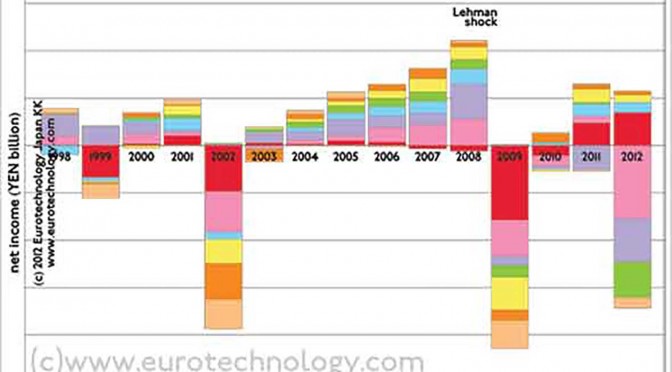

Here is an overview of NEC’s financial performance over the last 15 years, the period FY1998 – FY2012 – NEC’s business shrunk from YEN 5000 billion in FY1998 to YEN 3000 billion in FY2012, while on average reporting annual net losses of YEN 39 billion (US$ 390 million)/year over these 15 years.

During the 15 years FY1998-FY2012, NEC revenues declined from YEN 5000 Billion to YEN 3000 Billion, while reporting on average annual net losses of YEN 39 Billion/year. Source: our research report on Japan’s electronic industries. Purchase and download here: https://www.eurotechnology.com/store/j_electric/

Kazuo Inamori (80 years old, born January 30, 1932), Japanese serial entrepreneur, founded Kyocera Corporation on April 1, 1959, founded DDI (now KDDI) in 1984, and turned around Japan Airlines (JAL) during the last two years.

Japan Airlines (JAL) went bankrupt on January 19, 2010, Kazuo Inamori turned around JAL, and JAL went public again on Tokyo Stock Exchange on September 19, 2012, returning substantial profit for the Enterprise Turnaround Initiative Corporation of Japan Fund.

Legendary serial entrepreneur Kazuo Inamori (稲盛 和夫)

Kazuo Inamori used his “Amoba Management” (アメーバ経営) techniques to rebuild Japan Airlines from bankruptcy

Kazuo Inamori is famous for “Amoeba Management (アメーバ経営)”, essentially Amoeba management means divisional accounting, and has been refined for the management of Kyocera and many other companies.

Today Kyocera is divided into about 3000 “amoebas” – applying the amoeba management methods to Japan Airlines

Applying “Amoeba management” to JAL, Kazuo Inamori installed a real time system, to determine the profit of each route and each single flight in real time, while in the past profits (or losses) at Japan Airlines, were calculated months after the fact.

Kazuo Inamori on leadership: “the leader must have a vision and burning determination to carry out the vision whatever the obstacles”, and must communicate aims and targets to everyone in the company.

On nuclear energy:

Japan’s energy / electricity sector is in upheaval, and given Japan’s respect for seniority, given Kazuo Inamori’s standing in Japan, understanding Kazuo Inamori’s opinion is very important for understanding how Japan’s energy landscape is likely to evolve in the future.

“In the past the problems of nuclear energy were hidden from the public, and in the future must be disclosed”.

“It is not possible to maintain the current sophisticated society without nuclear power”. He thinks that nuclear power is a necessary evil.

Over the last 15 years, their combined annual sales growth was zero, and their combined annual loss was YEN 50.6 billion/year (= US$ 0.6 billion/year).

Compelling evidence that new business models for Japan’s electronics sector present a huge opportunity – as explained in this BBC interview.

Sales growth of Japan’s “Big-8” electrical manufacturers vs top 7 electronics component makers

Contrasting Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC) with Japan’s 7 electronic parts makers (Murata, Kyocera, TDK, Alps, Nidec, Nitto, ROHM)

Over the last 14 years since FY1997, the combined growth in revenues (=sales) of Japan’s “Big-8” electronics groups was zero. The compound annual growth rate (CAGR) of Japan’s top 7 electronic parts makers combined was +3.1%.

Net income/losses of Japan’s “Big-8” electronics giants vs top-7 electronics components makers

Net income (profit) of Japan’s “Big-8” electronics groups vs top-7 electronics parts makers

Over the last 14 years since FY1997, Japan’s “Big-8” electronics groups combined showed average losses of YEN 50.6 billion/year (=US$ 0.6 billion/year), while Japan’s top 7 electronic parts makers combined earned YEN 196 billion/year (= US$ 2.4 billion/year).

Net income/losses of Japan’s top electrical groups

Net after tax income of Japan’s “Big-8” electronics groups

This figure shows net after tax income for Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC), for the years since FY1997. For 5 of these 14 years the industry sector reported combined losses, which in total exceeded the profits achieved in good years. As a result, averaged over all 14 years, the industry sector shows combined losses on the order of US$ 0.6 billion/year.

Creating new business models for this very large industry sector (of similar economic size as the Netherlands) is a huge opportunity.

et income/losses of Japan’s top-7 electronic component makers

Net income of Japan’s top 7 electronic parts makers

Japan’s top 7 electronic parts makers are in a much better financial situation than Japan’s electrical groups.

Over the last 14 years since FY1997, this industry sector only showed a net overall loss one single time – in the year following the Lehman shock, but showed combined net profits during all other years, resulting in average annual net profits on the order of US$ 2.4 billion/year.

BBC interview: “New business models for Japan’s electrical groups needed”

Taking advantage of low EURO exchange rates and the high YEN, and low valuations during the current economic crisis, Kyocera acquired 93.84% of TA Triumph-Adler AG for a total purchase price on the order of EURO 98.7 Million.

Triumph was founded 1896 as a bicycle maker, and has grown into a major European office equipment manufacturer and sales company. Triumph used to be famous for typewriters, with the disappearance of typewriters, Triumph went through a long sequence of restructuring and through many merger and acquisition transactions.

Kyocera acquired TA Triumph-Adler for its distribution network: TA Triumph-Adler has about 35,000 companies as customers in 33 countries, with 70% of sales in Germany, giving Kyocera a much larger distribution footprint in Germany and EU.

For an overview and analysis of Japan’s formidable electronics companies read our J-ELECTRIC report.

About 50 million mobile phones equipped with digital terrestrial mobile TV (“oneseg”) have been delivered up until today – not counting “oneseg” tuners for PCs, car navigation units and stand-alone units. Comparing this number with reports of mobile TV roll-out in other countries around the world, we conclude that 72.5% of todays mobile phones with mobile TV are in Japan.

How much mobile TV do Japanese people watch on their mobile phones? In the latest version of our mobile-TV report, we explain in detail our methods to determine that averaged over all of Japan’s population of 125 million (including those who don’t have a mobile-TV yet), the average viewing time is between 0.4 – 2.3 hours of mobile TV / month. WOW!

Mobile TV 2.0 (OneSeg-2) Not surprisingly, Japan’s media giants are now starting to move, and develop programming specially designed for mobile TV: for example “lunchbox” mobile TV broadcast to mobile phones from 12:00noon – 12:40pm weekdays with news, weather, diet information, summaries of TV shows… it’s only a question of weeks or months now in Japan for mobile TV to develop into a totally new advertising and m-commerce medium, and some has started already.

Starting the global mobile internet revolution with i-Mode in February 1999, we can see Japan’s leadership emerging in the mobile TV arena. Japan’s challenge is to leverage this know-how globally, Japan missed this chance with i-Mode and left the field to iPhone and friends!

In December 2008 97.5% of global mobile TV was in Japan and S-Korea

72.5% of all mobile phones with digital TV globally are in Japan: In the same way as with mobile internet (i-mode), Japan is again the global forerunner in mobile TV, together with South Korea.

(2) for mobile operators DoCoMo, KDDI and SoftBank margins are 10%-20% and increasing despite the crisis! Could mobile phone usage be crisis resistant?

(3) TV media groups had healthy margins in the 10%-20% range back around 2001- however these margins have been slowly melting away, and TV group margins are heading to cross the zero line into the red zone by 2010-2011. Watch out for a TV media crisis. Read more below.

Consumer electronics sector operating margins:

Nintendo bucks the trend: while Japan’s electronics firms’ margins are dropping into the red, and have never been much higher than 5% during the last 10 years, Nintendo‘s operating margins are above 30% and rising despite the crisis.

Margins of top Japan’s electronics multinationals and Nintendo

Mobile phone sector margins are 10% – 20% and rising despite the crisis.

Mobile phones seem to be resistant to the current crisis. DoCoMo‘s, KDDI‘s and Softbank‘s margins are healthy and improving despite the crisis.

Operating margins of Japan’s top 3 mobile operators

(Find full data, fully labeled graphics and analysis in our JCOMM Report)

Margins of TV media groups have been melting away since their peak in 2001.

Back in 2001 Japan’s TV media groups used to enjoy healthy margins of up to 20%. Over the last 8 years these healthy margins have molten away, and Japan’s large TV media groups are likely to all simultaneously go into the red from 2010 onwards, unless dramatic action is taken. Media groups will need to grow profitable new business, e.g. mobile-TV, and other cross-media growth areas.

Could it be that recent anti-takeover measures have made the large TV media groups complacent?

Operating margins of Japan’s TV media groups

(Find full data, fully labeled graphics and analysis in our J-MEDIA Report)

ICT trends for Japan: Ericsson and Nokia Siemens Networks (NSN) remain engaged in Japan’s ICT sector

by Gerhard Fasol

One of the Embassies here in Tokyo asked me to write a report about ICT trends for Japan…

ICT trends for Japan: Mobile phone sector

Pushed by the Government the mobile operators changed the business model for mobile phone sales from a straight subsidy model to an installment payment system. As a consequence the mobile phone sales collapsed, creating huge difficulties for Japan’s mobile phone makers, but greatly improving the financial results of mobile operators.

Smart phones grow market share in Japan

An interesting trend is the growth of the “smart-phone” market (Blackberry, HTC-Windows-Mobile phones, iPhone etc.) and mini-PCs, which can be acquired for YEN 1 with subsidy from eMobile.

In this context the Japanese telecom equipment makers association invited me to give a presentation, which was booked out 2-3 weeks ahead – about 100 Japanese telecom equipment maker managers attended! The General Affairs Vice-Minister / Secretary of State attended…

Nokia terminates mobile phone business in Japan

On November 27th, 2008, global press announcements announced that NOKIA will stop making mobile phones for Japan’s mobile operators with immediate effect. DoCoMo and SoftBank had NOKIA phones in preparation and had already started marketing efforts – these were cancelled a few days after NOKIA’s press announcement.

NOKIA had founded the Japan subsidiary on March 3rd, 1989, almost exactly 20 years ago, thus NOKIA has given up entering Japan’s mobile phone market after 20 years of efforts. NOKIA will not totally shut down in Japan, NOKIA announced that R&D and procurement will continue, and VERTU announced to enter Japan’s market with a mobile vertual network operator (MVNO) model renting network capacity from DoCoMo, and opening own shops.- However the opening of these direct VERTU stores keep being postponed.

NOKIA joins the row of European telecom companies which have given up operations in Japan: Vodafone, Cable & Wireless.

Nokia Siemens Networks (SNS) is continuing business in Japan as well, so NOKIA will not be entirely gone from Japan.

M&A

European company’s acquisitions in Japan are currently at low levels, including the ICT sector. By far the largest acquisition in Japan by a company from the European/Mediterranian area was not by an EU company, but by the Israeli company Iscar which acquired the Japanese company Tungaloy for around US$ 1 Billion. However, this acquisition was driven by US capital. Read details in our blog here.

In the opposite direction, Japanese acquisitions in EU and elsewhere, there is a boom of acquisitions by Japanese companies abroad. For example, TDK acquired the German company EPCOS, Fujitsu acquired the outstanding 1/2 of Fujitsu-Siemens, NTT-Data acquired 72.9% of Cirquent which was a 98% subsidiary of BMW before. SONY acquired the outstanding 1/2 of the SONY-Bertelsmann Music Group from Bertelsmann.

The current trend is definitely a strengthening of Japanese acquisitions in Europe.

The most important issue however are not the acquisition transactions themselves, but the crucial issue will be whether these acquisitions create or destroy value. In many cases the difficulties to overcome “cross-cultural” issues are enormous. Many huge wrecks line the road: Vodafone-Japan, Cable-Wireless-Japan, NOKIA’s mobile phone business in Japan, or DoCoMo’s overseas acquisitions. There are also many success stories – the most impressive and famous one Nissan-Renault, however there are many more. An interesting case in progress is Nippon-Sheet-Glass (now NSG Group)’s acquisition of Pilkington Glass (read about a presentation by NSG’s CEO here in our blog).