This morning 7:30am I was interviewed on BBC TV Asia Business Report about an update of Toshiba’s ongoing crisis, which has been 20 years in the making.

Here some notes in preparation for my interview.

What is Toshiba’s situation now?

Toshiba’s market cap today is YEN 1024 billion = US$ 9.6 billion.

Toshiba is expected today to announce write-off provisions on the order of US$ 6 billion.

Toshiba owes about US$ 5 billion to main banks as follows:

Mizuho YEN 183.4 billion

SMBC YEN 176.8 billion

Sumitomo Mitsui Trust Holdings YEN 131.0 billion

BTMU YEN 111.2 billion

Total YEN 602.4 billion = US$ 5.3 billion

Toshiba is on notice for delisting by the Tokyo and Nagoya Stock Exchanges, and faces the risk of being delisted by March 15, 2017, i.e. in about 4 weeks from now.

Toshiba is trying to raise capital e.g. by seeking investment in the IC/flash memory division, however, Toshiba seeks to keep control, so Toshiba is trying to raise a minority share, or non-voting shares or similar, in order not to lose control.

How did Toshiba get into a situation to potentially need to write off US$ 6 billion?

Toshiba acquired 87% of the US nuclear equipment manufacturer Westinghouse.

While Westinghouse is a famous name, what Toshiba actually acquired seems to have gone through a period of restructuring.

In 2015 Toshiba acquired the construction company SHAW’s assets from the Chicago Bridge & Iron Company CB&I for US$ 229 million plus assumed liabilities. CB&I had acquired SHAW for US$ 3.3 billion in July 2012, and SHAW has on the order of US$ 2 billion annual sales.

Why did Toshiba acquire a company for US$229 million, which has US$ 2 billion annual sales, and which was in 2012 acquired for US$ 3.3 billion? Which factors reduced the value of this company from US$ 3.3 billion to US$ 229 million within the 3 years from 2012 to 2015?

Presumably because there are large liabilities arising from nuclear construction, which Toshiba now seems to have to assume.

What is likely to happen now with Toshiba? Is Toshiba too big to fail?

Difficult to say what will happen. Toshiba is a huge corporate group with about 200,000 employees and many factories in many countries, so clearly Toshiba is not going to disappear without trace.

The immediate risk is that Tokyo Stock Exchange carries out its warning, and delists Toshiba, which will further increase Toshiba’s ability to raise capital. In the case of a delisting, private equity, and/or government might invest and restructure, and Toshiba might be split up. For example, Toshiba’s nuclear Westinghouse division is totally separate from its very successful flash memory division, there is not much business logic in having both under one holding company.

Impact on UK

Toshiba acquired 60% of UK based NuGeneration with the view to build nuclear power stations in the UK. This project requires Toshiba to contribute to the funding of the nuclear project, for which Toshiba would probably need a financially healthy partner.

What is the big picture? How did Toshiba get into this crisis?

Toshiba’s crisis has been building up for 20 years, and is in my view a consequence of corporate governance issues over a long time.

Essentially, Toshiba should have been reformed 20 years ago from the top down.

Japan’s 8 electronics giants have had essentially no growth and no profits for 20 years. This tragedy has been obvious for many years now, and was a big contributing factor for Japan’s government to reform Japan’s corporate governance laws and regulations, see:

Toshiba’s Board of Directors was exchanged in September 2015, and now includes several very capable and experienced Japanese independent Board Directors, but unlike Hitachi, even today neither Toshiba’s Board of Directors, nor Toshiba’s Executive Board include one single foreigner.

One might think that a huge global group like Toshiba with complex businesses around the globe might benefit from a variety of view points and experiences from different countries at Supervisory Board and Executive Board level – not all just from one single country. Japanese corporations including Hitachi, SoftBank, Nissan and a small number of others are now recognizing the benefits of diversity of experience and viewpoints at Supervisory Board and Executive Board level.

We can only hope that Toshiba’s executives and Board Directors have the experience and ability to solve the extremely complex issues deep inside the bowels of the US nuclear construction industry – far away on the other side of the world.

On 18 July 2016 SoftBank announced to acquire ARM Holdings plc for £17 per share, corresponding to £24.0 billion (US$ 31.4 billion)

SoftBank acquires ARM: acquisition completed on 5 September 2016, following 10 years of “unreciprocated love” for ARM

On 18 July 2016 SoftBank announced a “Strategic Agreement”, that SoftBank plans to acquire ARM Holdings plc for £24.0 billion (US$ 31.4 billion, ¥ 3.3 trillion) paid as follows:

SoftBank’s start in telecoms via the acquisition of Tokyo Metallic, SoftBank’s acquisition of Vodafone Japan in combination with having developed YAHOO-Japan into the leading internet service company in Japan, were among the most important stepping stones for SoftBank to become a key global player in mobile communications.

Masayoshi Son: unreciprocated love for ARM for 10 years

In the Nikkei interview of 3 September 2016, Masayoshi Son explains that he had an “one-sided / unreciprocated love for ARM” for at least 10 years, but decided to acquire SPRINT first. After acquiring SPRINT he had to pay down debt before being able to acquire ARM now.

ARM was founded on 27 November 1990 as Advanced RISC Machines, however the abbreviation ARM was first used in 1983 and initially meant “Acorn RISC Machines”.

Acorn Computers Ltd was founded in 1978 in Cambridge (UK) by Hermann Hauser and Chris Curry to produce computers, and its most famous product was the BBC Micro Computer.

ARM has built an ecosystem of IC design systems and platforms which are at the core of low energy consumption ICs and CPUs for smartphones and many other electronic devices and cars. ARM may become or already is one of the core technology companies for the Internet of Things (IoT).

SoftBank’s ARM Business Department’s name changed to “New Business Department”

the future of Japan’s US$ 600 billion electronics sector, which dominated world electronics in the 1980s but failed to keep up with the evolution and growth of global electronics.

To survive Japan’s old established electronics conglomerates have two choices:

focus on a small number of key products (remember Apple CEO Tim Cook showing that all of Apple’s products fit on one small table)

actively managed portfolio model

however, for Japan’s economy to prosper, Japan needs many more young fresh new companies in addition to the old established conglomerates.

Interviews for BBC-TV and French Les Echos

Last week I was interviewed both live on BBC-TV and also by the French paper Les Echos about SHARP’s future:

In summary, I said that its not just about SHARP’s current predicament, but its about corporate governance reform in Japan, about reinventing Japan’s electronics sector, and that its more likely at this stage that Japan’s Innovation Network Corporation (INCJ) will take control SHARP, since INCJ is not just concerned with SHARP but with the bigger picture of restructuring Japan’s electronics sector.

INCJ has concepts for combining SHARP’s display division with Japan Display, and has plans for SHARP’s electronics components divisions, and for the white goods division, and other divisions.

SHARP governance: How and why did SHARP get into this very difficult situation?

Essentially SHARP assumed that the world market for TVs and PC displays will continue to demand larger and larger and more expensive display sizes, and thus took bank loans to build a very large liquid crystal display factory in Sakai-shi, south of Osaka.

In addition, SHARP, has a huge portfolio of many different products ranging from office copying machines and printers and scanners, mobile phones, high-tech toilets, liquid crystal displays, solar panels, and hundreds of other products. SHARP keeps adding new product ranges constantly expanding its portfolio of businesses, and rarely sells loss making divisions.

Effective and strong independent, outside Directors on the Board might have asked questions during the decision making leading to the building of the Sakai factory. They might have asked for a Plan B, in case the global display market takes a turn away from larger and larger and more expensive displays, or if the competition heats up and prices start decreasing, they might have asked about SHARP’s competitive strengths, they might have also questioned the wisdom to finance an expensive factory via short-term bank loans as opposed to issuing shares to spread the risks to investors.

Its not just outside Directors, shareholders could have also asked such questions.

SHARP has about YEN 678 billion (US$ 5.6 billion) debt, most is short-term debt, and in a few weeks, in March 2016, SHARP needs to repay about YEN 510 billion (US$ 4.2 billion), and needs to find this amount outside.

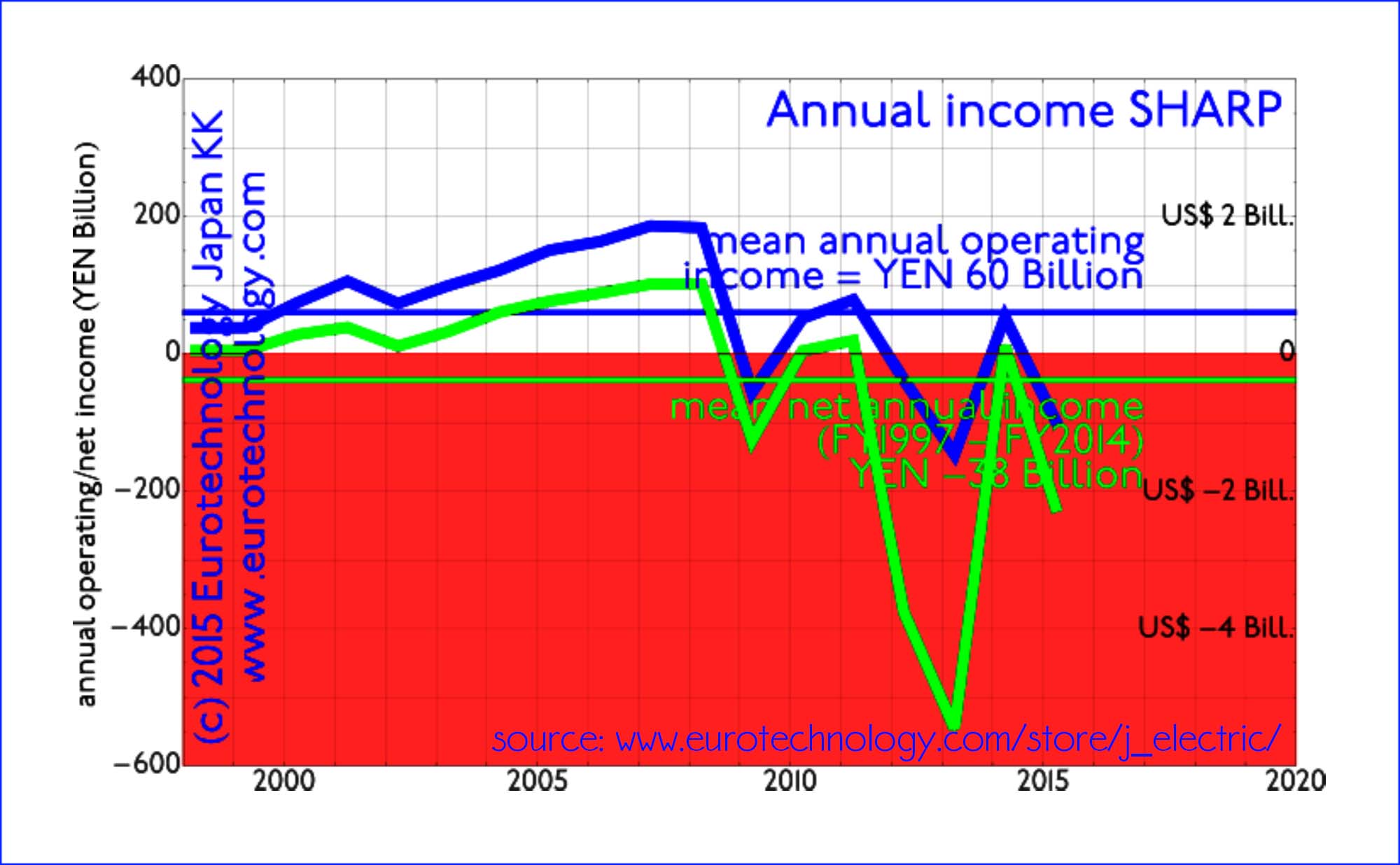

SHARP is a Japanese electronics company, founded in 1912 by Tokuji Hayakawa in Tokyo as a metal workshop making belt buckles “Tokubijo”, and today one of the major suppliers of liquid crystal displays for Apple’s iPhones, iPads and Macs.

SHARP today has about 44,000 employees, many factories across the globe, sales peaked around YEN 3000 billion (US$ 30 billion) in 2008, and show a steady downward trend since 2008.

Revenues (profits) peaked in 2008, and have fallen into the red since.

SHARP’s revenues (sales) peaked in 2008 around YEN 3000 billion (US$ 30 billion), and show a downward trend ever sinceAveraged over the last 14 years, SHARP shows average annual net losses of around YEN 38 billion per year (US$ 380 million per year)

What future for SHARP? Focus vs portfolio company

SHARP (or rather, its creditors, the two “main banks” Mizuho and Mitsubishi-Tokyo-Bank, and others controlling the fate of today’s SHARP) needs to decide whether it focuses on a group of core products, in which case it needs to be No. 1 or No. 2 globally for these products. Successful examples are Japan’s electronic component companies.

Or on the other hand, SHARP could be a portfolio company, in which case this portfolio must be actively managed.

What future for Japan’s US$ 600 billion electronics sector?

combined have sales of about US$ 600 Billion, similar to the economic size of The Netherlands, but combined for about 15 years have shown no growth and no profits. They are poster children for the urgent need for corporate governance reform in Japan.

These 8 electronics conglomerates are portfolio companies, and they need to manage these portfolios actively, such as General Electric (GE) or the German chemical industry are doing. Germany’s large chemical and pharmaceutical industries started active and drastic product portfolio management in the 1990s, and are continuing constant and active portfolio optimization via acquisitions, spin-outs, and other M&A actions, and so is GE.

Why “let zombie companies die” is beside the point

Concerning SHARP some media wrote headlines along the lines of “let zombie companies die”. Thats easy to write, however, SHARP is a group with 44,000 employees, many factories, about US$ 30 billion in sales annually.

“Let this zombie die” is not an option, SHARP has 100s of products, and divisions, and the best solution for each of these divisions is different. And that is exactly what the Innovation Network Corporation of Japan seems to be considering in its plans for SHARP.

I think the way forward is not “to let zombies die”, but to develop private equity in Japan

I think the move of Atsushi Saito, one of the key drivers of Japan’s corporate governance reforms, from CEO of Tokyo Stock Exchange/ Japan Exchange Group, to Chairman of the private equity group KKR is a tremendously important one in this context.

Will there be native Japanese private equity groups with sufficient know-how and ability to take responsibility of restructuring Japan’s electronics sector? Thats maybe the key question.

Why its not really about nationalism

Some media bring a nationalist angle into SHARP’s issues. However, Nissan was rescued by French Renault, UK’s Vodafone acquired Japan Telecom, and there are many other examples, where foreign companies acquire Japanese technology companies.

I don’t think nationalism is an issue here. The key issues is to create and implement valid business models for Japan’s huge existing electronics sector, and more importantly, create a basis for the growth valid new companies – not just reviving old ones.

Economic growth: Almost everyone agrees that economic growth is preferred over stagnation and decline. Fiscal policy and printing money unfortunately can’t deliver growth.

Governments best help economic growth by reducing friction, and by getting out of the way of entrepreneurs building, turning-round, and refocusing companies.

Some required action is counter to intuition: for example, in many cases reducing tax rates increases Government’s tax income, a fact known for many years. Effective education and research are key to create, understand and apply such non-obvious knowledge.

Companies need efficient leadership, leadership needs feedback, wise and diverse oversight by Boards of Directors, who ring alarm bells long before a company hits the rocks, or fades into irrelevance. Corporate governance reform may be the most important component of “Abenomics”. Read a Board Director’s view on Japan’s corporate governance reforms:

Japan’s electrical conglomerates are some of the poster children motivating Japan’s corporate governance reforms. In an interview about Toshiba’s future on BBC-TV a few days ago, I explained that Japan’s electrical conglomerates showed no growth and no profits for about 20 years, and the refocusing Toshiba has announced now should have been done much much earlier, 10-20 years ago (“Speed is like fresh food“). Refocusing Japan’s established corporate giants will release resources for start-ups, spin-outs and growth companies.

Japan can be very good at restructuring and turn-rounds, e.g. see

Over the last 18 years myself and our company have worked on many foreign-Japanese company partnerships, therefore we always have great interest in business partnerships involving Japanese companies, and have followed the Volkswagen-Suzuki relationship closely.

We published two blog articles after the ICC Arbitration Court issues judgement sealing the Suzuki-Volkswagen divorce, and before we became aware of the Volkswagen Diesel issues:

Interaction with Japan enforced total restructuring of leading US companies, including INTEL and MOTOROLA. According to my knowledge, there are almost no European companies yet which were forced to totally restructure their business due to interaction with Japan. I feel that this may happen in the future.

Volkswagen could be a candidate now, although US agencies and courts are now primary actors, Suzuki’s role may not be negligible.

Volkswagen had already lost out against Suzuki, and Suzuki’s CEO Mr Osamu Suzuki in the 1980s when India started to build an Indian automotive industry. India had considered to build India’s car industry based on Volkswagen’s Beatle, but decided to go with Mr Osamu Suzuki instead. Maruti Suzuki India Limited (マルチ・スズキ・インディア) achieved 45% market share in India’s passenger car market in 2014. Suzuki Motors owns 54% of Maruti Suzuki, and Mr Osamu Suzuki is greatly respected as Japan’s No. 1 top India expert.

When Mr Osamu Suzuki entered into the Maruti Suzuki India Joint-Venture, he reportedly insisted to have 100% decision making and management rights in the Joint-Venture.

Links between the Suzuki-Volkswagen and the Volkswagen Diesel issues time lines.

We can see interesting links in the time lines of the Suzuki-Volkswagen relationship and the Volkswagen Diesel issues:

Suzuki in 2005 decided to enter into a partnership with FIAT (not Volkswagen) on Diesel motors. This is 4 years earlier than the announcement of the Suzuki Volkswagen relationship on 9 December 2009.

Time line of events relevant to the Suzuki Volkswagen relationship

16 Nov 1970: “Maruti technical services private limited” (MTSPL) to create an Indian automobile industry, first CEO: Sanjay Gandhi. Sanjay Gandhi contacted Volkswagen AG to seek a cooperation to produce an Indian version of the VW Käfer (Beatle). However, a cooperation with Volkswagen did not work out. The company failed in 1977, and was reborn as Maruti Udyog Ltd by Dr V. Krishnamurthy.

1982: Maruti Udyog Ltd and Suzuki entered into a licensing and joint venture agreement, creating Maruti Suzuki India Limited (マルチ・スズキ・インディア), which in 2014 achieved a 45% market share of India’s passenger car market.

20 0ctober 2005: Suzuki and FIAT announce a partnership on FIAT’s Diesel engines (see: Suzuki announcement)

6 March 2006: Suzuki and GM announce the reduction of GM’s stake in Suzuki from 20% to 3%, strongly reducing the GM holding in Suzuki, which had started in August 1981. (see: Suzuki announcement)

9 Dec 2009: VW-CEO Martin Winterkorn and Suzuki-CEO Osamu Suzuki announced the “comprehensive partnership” at a press conference in Tokyo (see: joint Suzuki Volkswagen press announcement)

9 Dec 2009: Suzuki transferred 107,950,000 treasury shares to Volkswagen AG, valued approx at 226,695,000,000 yen (= approx. US$ 2.3 billion)

15 Jan 2010: VW purchased 19.89% of Suzuki shares for about € 1.7 billion

March 2011: Volkswagen writes in the annual report that Volkswagen “significantly influence financial and operating policy decisions” at Suzuki

Sept 2011: Suzuki’s Board decides to terminate the partnership

18 Nov 2011: Suzuki gives notice to Volkswagen of termination of partnership, Volkswagen does not reply (says Suzuki)

24 Nov 2011: Suzuki files for arbitration at International Court of Arbitration of the International Chamber of Commerce (ICC) in London

2013-2014: The International Council on Clean Transportation (ICCT) conducts a research project in collaboration with the West Virginia University to determine real world, away from test rigs, emissions from diesel cars in the USA. Project leader is John German. ICCT tests a VW Jetta, a VW Passat, and a BMW X5, and finds that in real world driving conditions, the VW Jetta exceeds the US-EPA Tier2-Bin5 Nix (Nitrogen Oxide) emission standards by 15 to 35 times, the VW Passat by 5 to 20 times, while the BMW X5 generally conformed to the standards except in extreme conditions. The fact that the BMW X5 conforms to the standard for the ICCT was proof that the technology to conform existed. (see: ICCT announcement)

30 Aug 2015: ICC Arbitration Court issues judgement and holds the termination of the partnership valid, orders VW to sell all Suzuki shares back to Suzuki (or a 3rd party selected by Suzuki), and orders Suzuki to pay damages for breaking the agreement

17 Sep 2015 8:45am: Suzuki purchases back 119,787,000 of its own shares previously owned by VW via Tokyo Stock Exchange ToSTNeT-3 system for 460,281,547,500 yen (approx. US$ 3.9 billion), completing the termination of the partnership and capital alliance with VW

26 Sep 2015: Suzuki announced the transaction to sell all 4,397,000 Volkswagen shares which Suzuki owns to Porsche Automobile Holding SE, completing the termination of the partnership and capital alliance with VW

The International Council on Clean Transportation (ICCT) study on real-world exhaust emissions from modern diesel cars

“In-Use Emissions Testing of Light-Duty Diesel Vehicles in the United States”

The ICCT contracted with the Center for Alternative Fuels, Engines and Emissions (CAFEE) at West Virginia University to test the real road emissions of three cars in the USA. This study is explained on the ICCT website “In-use emissions testing of light-duty diesel vehicles in the U.S.”

Mr Suzuki (Chairman of Suzuki Motors), wrote in his Japanese blog, that “ending the partnership with Volkswagen (Wagen-san as he calls VW) was like the relieve I feel after having a fishbone stuck in my throat removed”

No partnership works without meeting of minds, with opposite agendas and colliding expectations

by Gerhard Fasol, All Rights Reserved. 20 September 2015, updated 27 September 2015

VW Volkswagen Suzuki

Suzuki Volkswagen – bottom line first:

Volkswagen wanted Suzuki more than Suzuki needed Volkswagen

Volkswagen underestimated Suzuki’s strength and resolve, and didn’t do the required homework

Volkswagen overestimated its own leverage on the opposite side of the world from Wolfsburg

Partners with opposite agendas and colliding expectations, without communication and no homework can’t partner

Its not about “cultural differences”. Not at all.

On 9 December 2009 a beaming Martin Winterkorn (VW-CEO) was celebrating the new “comprehensive partnership” with Suzuki Motors, and Osamu Suzuki, the 79 year old CEO of Suzuki, was looking the other way, avoiding Mr Winterkorn’s eyes – as you can see in Reuters’ photograph of the occasion.

Reuters reported, that Mr Osamu Suzuki was asked how he would feel about a German CEO of Suzuki Motors in the future, and his answer was unambiguous: Mr Suzuki emphatically stated that Suzuki will not become a 12th brand for Volkswagen, and that he does not want anybody to tell him what to do.

Wall Street Journal reported, that Suzuki and Volkswagen would negotiate details in the weeks or months to come. We now know that these negotiations did not lead anywhere, and were never concluded satisfactorily.

It is obvious that there never was any “meeting of minds”, the expectations were colliding, and the CEOs had not a single language in common in which they could talk directly. At the press conference they looked away from each other.

Mr Suzuki (Chairman of Suzuki Motors), wrote in his Japanese blog, that “ending the partnership with Volkswagen (Wagen-san as he calls VW) was like the relieve I feel after having a fishbone stuck in my throat removed”

On 1 July 2011, Suzuki-CEO Osamu Suzuki informs the world about his frustrations about “Wagen” (ワーゲン), via a blog post “スズキとワーゲンの今とこれから (鈴木修氏の経営者ブログ)” (english translation: “Suzuki and Wagen now and the way forward”). Osamu Suzuki’s blog post can be read here (may need Nikkei subscription).

Professor Ferdinand Dudenhoeffer, Director of the Center for Automotive Research at the University Duisburg-Essen according to Bloomberg, summarized: “Mr Suzuki didn’t want to be a Volkswagen employee, and that’s understandable”.

Germany’s leading intellectual and business weekly Der Spiegel on 19 Sept 2011 quotes VW-CEO Martin Winterkorn about the VW-Suzuki relationship: “Da wackelt der Schwanz nicht mit dem Hund” (the tail is not going to wag the dog, which I guess has the meaning that Mr Winterkorn perceived Suzuki Motors as the junior partner who cannot have any independent power in a relationship with Volkswagen).

Suzuki Volkswagen alliance time line

9 Dec 2009: VW-CEO Martin Winterkorn and Suzuki-CEO Osamu Suzuki announced the “comprehensive partnership” at a press conference in Tokyo

9 Dec 2009: Suzuki transferred 107,950,000 treasury shares to Volkswagen AG, valued approx at 226,695,000,000 yen (= approx. US$ 2.3 billion)

15 Jan 2010: VW purchased 19.89% of Suzuki shares for about € 1.7 billion

Sept 2011: Suzuki’s Board decides to terminate the partnership

18 Nov 2011: Suzuki gives notice to Volkswagen of termination of partnership, Volkswagen does not reply (says Suzuki)

24 Nov 2011: Suzuki files for arbitration at International Court of Arbitration of the International Chamber of Commerce (ICC) in London

30 Aug 2015: ICC Arbitration Court issues judgement and holds the termination of the partnership valid, orders VW to sell all Suzuki shares back to Suzuki (or a 3rd party selected by Suzuki), and orders Suzuki to pay damages for breaking the agreement

17 Sep 2015 8:45am: Suzuki purchases back 119,787,000 of its own shares previously owned by VW via Tokyo Stock Exchange ToSTNeT-3 system for 460,281,547,500 yen (approx. US$ 3.9 billion), completing the termination of the partnership and capital alliance with VW

26 Sep 2015: Suzuki announced the transaction to sell all 4,397,000 Volkswagen shares which Suzuki owns to Porsche Automobile Holding SE, completing the termination of the partnership and capital alliance with VW

“Comprehensive partnership” without meeting of minds does not work

Partnerships are hard when CEOs on both sides don’t have any language in common, thus can’t talk to each other – and have exactly opposite expectations from the start and don’t address them until its too late

Processes and methods successful in Europe or USA often don’t work in Japan

Its not about “cultural differences”. Not at all.

Its about trust, respect, communication and “meeting of minds”, shared (not opposite) expectations and agendas.

VW made approx. US$ 1.3 billion profit on the Suzuki shares it owned from 2009-2015

Suzuki broke even approximately on selling own treasury stock to VW and repurchasing the same shares back from VW a few days ago, and on temporarily owning 2.5% of VW, but still may have to pay compensation to VW.

During the period 2009-2015 both VW and also Suzuki share prices increased substantially. The reason that VW made substantial financial profits from the VW-Suzuki share transactions, while Suzuki did not, is that Suzuki used 1/2 of the proceeds of selling Suzuki treasury stock to VW for R&D, thus had a much smaller holding of VW shares than VW did of Suzuki shares.

With cash reserves of approx. US$ 8 billion Suzuki will be just fine, and can now focus on expanding Maruti-Suzuki’s 37% market share of India’s passenger car market and other exciting growth projects.

And Volkswagen can now focus on growth markets, and Toyota – and other very pressing issues.

many of the underlying issues also apply in all other business areas, such as electronics, and technology.

Sanyo Shokai pivots from Burberry to Mackintosh and other brands

Burberry Japan pivots to direct business to solve Burberry’s “Japan Problem”: for the last approx. 50 years Burberry’s business in Japan was not Burberry’s business at all, but run under license by the Japanese company Sanyo Shokai and the giant trading company Mitsui. Sanyo Shokai’s core business was developing its own product lines Blue Label and Black Label and selling them under the Burberry Blue Label and Burberry Black Label brands.

Almost every day a foreign company approaches us to help them find a “Japanese partner” to build their business in Japan…

There are many examples of very successful Japan-market-entries via partnerships. Success stories include: Oracle, Salesforce.com, Starbucks, Fuji-Xerox, Yahoo, SuperCell, and many more, and until a few months ago, Burberry.

Burberry found an excellent Japanese partner in 1965, Sanyo Shokai, backed by giant trading company Mitsui, and Sanyo Shokai built a terrific business for Burberry in Japan! Not only did Sanyo Shokai import Burberry products to Japan, but Sanyo Shokai also developed two enormously successful sub-brands for Burberry in Japan: Burberry Blue Label and Burberry Black Label. And Sanyo Shokai kept transferring substantial royalties/license fees to Burberry’s headquarters.

Actually it turned out that almost all the business value for Burberry in Japan was in the Burberry Blue Label and Burberry Black Label sub-brands, which were developed by Sanyo Shokai in Japan, by Japan and for Japan – and with the required Japanese quality and customer service. Sanyo Shokai also contributed the Japanese Burberry flagship store in one of the world’s prime luxury shopping areas, Ginza, and about 300-500 Burberry stores all over Japan – many in prime locations.

In June 2015, Burberry terminated this very successful licensing relationship.

Now after their divorce, both Burberry and Sanyo Shokai rebuild their businesses in Japan from scratch:

Burberry lost 300-500 stores in Japan belonging to Sanyo Shokai including the Ginza flagship store

Burberry lost 300-500 stores which belong to Sanyo Shokai, and Sanyo Shokai’s flagship store in Ginza, and essentially has to build a Burberry business in Japan from zero, while former partner Sanyo Shokai is busy moving former Burberry customers over to Mackintosh and other Sanyo Shokai brands, with Mackintosh in almost the same segment Burberry is now entering afresh

Sanyo Shokai now pivots 300-500 stores from the Burberry brand to Mackintosh and other brands

Sanyo Shokai licensed the Mackintosh brand from Osaka based Yagi Tsusho, and is now pivoting 300-500 stores in Japan from the Burberry brand to the Mackintosh brand, and other Sanyo brands

Some puzzles about the Burberry – Sanyo Shokai split

why has Burberry not decided on a less disruptive transition?

For example, acquiring Sanyo Shokai comes to my mind. Acquisitions in Japan are not unheard of, and since Sanyo Shokai is a publicly traded company, well established rules apply.

why did Sanyo Shokai over the 50 years since starting the relationship with Burberry not build its 100% owned brand?

Much smaller Yagi Tsusho managed to acquire Mackintosh, why did not Sanyo Shokai within the last 50 years acquire or develop a 100% owned and successful brand? With Blue Label and Black Label, Sanyo Shokai has proven its ability to build and develop brands, why not under their own brand?

Has this transition been well thought through?

It will be interesting to see where both Burberry and Sanyo Shokai will stand 10 years from now – 10 years from this divorce. Both certainly are in challenging situations in Japan now after this divorce. Will both survive in Japan? Or only one of the two?

Foreign companies seeking to build a business in Japan via a partnership, and Japanese companies seeking to build the business of foreign companies in Japan can certainly learn from this case study. Although its fashion and apparel, many of the underlying issues also apply in all other business areas, such as electronics, and technology.

Burberry’s new directly operated flagship store in Tokyo OmotesandoSanyo Shokai’s flagship building in Tokyo-Ginzs, one of the world’s prime luxury shopping areas, much frequented by cash-rich Chinese shoppers. Currently being converted from the Burberry brand to Mackintosh and other Sanyo Shokai brands (second building from the left)

Dentsu dominates Japan’s media sector and advertising

Dentsu switches from JGAAP to IFRS accounting standards with big impact on KPIs

Dentsu dominates Japan’s advertising and media industries, and attracts some of the most creative Japanese talent, although Dentsu is not the first advertising agency in Japan – that priority belongs to Hakuhodo.

From April 1, 2015, Dentsu decided to switch to IFRS accounting standards from Japan’s JGAAP standards. For FY2014, Dentsu reports financial results both using IFRS and JGAAP standards, giving us the fascinating opportunity to compare both accounting standards for a major corporation.

So how big is Dentsu? For FY 2014 (April 1, 2014 – March 31, 2015) Dentsu reports (we have rounded the figures):

Net Sales (JGAAP) = ¥ 2419 billion (=US$ 19 billion)

Revenues (IFRS) = ¥ 729 billion (=US$ 6 billion)

For operating income, net income and other data IFRS and JGAAP measure quite different KPIs.

Disruption is on the way: CyberAgent based on blogs, Recruit based on classified advertising and HR, LINE based on sticker communications, and many more…

How big is Dentsu? US$ 37 billion, or US$ 19 billion or US$ 6 billion sales/year?

Managing Japan/West cultural issues via the Dentsu-Aegis-Network

As for many Japanese corporations, Dentsu’s challenge is to leverage a dominating position in Japan into a global business footprint, while managing the well-known cultural issues. Dentsu’s approach was to acquire the French/UK agency Aegis, and then via Dentsu-Aegis acquire a string of agencies all over Europe:

Dentsu dominates Japan’s advertising space, and is a very very strong force in Japan’s media industry sector, through control and management of major advertising channels with an overwhelming market share in Japan, and has been working hard to leverage its creative power and strength in Japan into a larger global footprint.

Japan’s mobile telecommunications sector continues to grow

The global mobile internet and smartphone revolution started in Japan in 1999, and Japan’s mobile telecommunications market is the world’s most advanced and most vibrant. Much mobile innovation and inventions, such as camera phones, color screens for mobile phones, mobile apps (i-Appli in Japan), and mobile payments were invented and first to market in Japan.

Globally the first mobile internet started in Japan in February 1999 when NTT-Docomo brought i-Mode to market. NTT-Docomo did not succeed to develop global business based on i-Mode, however, SoftBank took the lead, and is now building a global business built on Japan’s telecommunications sector’s strengths.

To understand Japan’s telecommunications market read our report:

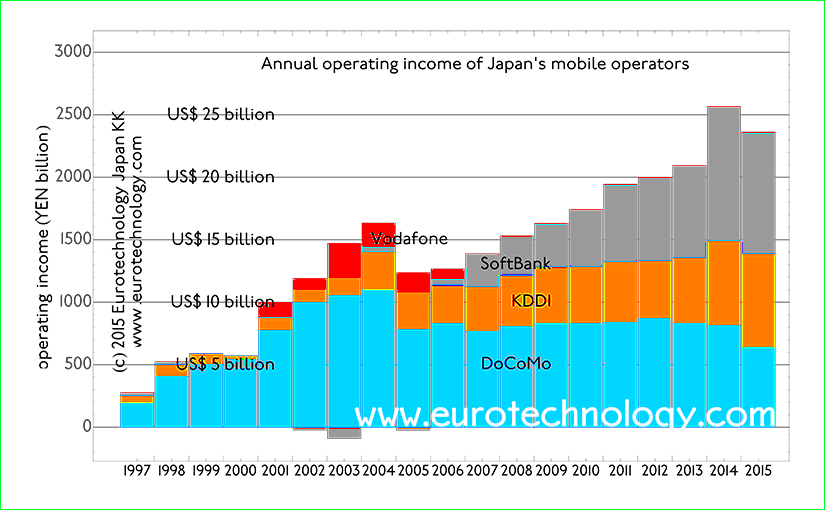

Japan mobile operators grow revenues to over US$ 170 billion in FY2014

While former monopoly operator NTT-Docomo’s business continues to shrink since its peak in 2002, KDDI is growing its predominantly domestic Japanese business slowly but steadily.

SoftBank on the other hand drives rapid growth with domestic Japanese acquisitions (Vodafone-Japan, Japan Telecom, eMobile and Willcom) and overseas acquisitions, which include US operator SPRINT, US mobile phone retailer BrightStar, Finnish game company SuperCell and many others – not to mention SoftBank’s investment in Alibaba.

Japan’s top three mobile operators combined revenues grow to over US$ 170 billion

Operating profits rise to approx. US$ 25 billion in FY2014

Operating profits and net profits are steadily increasing for Japan’s three mobile operators combined.

Former monopoly operator NTT-Docomo’s operating profits peaked in 2002, and have been steadily decreasing since this peak.

Both challengers KDDI and SoftBank on the other hand are growing operating profits steadily: KDDI mainly domestically in Japan, with relatively small global business, while SoftBank has dramatically increased business outside Japan with a series of acquisitions and investments, including US operator Sprint, US mobile phone distributor BrightStar and Finnish game developer SuperCell.

Operating income of Japan’s three mobile operators combined increases to approx. US$ 25 billion

To understand Japan’s telecommunications market read our report:

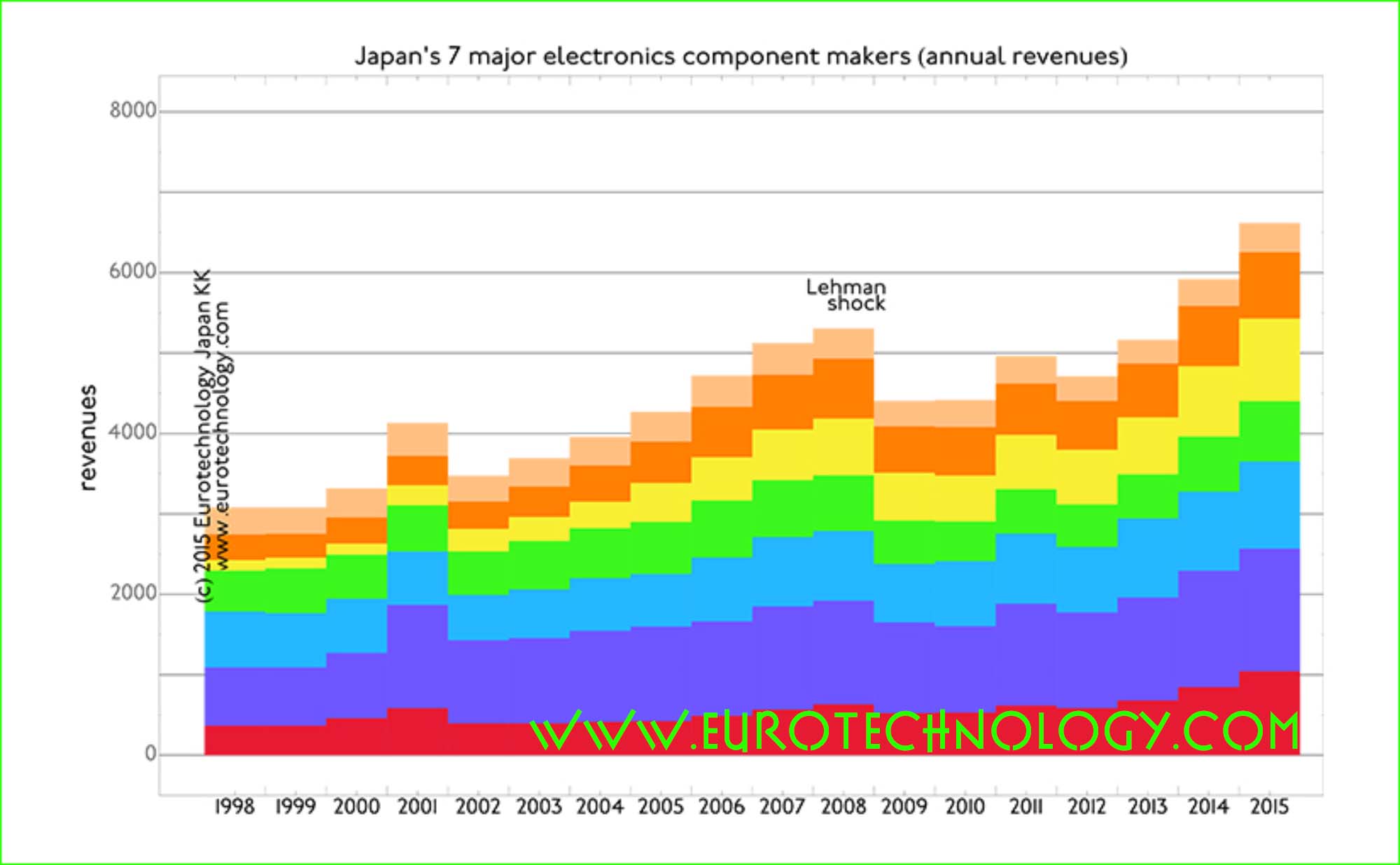

Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

At the Bank of Kyoto’s New Year celebration meeting, Japan’s stagnation and need for globalization were center of discussion – despite focus on globalization, the present author was more or less the only non-Japanese invited and attending(!).

The Chairman of Japan’s Industry Federation KEIDANREN, Mr Sakakibara (Chairman of Toray (東レ株式会社)), deplored that Japan’s economy is the only major industrial country not growing, and emphasized the need to overcome Japan’s well known Galapagos syndrome.

In an effort to overcome lack of growth in Japan, Japanese companies over the last years have been extremely active acquiring European technology companies – actually our company advised several Japanese companies’ M&A teams on European acquisition strategies and opportunities.

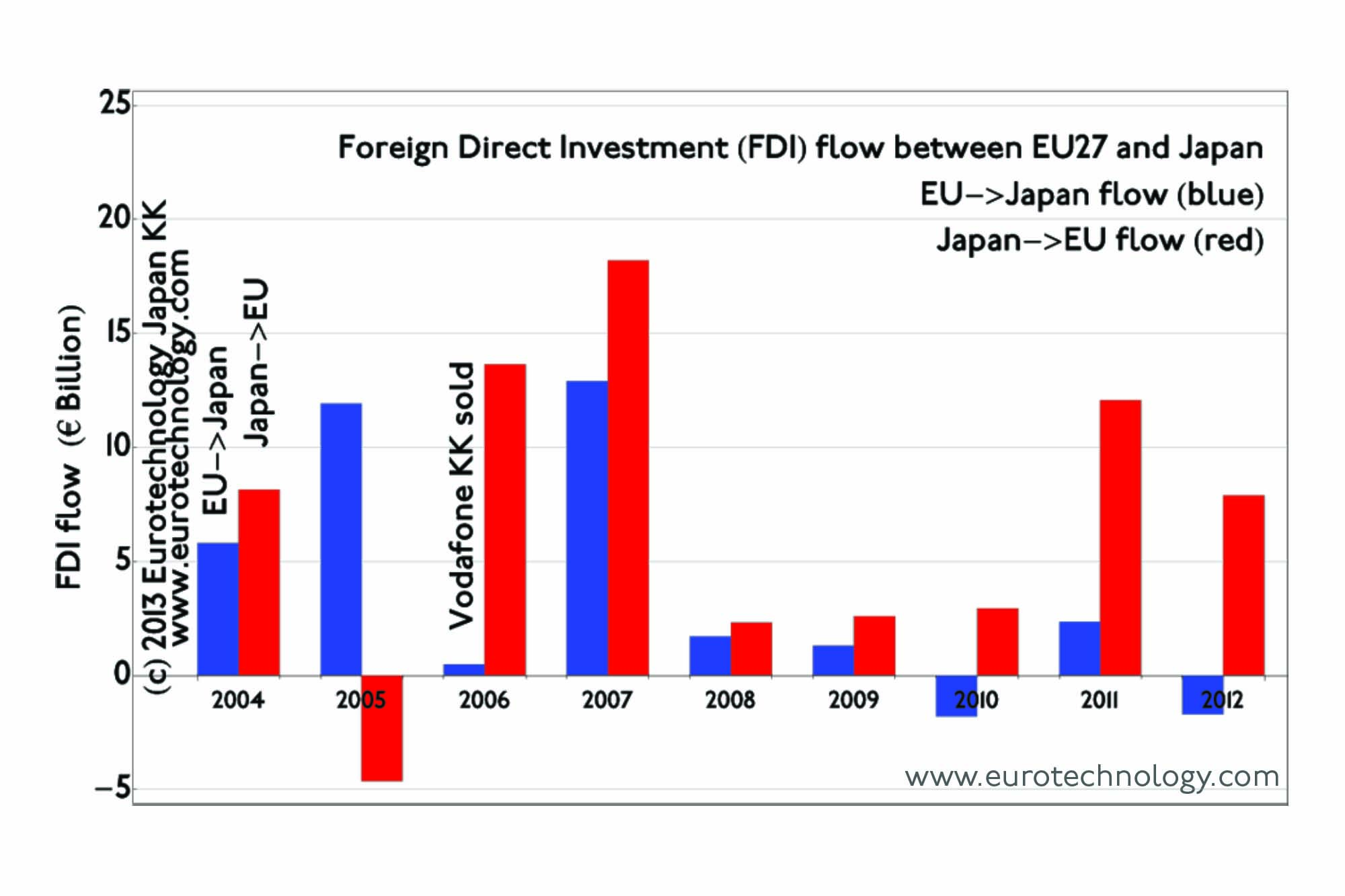

Japanese companies are particularly active acquiring European technology companies – this year alone, the EU-Japan investment registry shows Japanese acquisitions in Europe totaling € 6 billion – far more than European acquisitions in Japan this year.

It is well-known that EU <-> Japan post-merger management requires substantial management know-how. While such management known-how has been built up between US-Japan over many years, EU-Japan investments had only a shorter time to develop, and in many cases companies are not willing to invest sufficiently in such know-how. As a consequence the majority of EU <-> Japan investments has failed unfortunately – poster-children are the failures of Vodafone’s acquisitions in Japan and the failures of Docomo’s investments in EU, and there are many more examples.

To overcome these problems, several recent Japanese investments are substantial investments but short of 100% where local European management is kept in place – following the Renault-Nissan success story. Indeed, Carlos Ghosn has emphasized that the Renault-Nissan investment would probably have failed, had it been a 100% take-over.

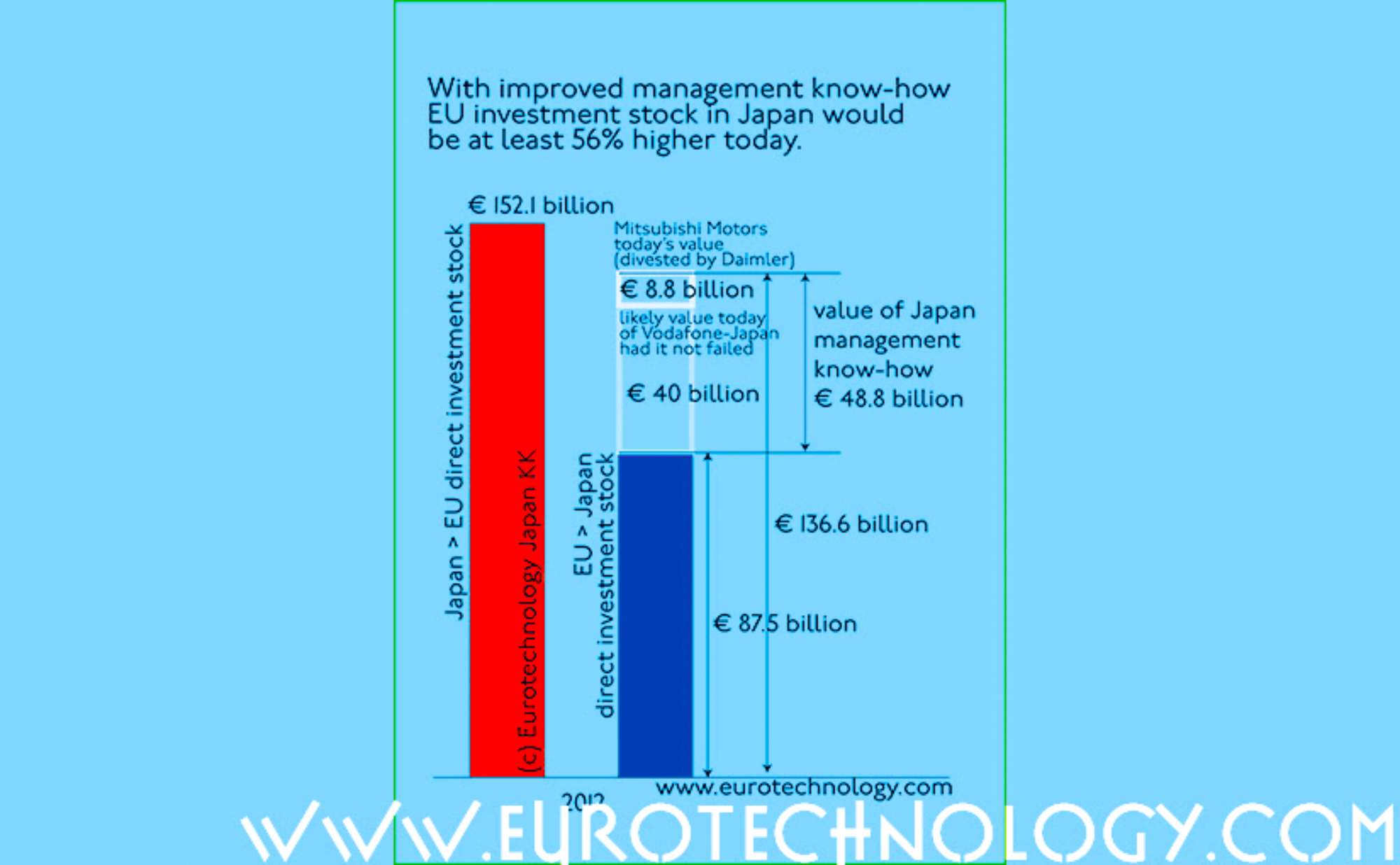

EU direct foreign investment into Japan could be 56% higher!

With improved management skills, EU owned business in Japan could be at least € 50 billion high than it is today

Many companies would wish to have a larger business in Japan, and generally the overall amount of direct EU investment in Japan is considered low. We show below that the value of EU investments in Japan could be at least € 50 billion higher than they are today, if some decisions had been taken differently.

We found a way to measure the value of management skills!

We analyzed the EUROSTAT data for direct investments between Japan and EU, and combining the EUROSTAT data with stock market capitalization data of relevant public companies we found a way estimate the value of management skills and management decisions in the EU-Japan direct investment field!

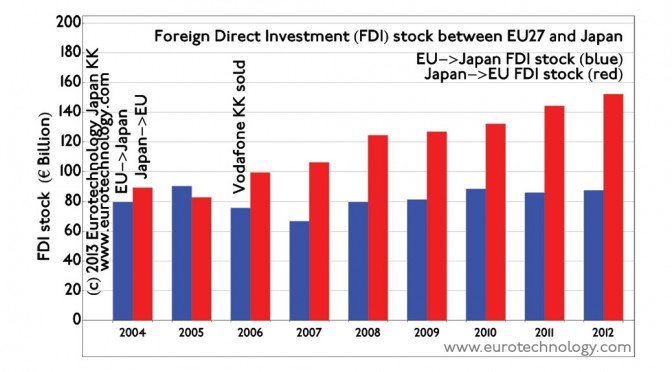

The figure above shows the EUROSTAT data for direct investment by EU companies in Japan and vice-versa:

the combined total of Japanese direct investment stock in EU (i.e. the acquisition of EU based companies by Japanese companies) in 2012 was about € 152.1 billion,

while the combined total of EU investment stock in Japan (i.e. the acquisition of Japanese companies by EU companies) in 2012 was about € 87.5 billion – substantially lower.

The fact of a relatively low EU investment stock is often superficially explained by “Japan is a closed country”, “cultural differences”, “low profitability in Japan”, “Japan is unattractive for foreign investment” etc.

Actually, the figure above shows, that if Vodafone would have been successful in managing Japan Telecom, that Vodafone had acquired, and if Daimler would have been successful in managing Mitsubishi Motors that Daimler had acquired, total EU investment stock in Japan would be at least € 50 billion higher than it is today.

How do we arrive at this estimation?

Mitsubishi Motors value today

Determining the value of Mitsubishi Motors today is straight forward. Mitsubishi Motors is a public company, traded on the Tokyo Stock Exchange (Securities Code 7211), and as of September 10, 2014, the market capitalization is YEN 1197 Billion = € 8.8 billion. If Daimler would have successfully managed Mitsubishi Motors Daimler would today own Mitsubishi Motors with a valuation of € 8.8 billion, and potentially even higher because of synergies.

Estimating the value of Vodafone’s acquisitions in Japan, had it been successful

Estimating the value of the companies Vodafone would own today in Japan, had it been successful in managing the company Japan Telecom it had acquired is more complex.

Essentially Vodafone acquired Japan’s 2nd largest full-service fix-net, internet, data-center and mobile general telecom operating company Japan Telecom (which had been built on railway rights of way, and had been majority owned by Japanese railway companies, before Vodafone acquired Japan Telecom). In about 30 or more separate investment banking transactions (which made investment bankers very happy), Vodafone acquired Japan Telecom, then split the company into several parts, and all parts in the end are today owned by SoftBank. The major transaction was the sale of Vodafone KK to SoftBank, however in total there were about 30 or more transactions.

As of today (September 10, 2014), there are three general telecom operating companies in Japan’s telecom market:

NTT Group, (Tokyo Stock Exchange Code 9432), market cap YEN 8025 billion = € 58 billion

NTT-Docomo (Tokyo Stock Exchange Code 9437), market cap YEN 8128 billion = € 59 billion

NTT-East

NTT-West

NTT-Communications

NTT-Data

and 100s more subsidiaries

KDDI: (Tokyo Stock Exchange Code 9433), market cap YEN 5655 billion = € 41 billion

SoftBank: (Tokyo Stock Exchange Code 9984), market cap YEN 9545 billion = € 69 billion

Therefore, if Vodafone would have succeeded in managing the company Japan Telecom it had acquired, it can be expected that a fictitious “Vodafone-Japan 2014” today would have a market value on the order of somewhere in the range between € 40 billion (KDDI) and € 70 billion (SoftBank). Now, since Vodafone – if it would have been successful and continued to develop successfully until this day in Japan, would not have the Alibaba and Yahoo-Japan, and 1500 other investments that SoftBank owns, nor the dominating market share that Docomo owns in Japan, we can assume that a fictitious “Vodafone-Japan 2014” would have a valuation similar to the one KDDI has today. Thus we conclude that Vodafone if it had been successful in managing Japan Telecom, would today own a business in Japan worth about € 40 billion.

Of course there are many more companies than Vodafone and Mitsubishi-Motors & Daimler, but because of their enormous size, in terms of statistics these companies totally dominate the overall statistics.

Estimating the value of Japan management know-how: € 50 billion in the case of Vodafone and Mitsubishi Motors/Daimler

We argue now, that if Daimler would have known how to manage Mitsubishi Motors correctly, and if Vodafone would have known how to manage Japan Telecom correctly, then today this knowledge would have created value of about € 50 billion in Japan, and the EU investment stock in Japan would be about € 50 billion (56%) higher than it is today.

The pitfalls and traps facing EU companies over managing Japanese companies

Foreign companies doing business in Japan face a number of dilemmas. Maybe the biggest dilemma is a situation which arises, when there is no Japan know-how represented on the Board of Directors of the mother company. This was the case for Vodafone, and it took Vodafone’s CEO and Board of Directors several years to realize that Japan Telecom could not be managed with the same “standard global management methods” as in all other markets. At that time, when Vodafone’s global CEO realized that “Japan is special”, Vodafone removed Vodafone-Japan from reporting to a Singapore-based Asia-GM, and moved Vodafone-Japan to report directly to the CEO, however this was only of many other problems, and also came far too late. NOKIA’s NSN also made a similar move years later, fortunately not too late. Read here for a more detailed discussion of the Vodafone-Japan case.

Another dilemma regularly arises about the management and governance structure of foreign subsidiaries in Japan. There are 100s of ways of organizing the management of foreign subsidiaries in Japan, and “cookie-cutter” approaches usually fail.

There are many more dilemmas, and this article shows, that solving these dilemmas correctly is worth many billion Dollars/Euros in the case of large corporations, and of course also of substantial value for small corporations and venture startups.

With better Japan management know-how, the EU investment stock in Japan could be at least € 50 billion higher:

Nokia strengthens No. 1 market position in Japan’s mobile phone base station market!

Japan’s mobile phone base station market

Japan’s mobile phone base station market is about US$ 2.6 billion/year and for European companies Ericsson and Nokia the most important market globally, although certainly also the most difficult one.

Nokia is No. 1 with a 26% market share, and Panasonic is No. 5 with 9% market share.

European investments in Japan

Nokia acquiring Panasonic’s network division is one of many investments and acquisitions in Japan by European companies. For more details, see the EU-Japan M&A register.

Panasonic to focus on core business, Nokia to expand market share in Japan

Panasonic, after years of weak financial performance, is focusing on core business. Nikkei reports that Panasonic is planning to sell the base station division, Panasonic System Networks, to Nokia.

Succeeding in Japan at the second try, learning from initial failure:

We see a pattern here: after failing spectacularly trying to build a mobile phone business in Japan for almost 20 years without success, Nokia is now winning the second time round.

It can be hard for foreign companies to build a business in Japan, and many fail. Interestingly, there is a long list of famous companies that succeed on their second attempt after initial failure, this list includes:

IKEA: failed first time in 1974, succeeds now

DAIMLER: failed spectacularly first time with Mitsubishi Motors, now successful with Mitsubishi Fuso trucks – read the time line here

NOKIA: failed first time after trying for 20 years (1989-2008) to sell mobile phones in Japan, now successful with mobile phone base stations and network infrastructure

Our analysis of Japan’s mobile phone base station market shows, that Nokia became No. 1 in Japan’s base station market with the acquisition of Motorola’s base station division. Acquisition of Panasonic System Networks will expand Nokia’s NSN to expand market leadership in Japan’s mobile phone base station market.

I believe without success in Japan’s mobile phone base station market, there is a big chance Nokia as a company, or at least Nokia’s NSN division would not exist any more at all today.

With a market share of 26%, approx. US$ 700 annual sales in Japan, Nokia is No. 1 market leader in Japan followed by Ericsson on 2nd position. With the acquisition of Panasonic’s base station division, Nokia should be able to expand its market share beyond 26%+9% = 35% and expand its leadership, especially via Panasonic’s deep relationship with Docomo.

Because Docomo with its very deep pockets, is traditionally the first globally to develop and bring to market the most advanced radio technologies, a deeper relationship with Docomo will also help Nokia to develop and bring to market new communication and radio technologies. Thus I believe the impact on Nokia will be far more than an increase of the market share in Japan from 26% to 35%.

Panasonic System Networks

Panasonic System Network’s market share is estimated at around 9% of Japan’s mobile phone base station market, while international sales are essentially non-existent. Thus Panasonic System Network’s global market share is negligible, giving Panasonic little possibility for the scale necessary to operate a stable profitable longterm base station business.

Japan’s mobile phone handset makers and base station makers have for many years focused on serving Japan’s internal market only, and in particular have focused on Japan’s No. 1 mobile phone operators NTT Docomo. This gave Japan’s mobile phone base station makers a temporary home advantage, however with the value shift from hardware to software, they lack scale, and are subsequently uncompetitive globally. More about Japan’s Galapagos effect here.

Over the last 15 years since 1998, Panasonic has shown no growth in revenues, and average net losses of YEN 85 billion (US$ 0.85 billion) per year, as typical for most of Japan’s top 8 electronics companies and as we analyze in detail in our report on Japan’s Electronics Industries.

Panasonic is on 5th rank with about 9% market share in Japan’s mobile phone base station markets, and has little chance and not the capital to scale its base station and mobile phone businesses globally. For Panasonic in it’s current very limited financial situation, focus on core business areas is very prudent.

The context: EU investments in Japan

While Japanese investments in Europe are booming, recently European investments in Japan have been stagnating after Vodafone’s withdrawal from Japan, and there are very few new European investments in Japan. Could it be that Nokia’s investment in Japan starts a new trend of renewed European investments in Japan?

Understand Japan’s telecommunications markets

Report on Japan’s telecommunications industry

(approx. 270 pages, pdf file)

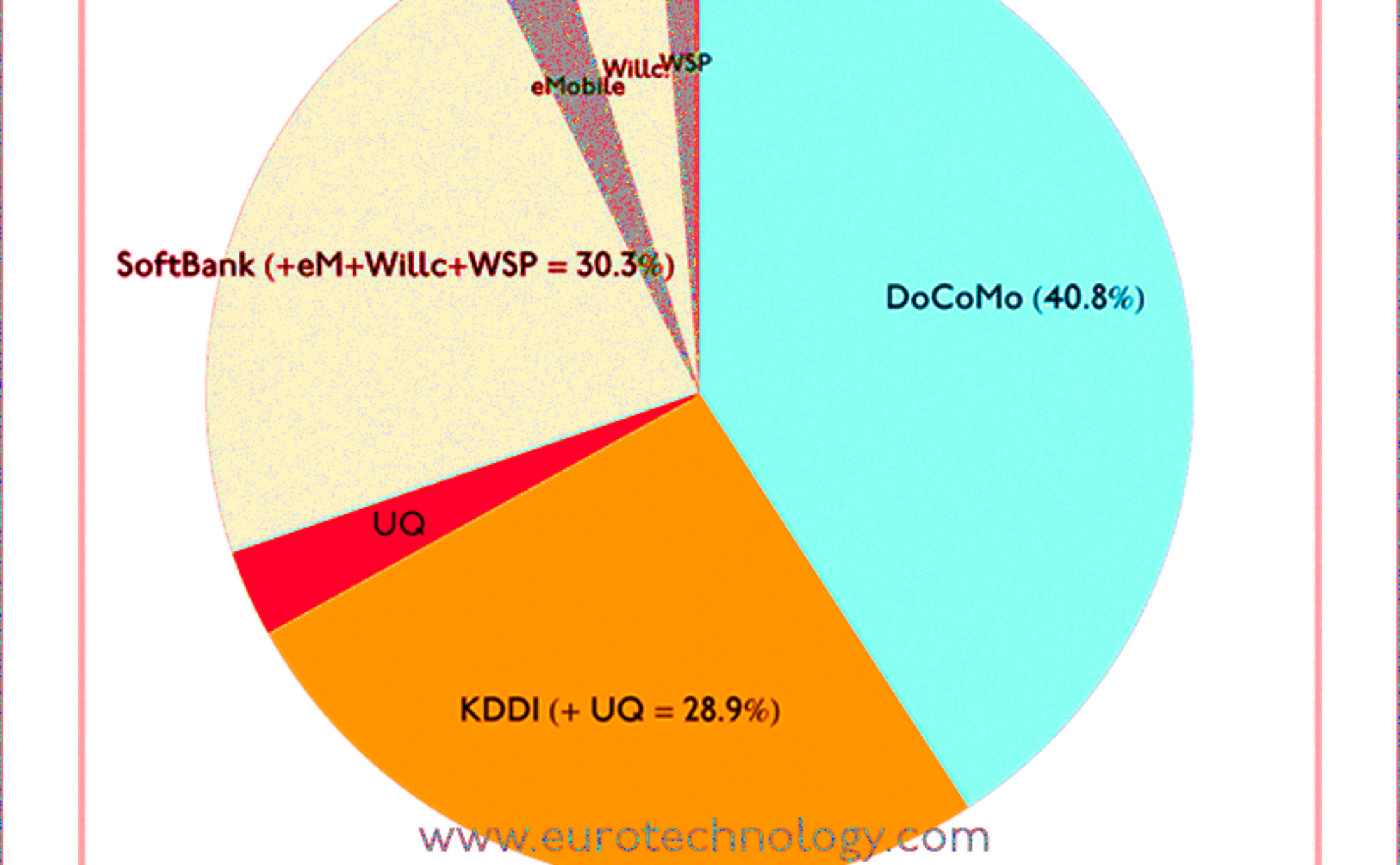

Many press articles get SoftBank market share in Japan wrong

With SoftBank‘s acquisition of US No. 3 mobile operators Sprint and the possibility that Softbank/Sprint will also acquire No. 4 T-Mobile-USA, SoftBank and Masayoshi Son are catching global headlines.

SoftBank market share in Japan: Many media articles report wrong data, because they forget to include group companies

These articles state SoftBank’s market share in Japan’s mobile market as 25% and say that KDDI Group has more subscribers than Softbank Group in Japan, but is this really true?

SoftBank recently acquired eMobile/eAccess, and has been the court-appointed reconstruction partner of Willcom, after Willcom’s financial failure. Therefore eMobile/eAccess and Willcom are also part of the SoftBank group, and SoftBank plans to merge both. In addition, Wireless City Planning (WCP) are also part of the SoftBank group. You will find these transactions, the logic and reasoning behind them explained in great detail in our reports on SoftBank and on eAccess/eMobile.

List of mobile operators on Japan’s market today:

We have the following mobile operators currently in Japan – subscription market shares are shown in brackets (subscriber numbers for Docomo, KDDI and Softbank are as of February 28, 2014, while for other operators the latest officially reported numbers are used):

eMobile/eAccess (note: eMobile, eAccess and Willcom are now combined into Ymobile)

Willcom (now merged into Ymobile)

Wireless City Planning (WCP)

fixed line and other businesses

several virtual mobile operators, e.g. Japan Communications Inc. who lease communications capacity e.g. from Docomo and retail this leased capacity to their own subscribers

The SoftBank group including eAccess/eMobile, Willcom and Wireless City Planning has actually more than 30% of Japan’s mobile subscriber market – not 25% as some articles write.

For detailed market data, statistics and analysis of Japan’s highly competitive mobile communications market, read our market report on Japan’s telecom markets, which includes analysis and data for Japan’s wireless, fixed, ADSL and FTTH markets, and detailed financial data, analysis, and comparison of the financial performance of NTT, NTT Docomo, SoftBank and KDDI.

We are also preparing reports on Japan’s cloud and data center markets –

Subscriber market shares in Japan’s wireless communications markets for each of the competing groups: Docomo, KDDI and SoftBank.

Learn more about SoftBank, Masayoshi Son, and his 30/300 year vision for SoftBank

Start-up Nation Israel 2014 – Israel Japan Investment Funds meeting on March 4, 2014 at the Hotel Okura in Tokyo

Israeli Venture funds introduce Israeli ventures to Japanese investors

Acquisition of Viber by Rakuten draws attention in Japan to Israeli ventures

The recent acquisition of the Israel-based OTT (over the top) communications company Viber by Rakuten for US$ 900 Million has drawn attention in Japan to Israel’s innovative power, however many Japanese companies are already cautiously investing in Israel while keeping a low profile, we learnt at the “Start-up Nation Israel 2014” Israel Japan Investment Funds meeting on March 4, 2014 at the Hotel Okura in Tokyo.

Most of the companies presented at the conference were highly sophisticated computer security, medical equipment, and similar “mono zukuri” type ventures, but also included a “selfie” app for auto-portrait or group photos using iPad or iPhone.

By the way: our company is currently working to sell an Israeli venture company to Japan as an exit for investors, and to accelerate business development in Japan for this company.

Her Excellency, Ambassador of Israel to Japan, Ms Ruth Kahanoff opened the conference:

Her Excellency, The Ambassador of Israel to Japan, Ms Ruth Kahanoff

Economic Minister of Israel to Japan, Mr Eitan Kuperstoch explained that while there is substantial investment in Israel’s ventures by many major Japanese corporations, there is much scope for increases. Japan’s investment added together are on the order of 1% of foreign direct investments to Israel:

Economic Minister to Japan of Israel, Eitan Kuperstoch

Pitches by Israeli Venture Funds

BRM Group: actually a privately held fund, strictly speaking not venture capital

CHIMA Ventures: medical devices, minimal invasive surgery tools.

TERRA Venture Partners: Terra invests in about 16-20 (4-5 per year) for a 1-2 year incubation period, followed by a “cherry picking” process. Terra VP invests in companies surviving the “cherry picking”. Veolia, GE, EDP, Clearweb, Enel are partners.

Giza Venture Capital: 5 funds, US$ 600 million under management, 102 investments, 20 active, 38 exits. Examples are: XtremIO, Actimize, Telegate, Precise, Plus, msystems, cyota, Olibit, Zoran, XTechnology. A particular success story is XtremIO: the team of 21 people (including secretary) turned US$ 6 million investment into a US$ 435 million cash sale to EMC.

StageOne Ventures: Early stage US$ 75 million fund, 17 investments.

Gillot Capital Partners: seed and early stage. Focus: cyber security.

SCP Vitalife Partners: 2 funds, US$ 230 capital under management.

Magma Venture Partners: focus on information and communications sector. Created over US$ 2 billion in acquired company value. Biggest success story: waze (crowd sourced location based services), return on capital investment: 171-times.

OrbiMed Healthcare Fund Management: largest global healthcare dedicated investment firm.

Nielsen Innovate:

Panel discussion of Israeli Venture Capital Fund Managers and the Vice-President of Japan’s Venture Capital Association

Presentations and Panel discussion

Arik Klienstein: Driving innovation in Israel – the 8200 impact

8200 is a unit within the Israeli Defence Forces similar to the US NSA – technology based intelligence collection. 8200 veterans lead many Israeli start-ups including NICE, Verint, Check Point, paloalto.

8200 and the start up culture:

Select the best people out of high school or college

Short first formal training. Most of training done on the job

Flexible dynamic organizational structure

Direct and constant relationship with the end user

“Think out the box” mentality – no assumptions. Hierarchy-less flat structure

Must win attitude!

Tal Slobodkin (Talpiot 18 Graduate): The Talpiot program

Talpiot is Israel’s elite Israel Defense Forces training program, dedicated to create leading research and development officers for the various branches of the Israeli Defence Forces. Program was created in 1979, about 1000 graduates today.

Selection process:

starts with 15,000++ high school seniors

100-150 attend next level of leadership assessment

50-75 reach final selection committee

30-40 enter the program

25-35 graduate

Training and assignment:

three full academic years

full dual degree in Maths and Physics, most graduate additionally in Computer Science or other subjects

military training

significant exposure to all cutting edge military and non-military innovation

develop management skills

graduates pick own final assignment

minimum assignment is additional 6 years, average tenure in Israeli Defense Forces is 10 years

Notable graduates:

Yoaf Freund: Professor at UC San Diego, Goedel Prize winner

Elon Lindenstrauss, Professor of Mathematics at the Hebrew University and winner or 2010 Fields Medal

Marius Nacht, co-founder of Check Point Software

Eli Mintz, Simchon Faigler, Amir Natan, founders of Compugen Ltd

Founders of XIV, sold to IBM for US$ 400 million

Eviatar Metanya, head of National Cyber Bureau

Ophier Shoham, head of Israel’s Defence R&D Agency (Israel’s DARPA)

Elchana Harel (Harel-Hertz Investment House): Japanese investments in Israel

94 Japanese investments in Israeli High-tech during 2000-2014:

ICT: 41 investments

Semiconductors: 25 investments

Life sciences: 11 investments

VC funds: 17 investments

Characteristics:

Most investments are strategic, not financial, not exit driven

Most investments are direct into target companies, and relatively small by global standards: up to US$ 3 million

In many cases “silent investments”: e.g a Japanese electronics company does not want their Japanese competitors to know that they invest in Israel

Japanese investors mostly follow Israeli or US lead investors. Japanese investors seldom lead.

Japanese acquisitions in Israel:

Nikken Sohonsha: NBT

Yasukawa Robotoics: Yasukawa Israel (Eshed), Argo Medical Robotics

David Heller: cooperation of Israeli investment funds with Japan

Israel’s venture capital fund industry was created by Israel’s Government creating the Yozma Fund of Funds: Israel’s Government invested a total of US$ 100 million in 10 VC funds (US$ 10 million per fund) under the condition that these funds had to attract much larger non-Government investment. In total the Yozma Fund of Funds invested US$ 100 million and resulted in a VC fund industry with a total of US$ 17 Billion of VC funds raised since 1993.

There is a relatively large number of Japanese investments in Israeli funds, however, the combined total investment is rather low, approximately 1% of all foreign investments in such funds. Thus there is much scope for increased Japanese investments in Israeli funds and ventures.

London Stock Exchange formed the Tokyo AIM market as a joint venture with Tokyo Stock Exchange and now withdraws from this venture and from Japan

Initially, London Stock Exchange and Tokyo Stock Exchange created Tokyo-AIM as a joint-venture company in order to create a jointly owned and jointly managed AIM Stock Market in Tokyo, modeled according to the very successful London-AIM model.

“Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own” NIKKEI on March 26, 2012

However, on March 26, 2012 NIKKEI reported that “Tokyo Stock Exchange has learnt enough from the London Stock Exchange to set up a similar market on its own. TSE plans to improve the rules of its own new market, so that TSE can create a more welcoming market” (our translation of the original Japanese NIKKEI article to English).

London Stock Exchange withdraws from joint venture, and Tokyo Stock Exchange takes 100% control of Tokyo AIM

London Stock Exchange withdrew from the venture, and Tokyo Stock Exchange took over 100% of Tokyo-AIM. Essentially, London Stock Exchange AIM’s venture into Japan failed, while the stock market created by the venture continues without London Stock Exchange’s involvement. As explained in our blog here, these events are very very similar to what happened with NASDAQ about 10 years earlier!

Tokyo AIM name changed to TOKYO PRO Market and TOKYO PRO-BOND Market

In 2012, the name was changed from Tokyo-AIM, to TOKYO PRO Market and TOKYO PRO-BOND Market. Details can be found here:

EU Japan investment stock is expected to increase with the future Economic Partnership Agreement

European direct investments into Japan, European acquisitions in Japan

EU investments in Japan have been relatively constant around EURO 80 billion. There has been a marked reduction in EU investment in Japan in 2006 due to the withdrawal of Vodafone from Japan with the sale of Vodafone KK to Softbank for approx. EURO 12 billion (find details of the Vodafone-SoftBank M&A transaction here). This reduction of EU investment stock in Japan is clearly visible in the graphics below in 2006 and 2007.

Japanese direct investment in Europe, Japanese acquisitions in Europe

Japanese investments in EU are steadily increasing, as Japanese companies are seeking to grow business outside Japan’s saturated market, and as Japanese companies acquire European companies for market access, technology and global business footprint. In 2012 the total investment stock of Japanese companies in the EU-27 has reached around EURO 150 billion.

EU Japan investment flow is mainly from Japan to Europe and totals about EURO 10 billion per year

Investment flow between EU and Japan shows strong impact from the Lehmann shock economic downturn, and was very quiet between 2008 and 2010. In recent years, mainly Japanese investments to Europe have picked up, and currently about EURO 10 billion per year flow from Japan to Europe, Japanese companies acquiring European companies to globalize and also to pick up known-how and technologies.

Investment flow from EU to Japan remains at relatively low levels around EURO 1 billion annually, while investments by Japanese companies in the EU are on the order of EURO 10 billion per year currently.

Japan to Europe direct investment register:

Investment flow recently is almost one way from Japan into Europe.

EU Japan investment flow is mainly from Japan to Europe and totals about EURO 10 billion per year

With the expected Economic Partnership Agreement (EPA) we expect investment flows to increase in both directions.

The pressure to globalize, and saturation of Japan’s markets drives Japanese corporations to invest in Europe, therefore we expect the future Economic Partnership Agreement between Japan and EU to stimulate further Japanese investments in Europe more than in the Europe -> Japan direction.

SOMPO, a Japanese insurance company owned by NKSJ Holdings, acquired Canopius in order to globalize

In order to globalize, Japanese insurance company Sompo Japan (株式会社損害保険ジャパン), part of the insurance group NKSJ Holdings (NKSJホールディングス株式会社, TSE / JPX: No. 8630) announced yesterday the acquisition of 100% of the UK re-insurer Canopius Group Limited, operating on Lloyd’s for UKL 594 million (US$ 972 million), from the current owners. Current majority owner of Canopius is Bregal Capital.

Canopius will keep the brand, company name, and management team.

Canopius, is an insurance group, one of the top ten insurers in the Lloyd’s market, was founded in December 2003, almost exactly ten years ago, via a Management Buy-Out (MBO) with UKL 25 million capital, which grew about twenty-fold to about UKL 500 million today, and today has about 560 employees.

Canopius is named after Nathaniel Canopius, native of Crete, who studied at Balliol College, Oxford, apparently introduced coffee drinking to Oxford around 1637 (according to the Canopius website), and later became Archbishop of Smyrna (Source: “Anglicans and Orthodox, Unity and Subversion, 1559-1725”, by Judith Pinnington, 2003, ISBN 0-85244-577-6, page 15).

Stanford Economics Professor Takeo Hoshi thinks that there is a 10% chance that Abenomics will succeed to put Japan on a 2%-3% economic growth path, while the most likely outcome will be 1% economic growth. Read our notes of Professor Hoshi’s talk in detail here.

Can Japanese companies globalize?

“Globalization” of course is not an aim in itself. In Europe and USA there are plenty of companies which are very successful and not globalized. However, Japan could capture much more global value from technology and creativity by creating more global companies: the shining example is SoftBank.

Read legendary Masamoto Yashiro’s viewpoints about globalization at a recent Tokyo University brainstorming event by the President of Tokyo University (Masamoto Yashiro was Chairman of Exxon-Japan, of Citibank-Japan, and Shinsei-Bank, and Board Member of the Construction Bank of China). Masamoto Yashiro says that a change of mind-set is urgently needed.

Until March 11, 2011, Japan’s energy markets were essentially frozen in the structures created in 1952, which again resulted from the war-time nationalization of Japan’s electricity sector (see our Energy Report). Japan’s electricity markets alone are worth about US$ 200 million per year – and this market is now in disruption.

Recently I was invited to brief the Energy Minister of Canada, Mr Joe Oliver, and Sweden’s Trade Minister Dr. Ewa Björling about Japan’s energy markets. My briefings are based on our analysis, which you can find in our Energy Report, and Renewable Energy Report.

The liberalization of Japan’s energy markets will create winners and losers – comparing the financial performance of Japan’s electricity companies and gas companies is an indication of things to come. Actually, only Japan’s electricity markets are being liberalized currently, liberalization of Japan’s gas markets is still for the future.

Disrupting Japan’s game sector

Japan’s game makers have essentially created the global game market, and are ripe for disruption by smart phones and tablets one would think. Indeed, just three Japanese newcomers Gree + DeNA + GungHo alone (there are many more) create more annual net income than Japan’s top 9 game makers combined! The origin of this disruption by newcomers in Japan however is not created by Western companies, and not by smart phones, but goes back to the creation of i-Mode in February 1999 (and some months later EZweb and Jsky). Recently the world is slowly waking up to the fact, that Japan’s game markets is one of the world’s biggest, if not the biggest… and hard for foreign companies to penetrate, unless done correctly…

TowerJazz acquires three of Panasonic’s large written off wafer fabs for around US$ 100 million

Massive market entry to Japan for TowerJazz

Nikkei (the world’s biggest business daily, see our J-Media report) reported as their top headline yesterday, that TowerJazz is planning to acquire interests in three of Panasonic’s reportedly largely written-off semiconductor fabs valued at about US$ 100 million.

Nikkei reports that Panasonic plans to spin out three fabs into a separate company, to be owned 51% by TowerJazz and 49% by Panasonic:

Uozu-shi in Toyama-ken (富山県魚津市)

in Tonami-shi in Toyama-ken (富山県砺波市), and in

Myoku-shi in Niigata-ken (新潟県妙高市)

TowerJazz entered Japan’s market by acquiring the Nishiwaki semiconductor fab near Nishiwaki-shi in Hiyogo-ken near Kobe.

TowerJazz is a leading Israel-USA foundry company traded on NASDAQ. TowerJazz in 2011 acquired a semiconductor fab in Nishiwaki-shi in Hiyogo-ken (兵庫県西脇市). The Nishiwaki fab was initially built by a joint-venture between Texas-Instruments and Kobe-Steel, and was later acquired by Micron. TowerJazz acquired the Nishiwaki-fab from Micron in 2011.

We believe that the driver for these transactions are both PUSH and PULL:

PUSH:

Panasonic’s need for capital

Panasonic’s need to withdraw from loss-making operations (Panasonic’s semiconductor operations reported YEN 20500 million (US$ 200 million) operating losses for revenues of YEN 184 billion YEN (US$ 1.8 billion) and need to focus on a smaller number of core businesses

need for investments in the semiconductor fabs to upgrade equipment and Panasonic’s difficulties to supply such capital

In the past Matsushita (Panasonic was previously named after its founder) was nick-named “Matsushita Bank” because of its solid financial situation. However on October 31, 2012, President Kazuhiro Tsuga announced that “Panasonic is an unusual company” referring to Panasonic’s financial predicament: Panasonic had reported YEN 754.2 billion (US$ 7.5 billion) net losses for FY2012 (ending March 31, 2013). At the same time, President Tsuga also announced a program to revive Panasonic. This event is known as the “Panasonic shock”.

Moving semiconductor fabs from Panasonic to TowerJazz management or co-management/co-ownership is a good example of how Japanese management can be globalized.

Its not well known in Europe and US yet, but SoftBank is a very large company, and aiming to become the world’s largest company

SoftBank is really a very large company, driven by the charismatic founder Masayoshi Son. To get a feeling for the size of SoftBank, while the investment in Supercell is a large amount of money by anybody’s standards, its about 5% of SoftBank’s acquisitions this year alone (in addition to M&A type investments, SoftBank also invests substantial sums in networking equipment and other telecom business infrastructure and data centers).

SoftBank invested in about 1500 companies, the most famous currently being Alibaba

Overall SoftBank invests in about 1500 companies or more: SoftBank takes a venture capital approach to this portfolio. Overall SoftBank investments are incredibly successful. As an example, look at the currently important Alibaba case:

Softbank acquired 36.7% of Alibaba in 2000 for US$ 20 million.

Alibaba’s market cap will be determined after its IPO, but currently figures between US$ 100 billion and even up to US$ 250 billion circulate. This would value SoftBank’s 36.7% stake in Alibaba at somewhere between US$ 36.7 billion and US$ 91 billion, a return on initial investment between 1835 and 4550 times!

While SoftBank’s overall portfolio is outstandingly successful, not every single investment is successful, as is normal for a venture type investment style.

This year alone, SoftBank investments and acquisitions amount to about US$ 30 billion

This year SoftBank’s direct investments and acquisitions alone are on the order of US$ 30 billion and include:

mobile phone distributor Brightstar which is another US$ 1.26 billion

Talouselämä questions about SoftBank and its investment in Supercell and my answers:

What are SoftBank’s targets? SoftBank wants to become one of the most important companies globally, has a 30 year plan and a 300 your plan

How does SoftBank integrate acquisitions? Case-by-case. In some cases, e.g. Vodafone-Japan KK, Softbank totally absorbed the company and its assets became much of the starting point of SoftBank Mobile, however today’s SoftBank Mobile is a dramatically different company compared to Vodafone-Japan KK, which according to Masayoshi Son in recent interviews “was going south”.

How important are games for Softbank? SoftBank is major investor in GungHo, which is one of the world’s most successful smartphone game companies.

What other businesses does SoftBank concentrate on, and what kind of goals does it have? SoftBank today focusses on mobile communications and internet, however is also active in other areas. For example, SoftBank is aggressively building an energy business, with focus on renewable energy, which includes renewable energy investments in Mongolia for example. SoftBank‘s more than 1500 investments include Alibaba and Yahoo Japan KK.

To understand SoftBank better, read our report on SoftBank, an analysis of SoftBank, history, current data, and the context.

Understand Japan’s games sector and its disruption

Report “Japan game makers and markets” (pdf file, approx 400 pages, 140 figures)

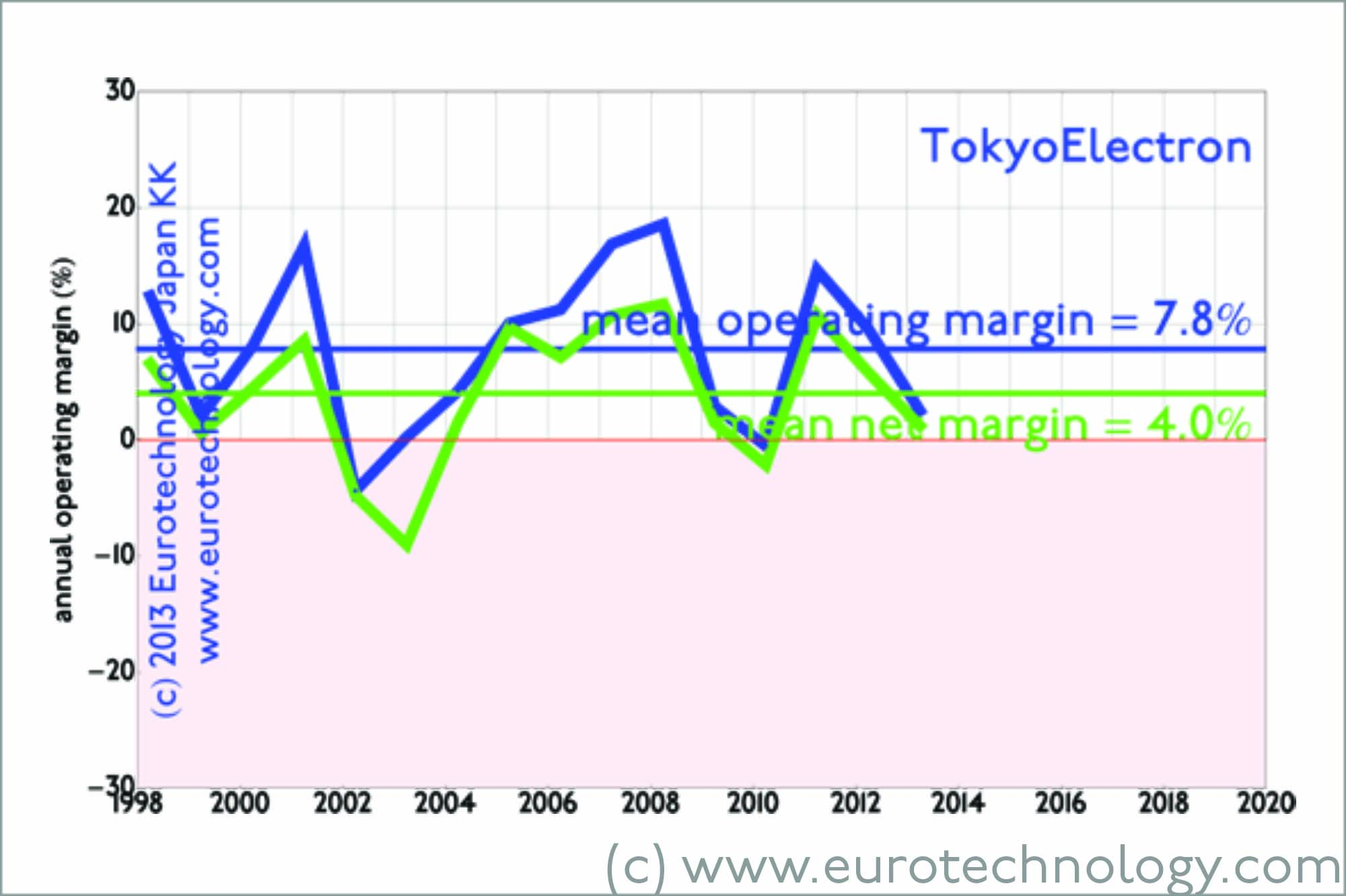

Global No. 1 (Applied Materials) and No. 3 (Tokyo Electron) plan merger

Subject to regulatory approval in different jurisdictions

Global No. 1 (Applied Materials) and No. 3 (Tokyo Electron) semiconductor manufacturing equipment makers on September 24, 2013 announced their “merger of equals” – creating a company with a nominal market capitalization of US$ 31.5 Billion, in one of the largest mergers of a Japanese company with a foreign company ever. I was this morning interviewed by BBC to comment – here additional background material and comments.

Tokyo Electron: excellent results in a very difficult industryApplied Materials margins

Summary of the Tokyo Electron & Applied Materials merger:

A new company will be created:

combined market capitalization of US$ 31 billion and about 24% market share

dual headquarters in Tokyo and Santa Clara, incorporated in The Netherlands

Chairman=Tetsuro Higashi (Tokyo Electron)

CEO=Gary Dickerson (Applied Materials)

CFO=Bob Halliday (Applied Materials)

ownership – corresponds almost exactly to the market capitalization ratio:

68% Applied Materials shareholders

32% Tokyo Electron shareholders

Anti-trust approval still outstanding:

Anti-trust authorities in several jurisdictions are likely to examine this planned merger, however it seems likely that there will be no major problems, since the product portfolios of both companies are quite complementary.

Currently Applied Materials has about 14% market share of semiconductor manufacturing equipment and Tokyo electron about 10%, thus about 76% of the market are supplied by competitors.

Of course the “pricing power” of the combined company could increase in certain cases, which could be also a driving force for this merger.

Market shares of IC manufacturing equipment market pre merger

Applied Materials: US$ 5.5 billion (14.4%)

ASML: US$ 4.9 billion (12.8%)

Tokyo Electron: US$ 4.2 billion (11.1%)

Lam Research: US$ 2.8 billion (7.4%)

KLA-Tencor: US$ 2.5 billion (6.5%)

Market shares of IC manufacturing equipment market post merger

Applied Materials + Tokyo Electron: US$ 9.7 billion (25.5%)

ASML: US$ 4.9 billion (12.8%)

Lam Research: US$ 2.8 billion (7.4%)

KLA-Tencor: US$ 2.5 billion (6.5%)

“Merger of equals” – really?:

Yes and no. Ownership of the merged company is split between shareholders of Applied Materials (68%) and Tokyo Electron (32%) according to current market capitalization ratio, and both CEO and CFO will be from Applied Materials. This is a clear message to Japanese corporations that market capitalization does matter dramatically. As we have shown in previous posts, the market capitalization of Japanese electronics companies today is dramatically low (considering revenue size, the glorious past and future potential) – so in any similar merger “of equals” even Japanese electronics giants could be the junior partner. This point was also addressed in a recent presentation by Hiroshi Mikitani. These sensitive issues were extremely skillfully and successfully handled by Renault and Nissan. Carlos Ghosn has said in this context that he believes a full acquisition would not have been successful.

“One of the largest mergers between a Japanese and a foreign company” – if executed and successful

There is some confusion on this point in the news articles that I have seen. The current market capitalization of Tokyo Electron is approx. US$ 10.07 billion.

By far the largest acquisition of a Japanese company by a foreign company was the acquisition of the Japan Telecom Group by Vodafone. Since this acquisition was done (and later undone) by a large number of separate transactions, it is difficult to put a specific size on this acquisition. Our estimation is that this acquisition was on the order of US$ 20 billion or higher – and was not successful longterm, some reasons are outlined here.

Large scale acquisitions of Japanese companies by foreign companies include:

Japan Telecom Group acquisition by Vodafone (undone: now part of SoftBank)

Nikko Cordial acquisition by Citigroup (undone: now SMBC-Nikko)

Japan Leasing acquired by GE

Nissan Motor partnership with Renault (minority stake, not acquisition)

Applied Materials and Tokyo Electron – Tax:

Tokyo Electron + Applied Materials plan a joint holding company in The Netherlands. One reason is to have a neutral location following the spirit of “merger of equals”, but tax also plays a role:

Projected tax rate for new holding company on profits in The Netherlands: 17%

Current tax rate on profits for Applied Materials: 28%

Current tax rate on profits for Tokyo Electron: 37%

Applied Materials and Tokyo Electron – Cultural issues:

Not to be underestimated. In our view success of this merger is not guaranteed at all, and will depend to some extent to skillful management of the bridging cultural issues.

Our report on Japan’s electronics industries – mono zukuri:

M&A in Japan: Interview with Arthur Mitchell by Dr Gerhard Fasol