On 18 July 2016 SoftBank announced to acquire ARM Holdings plc for £17 per share, corresponding to £24.0 billion (US$ 31.4 billion)

SoftBank acquires ARM: acquisition completed on 5 September 2016, following 10 years of “unreciprocated love” for ARM

On 18 July 2016 SoftBank announced a “Strategic Agreement”, that SoftBank plans to acquire ARM Holdings plc for £24.0 billion (US$ 31.4 billion, ¥ 3.3 trillion) paid as follows:

SoftBank’s start in telecoms via the acquisition of Tokyo Metallic, SoftBank’s acquisition of Vodafone Japan in combination with having developed YAHOO-Japan into the leading internet service company in Japan, were among the most important stepping stones for SoftBank to become a key global player in mobile communications.

Masayoshi Son: unreciprocated love for ARM for 10 years

In the Nikkei interview of 3 September 2016, Masayoshi Son explains that he had an “one-sided / unreciprocated love for ARM” for at least 10 years, but decided to acquire SPRINT first. After acquiring SPRINT he had to pay down debt before being able to acquire ARM now.

ARM was founded on 27 November 1990 as Advanced RISC Machines, however the abbreviation ARM was first used in 1983 and initially meant “Acorn RISC Machines”.

Acorn Computers Ltd was founded in 1978 in Cambridge (UK) by Hermann Hauser and Chris Curry to produce computers, and its most famous product was the BBC Micro Computer.

ARM has built an ecosystem of IC design systems and platforms which are at the core of low energy consumption ICs and CPUs for smartphones and many other electronic devices and cars. ARM may become or already is one of the core technology companies for the Internet of Things (IoT).

SoftBank’s ARM Business Department’s name changed to “New Business Department”

Outside Japan there is a tendency to focus on one of the two co-founders, Akio Morita, however, as an engineer Masaru Ibuka was as least as important a co-founder.

Masaru Ibuka (井深大), co-founder

Masaru Ibuka (井深大) was a passionate engineer, and drove much of the technical product development, recruiting and leading some of the best engineers.

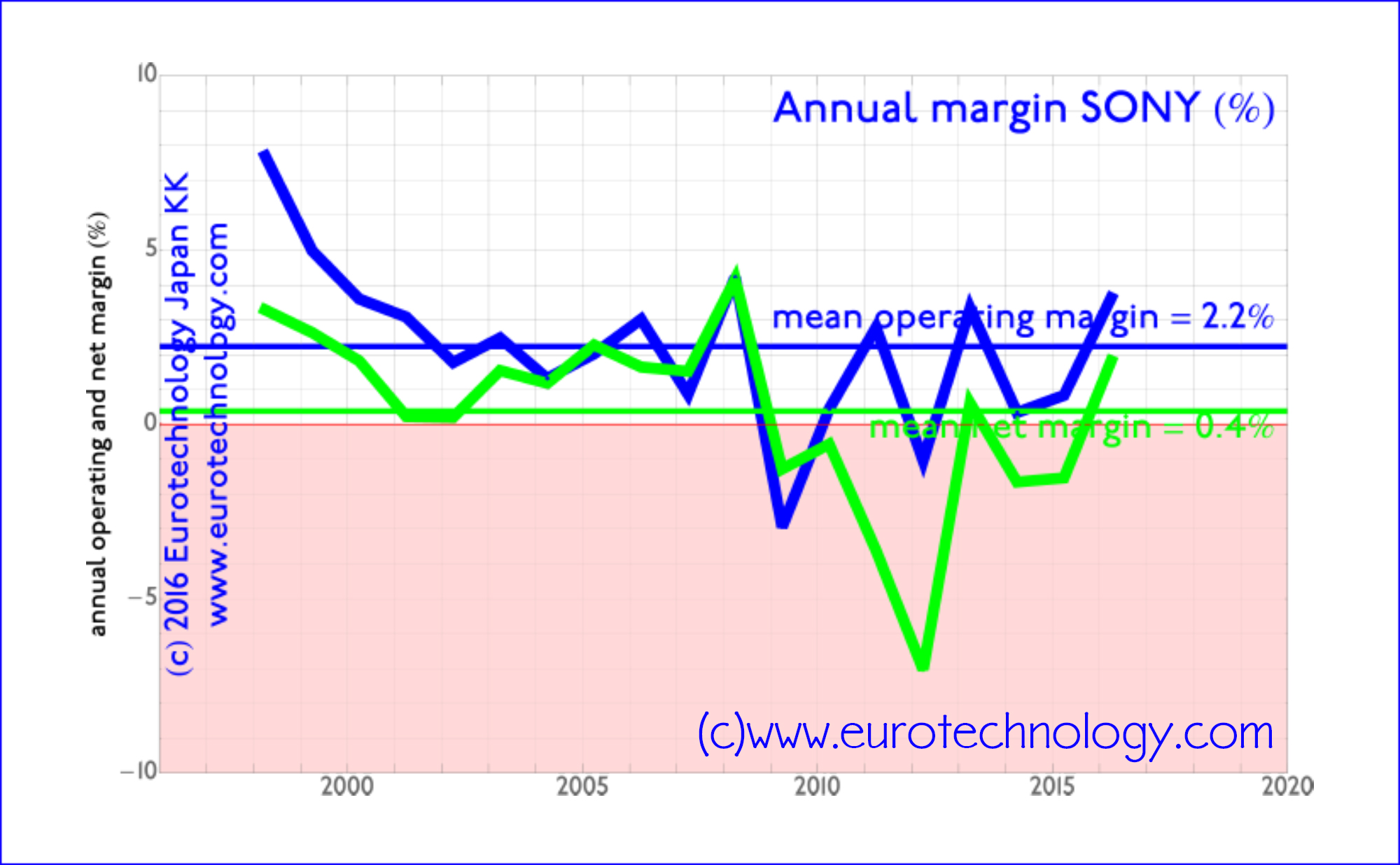

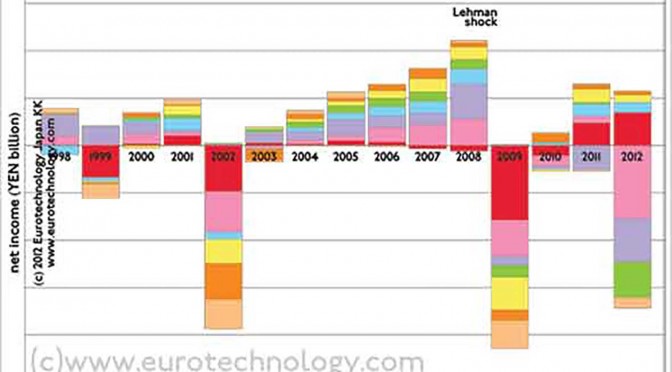

compound annual growth rate (CAGR) = 1.0% over the last 18 years

Essentially, over the last 18 years (FY ending March 31, 1998 – FY ending March 31, 2016), SONY’s revenues=sales have been stable, growing on average 1% per year.

SONY’s revenues/sales grow at an average compound annual growth rate (CAGR) of 1.0% over the 18 years from FY1998-FY2016

net income/profit margin = 0.4% over the last 18 years

Back in the days of Trinitron vacuum tube TVs and mechanical Walkman tape recorders, SONY’s products could command relatively high profit margins, the falling edge can be seen in the Figure below: gross profit margins were as high as 8% back in 1998, and net profit margins as high as 3% of sales. However, averaged over the last 18 years, net profit margins average about 0.4%.

SONY’s average net income/profit margin over the last 18 years has been very close to zero.

SONY’s subsidiary “SONY Financial Holdings Inc” (60% owned by SONY) is by far the most profitable division of SONY

SONY publishes detailed reports of operating profits for its different divisions, showing that by far the most profitable division are Financial Services, which are not an integral part of the SONY Corporation (ソニー株式会社), but a partly (60%) owned and separately managed subsidiary SONY Financial Holdings Inc (ソニーフィナンシャルホールディングス株式会社).

In the latest financial report for the Financial Year ending March 31, 2016, SONY Finance has twice as much income/profit as the next most profitable divisions – SONY’s Financial Services (mainly offering credit card and banking services inside Japan) are and have been by far the most profitable division of SONY for many years.

SONY Financial Holdings Inc (ソニーフィナンシャルホールディングス株式会社) is a subsidiary of SONY, and is independently listed on the Tokyo Stock Exchange [TSE Code 8729], was founded on April 1, 2004, and IPO was on Oct 11, 2007. SONY owns 60% of SONY Financial Holdings Inc’s shares.

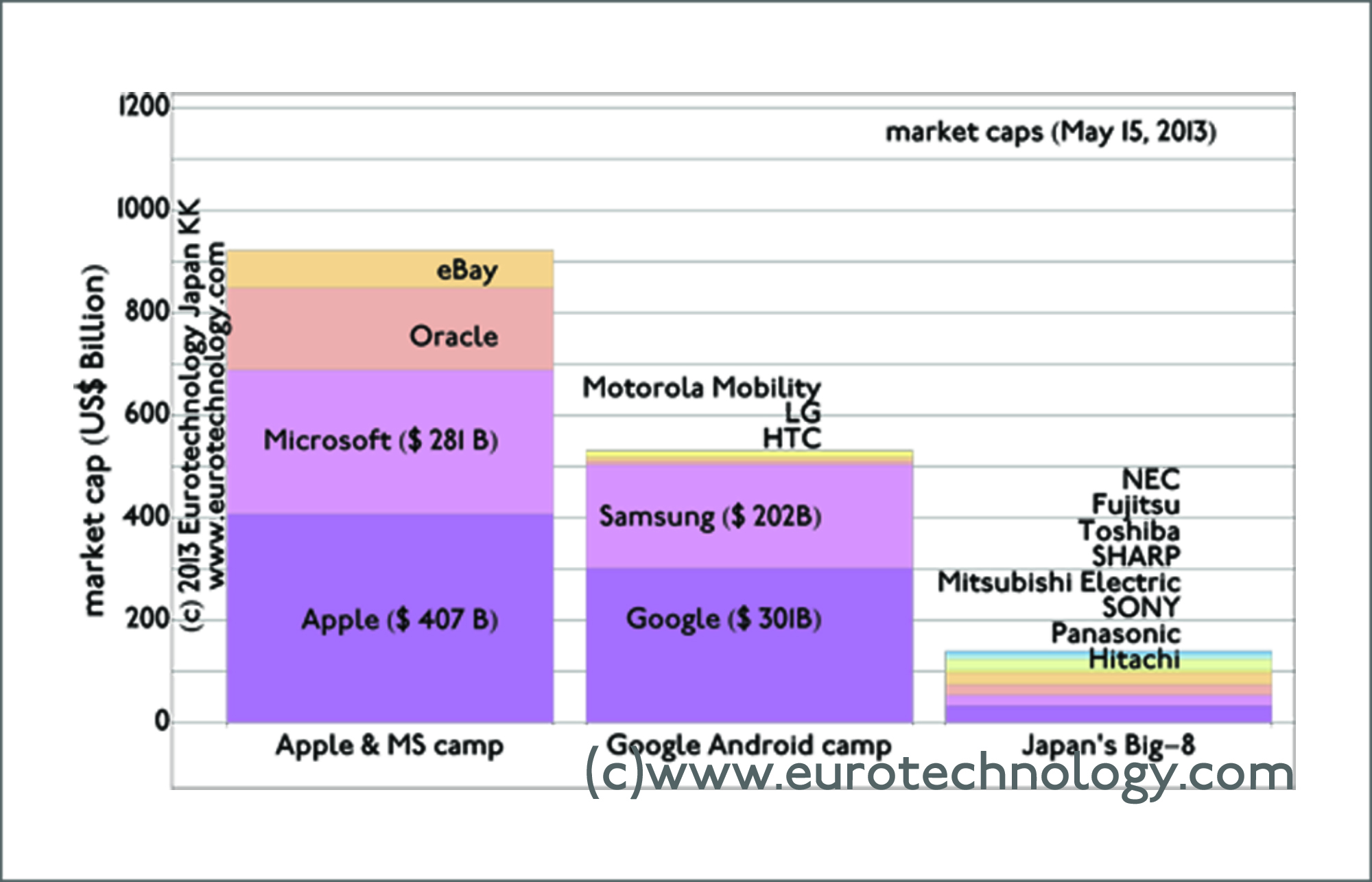

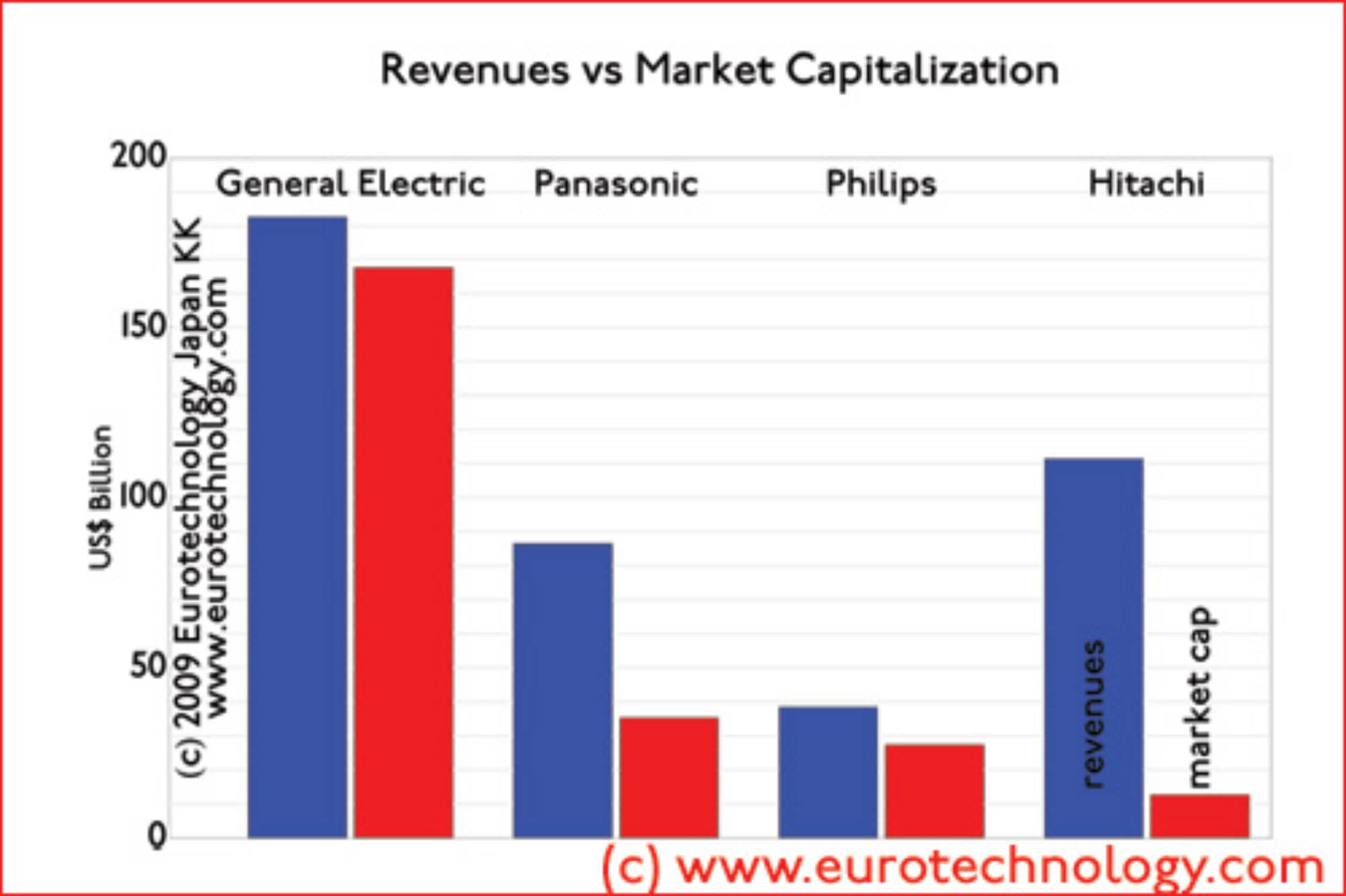

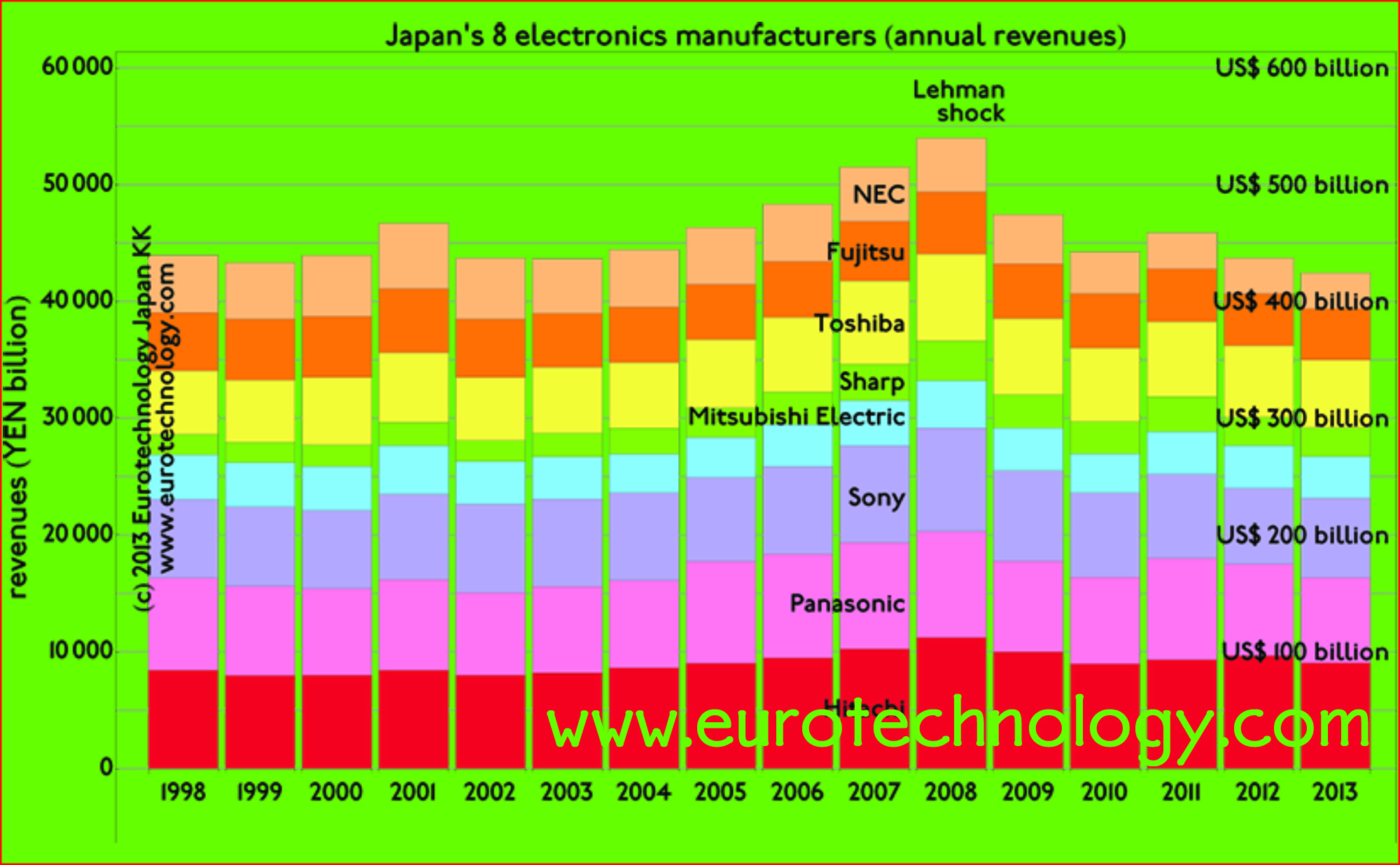

the future of Japan’s US$ 600 billion electronics sector, which dominated world electronics in the 1980s but failed to keep up with the evolution and growth of global electronics.

To survive Japan’s old established electronics conglomerates have two choices:

focus on a small number of key products (remember Apple CEO Tim Cook showing that all of Apple’s products fit on one small table)

actively managed portfolio model

however, for Japan’s economy to prosper, Japan needs many more young fresh new companies in addition to the old established conglomerates.

Interviews for BBC-TV and French Les Echos

Last week I was interviewed both live on BBC-TV and also by the French paper Les Echos about SHARP’s future:

In summary, I said that its not just about SHARP’s current predicament, but its about corporate governance reform in Japan, about reinventing Japan’s electronics sector, and that its more likely at this stage that Japan’s Innovation Network Corporation (INCJ) will take control SHARP, since INCJ is not just concerned with SHARP but with the bigger picture of restructuring Japan’s electronics sector.

INCJ has concepts for combining SHARP’s display division with Japan Display, and has plans for SHARP’s electronics components divisions, and for the white goods division, and other divisions.

SHARP governance: How and why did SHARP get into this very difficult situation?

Essentially SHARP assumed that the world market for TVs and PC displays will continue to demand larger and larger and more expensive display sizes, and thus took bank loans to build a very large liquid crystal display factory in Sakai-shi, south of Osaka.

In addition, SHARP, has a huge portfolio of many different products ranging from office copying machines and printers and scanners, mobile phones, high-tech toilets, liquid crystal displays, solar panels, and hundreds of other products. SHARP keeps adding new product ranges constantly expanding its portfolio of businesses, and rarely sells loss making divisions.

Effective and strong independent, outside Directors on the Board might have asked questions during the decision making leading to the building of the Sakai factory. They might have asked for a Plan B, in case the global display market takes a turn away from larger and larger and more expensive displays, or if the competition heats up and prices start decreasing, they might have asked about SHARP’s competitive strengths, they might have also questioned the wisdom to finance an expensive factory via short-term bank loans as opposed to issuing shares to spread the risks to investors.

Its not just outside Directors, shareholders could have also asked such questions.

SHARP has about YEN 678 billion (US$ 5.6 billion) debt, most is short-term debt, and in a few weeks, in March 2016, SHARP needs to repay about YEN 510 billion (US$ 4.2 billion), and needs to find this amount outside.

SHARP is a Japanese electronics company, founded in 1912 by Tokuji Hayakawa in Tokyo as a metal workshop making belt buckles “Tokubijo”, and today one of the major suppliers of liquid crystal displays for Apple’s iPhones, iPads and Macs.

SHARP today has about 44,000 employees, many factories across the globe, sales peaked around YEN 3000 billion (US$ 30 billion) in 2008, and show a steady downward trend since 2008.

Revenues (profits) peaked in 2008, and have fallen into the red since.

SHARP’s revenues (sales) peaked in 2008 around YEN 3000 billion (US$ 30 billion), and show a downward trend ever sinceAveraged over the last 14 years, SHARP shows average annual net losses of around YEN 38 billion per year (US$ 380 million per year)

What future for SHARP? Focus vs portfolio company

SHARP (or rather, its creditors, the two “main banks” Mizuho and Mitsubishi-Tokyo-Bank, and others controlling the fate of today’s SHARP) needs to decide whether it focuses on a group of core products, in which case it needs to be No. 1 or No. 2 globally for these products. Successful examples are Japan’s electronic component companies.

Or on the other hand, SHARP could be a portfolio company, in which case this portfolio must be actively managed.

What future for Japan’s US$ 600 billion electronics sector?

combined have sales of about US$ 600 Billion, similar to the economic size of The Netherlands, but combined for about 15 years have shown no growth and no profits. They are poster children for the urgent need for corporate governance reform in Japan.

These 8 electronics conglomerates are portfolio companies, and they need to manage these portfolios actively, such as General Electric (GE) or the German chemical industry are doing. Germany’s large chemical and pharmaceutical industries started active and drastic product portfolio management in the 1990s, and are continuing constant and active portfolio optimization via acquisitions, spin-outs, and other M&A actions, and so is GE.

Why “let zombie companies die” is beside the point

Concerning SHARP some media wrote headlines along the lines of “let zombie companies die”. Thats easy to write, however, SHARP is a group with 44,000 employees, many factories, about US$ 30 billion in sales annually.

“Let this zombie die” is not an option, SHARP has 100s of products, and divisions, and the best solution for each of these divisions is different. And that is exactly what the Innovation Network Corporation of Japan seems to be considering in its plans for SHARP.

I think the way forward is not “to let zombies die”, but to develop private equity in Japan

I think the move of Atsushi Saito, one of the key drivers of Japan’s corporate governance reforms, from CEO of Tokyo Stock Exchange/ Japan Exchange Group, to Chairman of the private equity group KKR is a tremendously important one in this context.

Will there be native Japanese private equity groups with sufficient know-how and ability to take responsibility of restructuring Japan’s electronics sector? Thats maybe the key question.

Why its not really about nationalism

Some media bring a nationalist angle into SHARP’s issues. However, Nissan was rescued by French Renault, UK’s Vodafone acquired Japan Telecom, and there are many other examples, where foreign companies acquire Japanese technology companies.

I don’t think nationalism is an issue here. The key issues is to create and implement valid business models for Japan’s huge existing electronics sector, and more importantly, create a basis for the growth valid new companies – not just reviving old ones.

Economic growth: Almost everyone agrees that economic growth is preferred over stagnation and decline. Fiscal policy and printing money unfortunately can’t deliver growth.

Governments best help economic growth by reducing friction, and by getting out of the way of entrepreneurs building, turning-round, and refocusing companies.

Some required action is counter to intuition: for example, in many cases reducing tax rates increases Government’s tax income, a fact known for many years. Effective education and research are key to create, understand and apply such non-obvious knowledge.

Companies need efficient leadership, leadership needs feedback, wise and diverse oversight by Boards of Directors, who ring alarm bells long before a company hits the rocks, or fades into irrelevance. Corporate governance reform may be the most important component of “Abenomics”. Read a Board Director’s view on Japan’s corporate governance reforms:

Japan’s electrical conglomerates are some of the poster children motivating Japan’s corporate governance reforms. In an interview about Toshiba’s future on BBC-TV a few days ago, I explained that Japan’s electrical conglomerates showed no growth and no profits for about 20 years, and the refocusing Toshiba has announced now should have been done much much earlier, 10-20 years ago (“Speed is like fresh food“). Refocusing Japan’s established corporate giants will release resources for start-ups, spin-outs and growth companies.

Japan can be very good at restructuring and turn-rounds, e.g. see

Independent 3rd party committee chaired by former Chief Prosecutor of Tokyo High Court

On 12 June, 2015, Toshiba announced corrections to income reports, and at the same time engaged an independent 3rd party investigation committee headed by former Chief Prosecutor at the Tokyo High Court, Mr Ueda, to investigate. This independent 3rd party committee submitted their report yesterday, and held a Press Conference this evening.

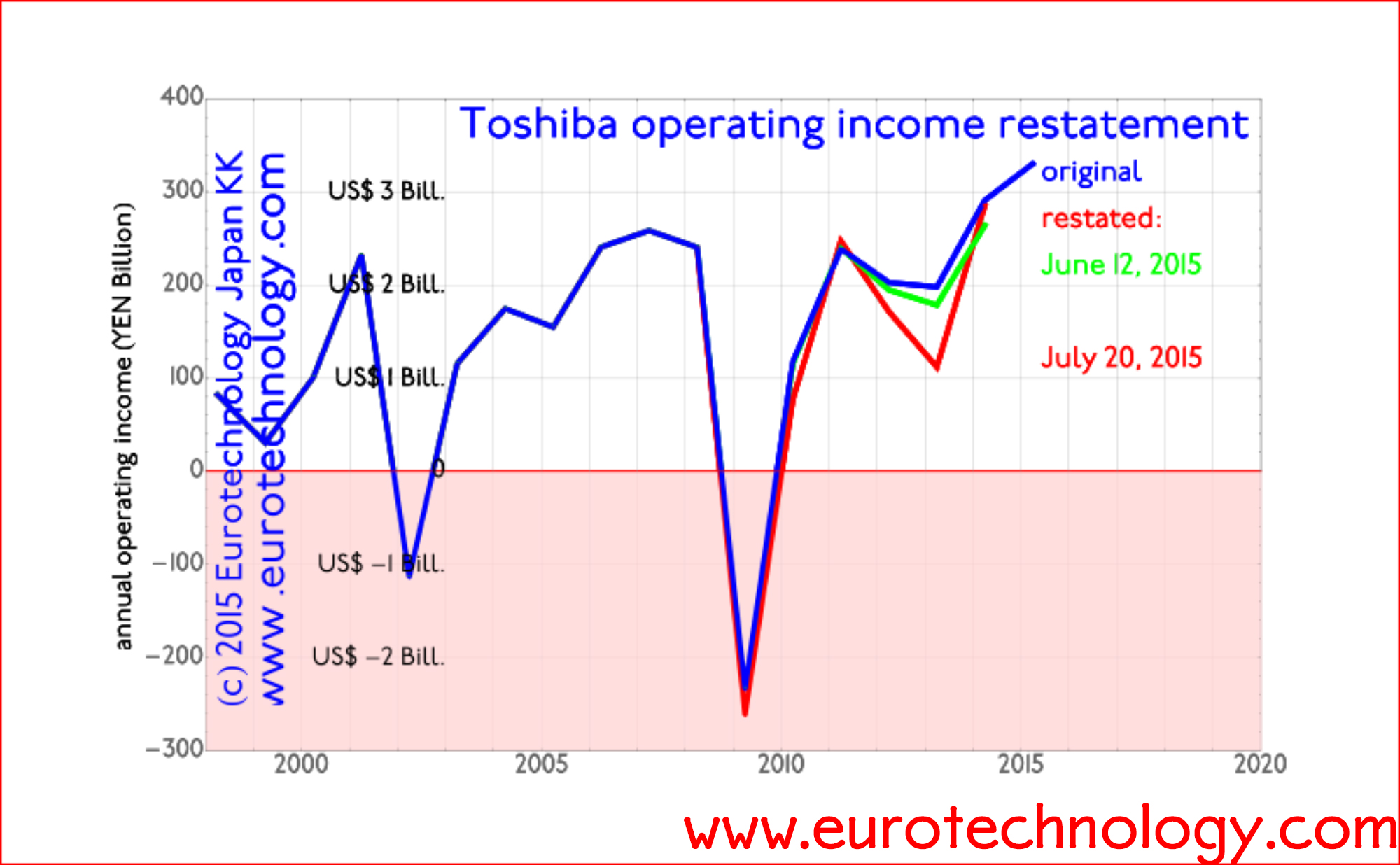

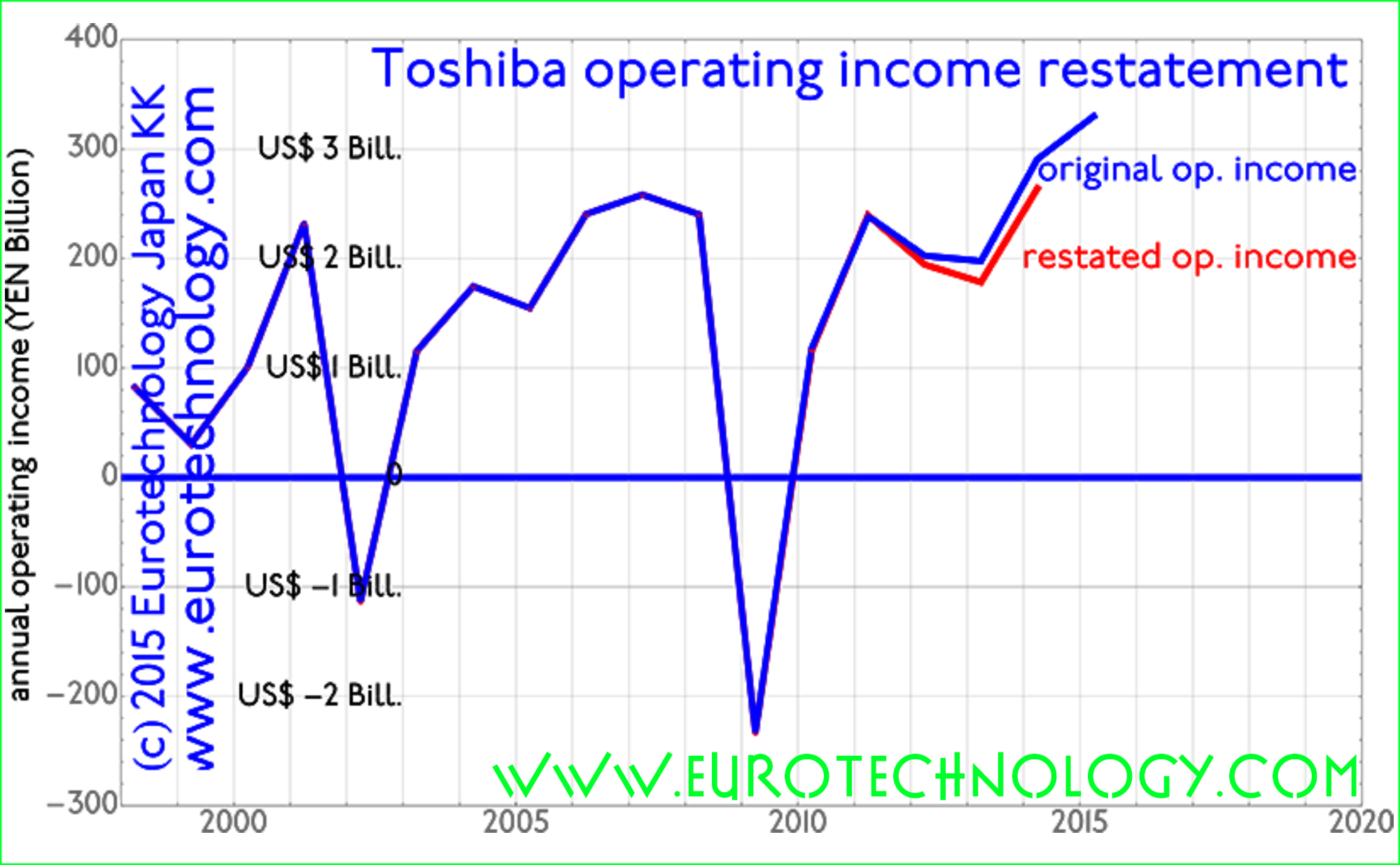

Lets look at the announced Toshiba financial data in detail. The figure below shows:

corrections announced by an internal committee on June 12, 2015 (green curve),

corrections announced by the independent 3rd party committee on July 20, 2015 (red curve).

The combined amount of downward corrections determined by the independent 3rd party committee is YEN 151.8 billion (US$ 1.22 billion) in total.

Lets put this amount into context:

annual sales: approx. YEN 6000 billion (US$ 60 billion)

annual operating income (average over last 17 years): YEN 148 billion (US$ 1.5 billion)

annual net income (average over last 17 years): YEN 19 billion (US$ 190 million)

Therefore the downward correction summed over the years corresponds to:

approx. 2.5% of average annual sales

approx. 103% of average annual operating profits, ie more than a full year of average operating profits

approx. 8 years of net profits

Toshiba – typical for Japan’s large electronics corporations – operates with razor-thin profit margins: Toshiba’s net profit margin averaged over the last 17 years is 0.25%.

Therefore, the downward correction corresponds to 8 years of average net income/profits.

Blue curve shows Toshiba’s initially reported operating income.

Green curve shows corrections determined by an internal examination, announced on June 12, 2015. Corrections amount to approx. YEN 50 billion (= approx. US$ 0.5 billion).

Red curve shows corrections determined by the independent 3rd party commission, chaired by former Tokyo High Court Chief Prosecutor Ueda and announced on July 20, 2015. Corrections amount to YEN 151.8 billion (= approx. US$ 1.22 billion)

Toshiba over the last few weeks published a number of announcements, and corrections to these announcements concerning accounting issues. Toshiba also engaged internal and independent external expert commissions to analyze possible accounting discrepancies, these committees have made preliminary announcements.

At a recent Press Conference, the CEO of the Japan Exchange Group (JXP) which includes the Tokyo Stock Exchange, Mr Atsushi Saito, said that “he feels very much ashamed for Toshiba”, and that “he cannot understand how Toshiba can be so lazy about their accounting”.

To understand Toshiba in the context of Japan’s electronics industry, read our report on Japan’s electronics industry sector:

Japan’s top-8 electronics giants – including Toshiba – have essentially stagnated for the last 17 years with negligible growth and negligible profits. Japan’s top 8 electronics groups combined have sales approximately as large as the economy of The Kingdom of the Netherlands. However, the big difference is, that in the 17 years since 1998, the economy of The Netherlands has approximately doubled, while Japan’s top 8 electronics companies have not grown their sales at all over these 17 years. Expressed in Japanese YEN, the combined sales of Japan’s top 8 electronics companies in FY1998 is about the same as in FY2014.

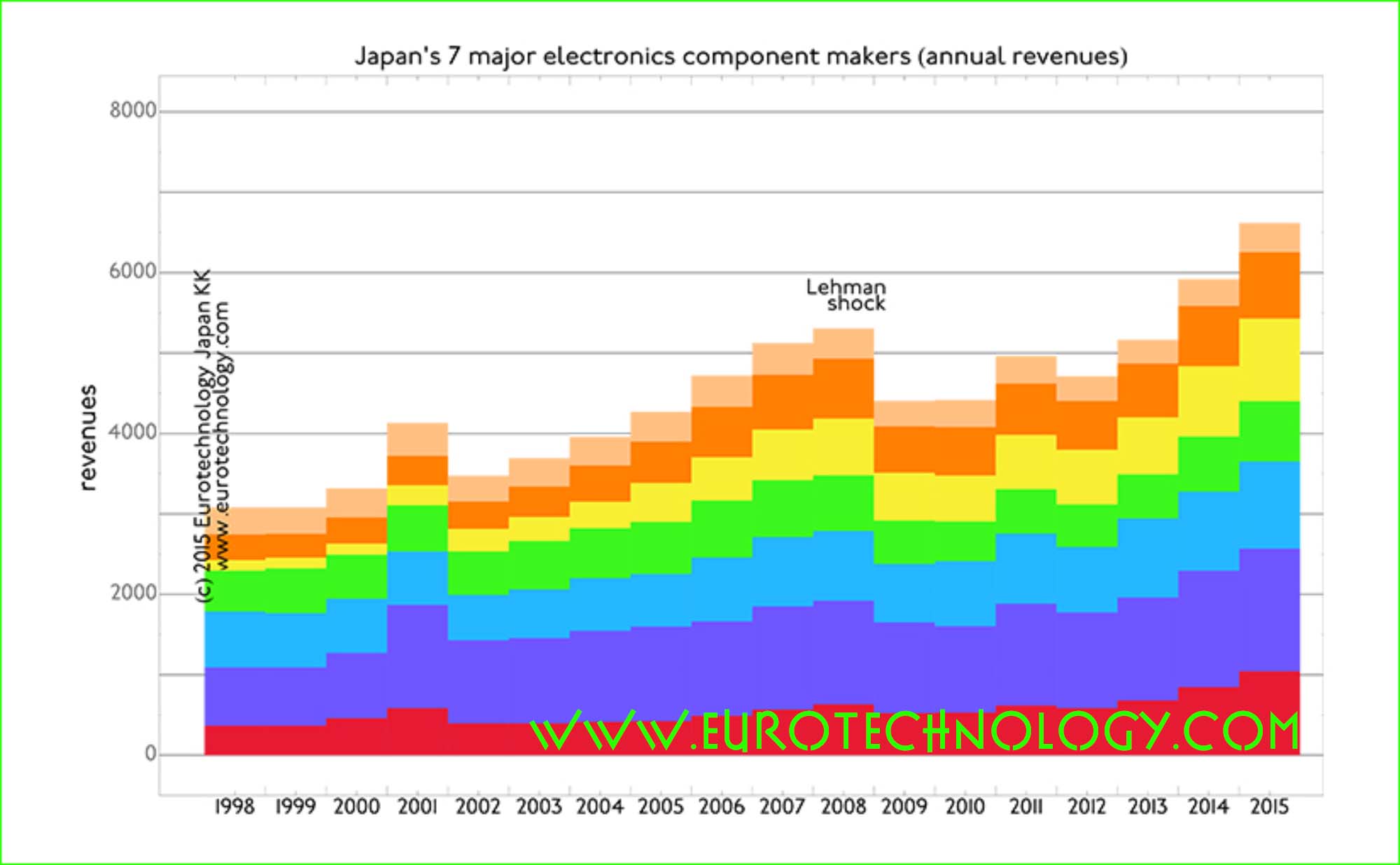

Japan’s electronics parts makers are a very different story: similar to The Netherlands, Japan’s top-7 electronic parts makers have grown to more than twice the size over the 17 years from FY1998 to FY2014. Some of the Japanese electronics parts makers have growth targets which should allow them to overtake Japan’s current incumbent electronics groups!

The stagnation of sales growth combined with almost zero profits over 17 years of Japan’s top 8 electronics groups, of which Toshiba is one, certainly puts much pressure on Japan’s electronics groups to improve performance. This pressure might be the background of accounting issues.

Lets look at the actual Toshiba financial data in detail

The figure below shows Toshiba’s previously reported operating income/profits (blue curve), and the recently announced preliminary corrections (red curve). The combined amount of downward corrections is about YEN 50 billion (US$ 0.5 billion) in total.

annual sales: approx. YEN 6000 billion (US$ 60 billion)

annual operating income (average over last 17 years): YEN 148 billion (US$ 1.5 billion)

annual net income (average over last 17 years): YEN 19 billion (US$ 190 million)

Therefore the downward correction corresponds to:

approx. 0.8% of average annual sales

approx. 33% of average annual operating profits

approx. 2 1/2 years (31.5 months) of net profits

Toshiba – typical for Japan’s large electronics corporations – operates with razor-thin profit margins: Toshiba’s net profit margin averaged over the last 17 years is 0.25%.

Therefore, the downward correction corresponds to 31.5 months of average net income/profits.

Toshiba accounting corrections amount to approx. 33% of average annual operating income

Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

Only with freedom and democracy, the values of open society and professionalism can the investment chain function effectively

Japan Exchange Group CEO Atsushi Saito: proud of Corporate Governance achievements, but ashamed of Toshiba

The iconic leader of the Tokyo Stock Exchange since 2007, now Group CEO of the Japan Exchange Group gave a Press Conference at the Foreign Correspondents Club of Japan on June 12, 2015, a few days before his retirement, to give an overview of his achievements and to review the status of Japan’s financial markets today.

Atsushi Saito expresses his satisfaction and pride and surprise about the big improvements in corporate governance and the mind change happening in Japan now.

Atsushi Saito has worked as equity analyst in the USA, experienced the US pension fund debate, and when he was pushing for reform of corporate governance in Japan around 1990 was ignored or even criticized. He is surprised to see that these changes he has been keeping pushing for since 1990 are actually implemented now.

Atsushi Saito directly expressed his shame about the accounting problems recently revealed at Toshiba, and contracts Hitachi, which has independent outsiders, women and non-Japanese foreigners on the Board of Directors, with Toshiba which has not. Atsushi Saito directly said: “I am very puzzled why Toshiba is so lazy to check their accounting”.

Atsushi Saito – leading the Tokyo Stock Exchange since 2007

Leading the Tokyo Stock Exchange since 2007, Atsushi Saito aspired to create an attractive investment destination in Tokyo for investors from all over the world with the following achievements:

modernized the trading systems

developed a self regulatory body

merge with Osaka to create Japan exchange group

Reform corporate governance to improve capital efficiency and corporate value of Japanese companies

The most imperative challenge has been left untouched for far too long: reform of corporate governance in Japan to improve capital efficiency and corporate value of Japanese companies.

Recently we introduced the Corporate Governance Code and we see a shift of mindset in Japanese companies.

Structural impediments remain remain in Japan’s financial market

Structural impediments remain remain in Japan’s financial markets, indirect finance from Banks remain a significant force in corporate finance.

Japanese investment bankers continue to fall way behind European and US rivals.

The post financial crisis regime under Basel 3 puts breaks on excessive leverage.

When global economy returns to high growth, we are not able to rely solely on money centered banks – banks will not be able to provide enough capital satisfy demands in a growing world economy.

Foresee demands for international organizations WorldBank, ADB and new AIIB and private equity funds.

With FinTec, we expect unbundling across separate financial service lines

With fintec, combining financial services and technology, we expect increasing unbundling across separate service lines for banking services, between settlement, wire transfers, loans and other services.

We will see more financial services.

Over dependence on main banks, risk aversion, lack of sense of duty by corporate managers led to the death of Japanese equity as an asset class

In Japan, as a consequence of dependence on indirect finance by money centric main banks, deep involvement of the main banks in corporate management, Japanese companies grew increasingly risk averse shied away from dynamic investment, and ultimately damaged corporate value.

There was a demise of the sense of duty by corporate managers use equity capital efficiently, and as a consequence of these factors, we saw a global divestment from Japanese stocks, eventually leading to the death of Japanese equity as an asset class.

Pushing since 1990 for reform of corporate governance in Japan, Atsushi Saito was not only ignored but even criticized

Atsushi Saito working as an equity analyst in the USA, followed the US pension debate, and started to push for reform of corporate governance in Japan around 1990, he was not only ignored but criticized.

Japan’s recent miraculous turn on corporate governance took Atsushi Saito by complete surprise

Today Japan addresses corporate governance, there is a miraculous turn of mindsets and regulatory framework. We saw:

amendment of companies act

corporate gov code

stewardship code

That these changes could happen came as a complete surprise.

Atsushi Saito hopes that this momentum can be maintained, and fiduciary duties of pension fund managers towards beneficiaries will be strengthened to nurture greater professionalism among Japanese institutional investors, similar to The Employee Retirement Income Security Act of 1974, or ERISA act in the USA.

Only with freedom and democracy + values of open society + professionalism can the investment chain function effectively

Only with freedom and democracy, the values of open society and professionalism can investment chain function effectively. This pattern is what defines truly advanced economy

The recent transformation has brought Japan back into the focus of professional investors globally and a new dawn beckons for Japan.

All stakeholders must remain focused to follow through these early signs of change to ensure that Japan welcomes a brighter future.

Questions and answers

Q: Japan not joining the Asian Infrastructure Investment Bank (AIIB) will deprive Japan of opportunities?

A: The Japanese Government did not say that it will not join the AIIB, but today there is no clear set of rules for the AIIB, the governance structure is unclear. To use tax payers money our government needs to be prudent before they make a decision on investment. There are about 20 international banks and similar organizations, 19 of them have clear governance rules. All except AIIB have clear governance rules. In case of AIIB China will have about 30% holding. Probably our Government will wait before making a decision, and Atsushi Saito thinks this is reasonable.

Q: Will Tokyo Stock Exchange enter into international alliance?

A: Stock Exchange business is a very nationalistic business – only USA has multiple exchanges. All other states have one single Exchange totally under control, regulations, culture by single states. Theoretically Exchanges between different countries can merge, but none succeeded. We saw no case in the world were Exchanges from different countries merged successfully, all such cooperations failed.

Q: Plans of Toyota to have non-traded convertable shares?

Its up to their shareholders. Legally they did not violate any rule.

Japan does not have any priority on special stocks.

I see a discrepance in the USA: The US aggressively raises the voice for rights of shareholders, and corporate governance elsewhere. At the same time US companies are the largest issuer of special stocks for special owners, e.g. for Google or Facebook, more than 50-60% of voting power is dominated by the founders of these companies. –

I see a discrepancy, its an ironical discrepancy. I am talking to the leaders of US : US is very nosy about our corporate goverance, protection of shareholders, but how do they protect shareholders of Google or Facebook?

Q: What is your advice for Japanese economy to regain vitality and energy, for Japan to become No. 1 in the world?

A: I am very concerned about efficient capital use and corporate governance. When I was securities analyst in USA, I was always asked about financial data of Japanese corporations.

Fuji Film had huge cash on the balance sheet – their competitor, the yellow-color photo company was always diligent with share holders, paid dividends, did share buy-backs. Fuji spent much R&D on pharmaceuticals and diversification. The Yellow color photo company disappeared, and Fuji Film is very healthy. Accumulation of sleeping capital is useless. But efficient use of capital is crucial.

when GM went bankrupt it was discovered that they had great technology, like electrical car projects which had been stopped. GM had stopped these R&D projects, because shareholders had insisted to stop R&D spending, and pay hire dividends, and ultimately went bankrupt.

Toyota had 3 trillion yen cash. This was heavily criticized. Toyota was secretely developing electric cars – now LEXUS electric car is bestseller in USA.

We are concerned to respect shareholders, but shareholders’ short term wishes are not always best for the company.

Even BlackRock wants long-term enterprise development rather than short term cash benefits.

Q: Impact of weak YEN on Stock Exchange

A: Even with weak yen, our trade balance is negative. Yen rate is not pushing export from Japan. Japan is manufacturing outside of Japan. Trade account is negative, capital account is black, currency account is black. Overseas subsidiaries are sending dividends back to Japan at the yen rate of 120. Its smart return in the capital account. Our industry structure has changed, we are not exporting on the back of weak yen, so we are not criticized.

Q: plans after retirement

A: I decided: no job – I will take rest.

Q: Disclosure. Often financial data are exposed early in Nikkei or Japanese press prior to official disclosure.

A: I am often asked about this. I don’t know how the press gets their information, its a free market for the press. As long as they don’t do any insider trading or use this information privately, I don’t see anything wrong with early public disclosure. Its a competitive issue between journalists, we cannot critisize competition among journalists. Very sharp journalists pick up information, we are not the police we cannot stop them. Its a competitive world – even for journalists.

I live far outside from Tokyo, sometimes journalists wait at the door to my home in the suburbs. I think this is an invasion of my privacy, and I don’t tell them information at my home.

Q: Trust in the stock market, low Japanese retail investor participation.

A: Advanced states have 60-70% own domestic investors, not outside foreign investors.

Foreign professional investors have immediately responded to the logic of our corporate governance reforms. Especially US and UK pension managers have immediately responded to the improved efficiency of our markets. Investment professionals in London, New York, Scotland can evaluate the meaning of our regulatory changes.

Japanese professional or private investors could not understand the improvements we have done, they did not react.

Mutual funds however are at record hights and we have 8 million ELISA private pension investments in Japan now. People start to build their own pensions now, so retail investors are coming into the market.

We have a normal quiet market now here in Japan regarding sales of equities.

Q: Tokyo as a financial center?

A: If you ask the same question to London, they will say that with IT all transactions are global. There may be arbitrage on the prices. If you compare Shanghai and NY, the trading volume in Shanghai is higher than in NY, but Shanghai not a global financial center, because they are not liberalized in capital in and outflow, they are No. 1 only in volume.

The definition of Financial Center of the World has changed.

We want to be one of the better places in financial business globally. We want to offer convenient and friendly conditions for financial people to come to Tokyo, as one of the centers for financial business.

Tax plays a very important role to define financial centers. London or NY or Tokyo cannot follow a city state like Singapore. We cannot have the same tax system. Tokyo is far bigger than Singapore.

“Global financial center” is a vague subject for me.

Q: Do current prices accurately reflect corp performance. Foreign investors: speculative short-term gains? will foreign investors pull out when Bank of Japan money flush ends?

A: I don’t think the Japanese market is overheating at all. I think the short term speculators have already left Japan.

Long term investors have long asked for change in Japan, Japan did not listen, but now for the first time Japan is listening and changing, and I am feeling longterm investors are understanding this change. We have long term investors here now in Japan.

Q: is high-frequency trading a danger for Stock Exchange?

A: Flash Crash in US was due to the diversity of exchanges. There are 50-60 markets in US. Flash Crash artificially made, not becaue of speed of trading.

Our rules for pricing system here in Japan, we learnt this since the Edo era, we cannot have flash crash, we limit the price changes, we are cooling the trading. Our system of pricing is different than in the USA.

We have many high-frequeny traders from abroad, and they appreciate our system. US high frequency traders critized us up to 10 years ago, but today they appreciate our pricing system here in Japan, they want to learn our Stock pricing system. This has really been a big change for us.

Q: False accounting at Toshiba. Impact on trust in Japan’s stock market.

A: I feel very ashamed for Toshiba. Toshiba should be the mentor or leader of Japanese industry – not the opposite.

Hitachi is a huge contrast to Toshiba. Hitachi aggressively introduced outside board members, foreign and women board members. Hitachi is investigated by outside and foreign board members.

Toshiba is a total contrast to Hitachi.

I am very puzzled by that – why is Toshiba so lazy to check their accounting.

We hope that auditors and accounting houses are more professional and more serious. They told us that their subsidiaries have different accounting system. They must have intentionally checked that point.

My answer: my feeling is one of shame. We should definitely not repeat this type of thing.

Q: Why do Japanese company accumulate so much cash reserves.

A: One reason is that Japanese labor laws compel Japanese companies to have reserves to pay for restructuring. We introduced changes in corp governance, and many companies now use the cash for M&A to acquire foreign companies, or e.g. Fanuc has increased dividends.

I am optimistic for Japanese companies, because they are using cash more efficiently now.

by Hitachi Chief Executive for Europe and subsequently Hitachi Board Director (2004-2014)

Sir Stephen Gomersall: Princess Chichibu Memorial Lecture to the Japan British Society at Ueno Gakuen, Tokyo, 5 March 2015

Sir Stephen Gomersall: It is a great honour to be giving this lecture this evening.

HIH Princess Chichibu was a charming and broad-minded Patron of this Society and of the many charities to which she devoted her later life. I remember her as a frequent visitor to the Embassy in the 70s, in her dusky blue or apple green kimonos, and occasionally turning up to watch when a British University Rugby team came to Japan.

She also personified the affinity between Japan and the United Kingdom which has its origin in our historical ties and in the nature of our peoples. I felt this throughout my years of living in Japan, and my job as Ambassador was made incomparably easier by the goodwill and respect of many segments of Japanese Government and society towards Britain. But we can’t assume that things will always continue in the same way: images can lag behind reality, and relationships have to be nurtured and given concrete meaning.

Our friendship, differences and challenges

So I’ve chosen to talk about why two countries which are so geographically remote and different from each other have a strong affinity and interest in developing our cooperation; and some of the joint challenges we face, and the contrast in the way our two countries have adapted to the huge changes of the last decades.

Three changes

The biggest change to affect the whole world over this period is what is loosely called globalisation.

Globalisation can be defined as the results, in economic, social and cultural terms, of the mobility of capital, production and people in a free global economy, and of the consequent international division of labour.

This has coincided with a second and more destabilising set of changes in the global structure of power, and the weakening, if you like, of any over-arching system, legal or military, of world governance. This began with the dissolution of the Soviet Union, has continued with the shift from the old G7 to the newer G20, the rise of China in particular, and consequent changes in the position of the United States. New threats of terrorism originating in failed states, and in Japan’s case, the threat from North Korea, are part of this troubling mix.

One can add a third change – the internet, digital and media revolutions – which to the positive have empowered people outside government, helped development in poor countries and created massive consumer convenience; have made political protest easier, as in Egypt and Ukraine; but on the negative have opened new possibilities for cyber warfare and terrorist recruitment, and arguably in the West at least, accentuated the short-termism and sensationalism of contemporary politics.

So I would like to talk, not from an academic standpoint, but from my experience about how I perceive Japan and the UK have been impacted and coped with these in our foreign policy, politics, economy and industry.

The Tea Ceremony as metaphor

But let me first explain how the Art of Tea came into the title.

A very small act of globalisation took place when my friend and fellow Embassy language-student, Robert Cooper and I decided that the study of Tea might be a good route to immersion in a part of Japanese culture and presented ourselves for induction to the Master of the Tea Ceremony at Tokeiji in Kamakura. This is a very famous temple, and its lightly constructed, almost translucent tea house had a special and very tiny door, hardly the size of a dog kennel, through which new initiates had to prostrate themselves on first entry. This had not been built for gaijin, but Robert, who went first in his jeans, an American shirt and dazzling white tennis socks which he thought sufficiently close to tabi, and I crawled through it into the presence of a shocked but stoical Sensei within.

This wizened figure, with a loosely wrapped kimono and upright hair, then intoned to us in courteous but almost impenetrable Japanese some of the history of the Temple, the relationship between Tea and Zen, the necessity of subordination of self, and the rewards which might be ours through striving for perfection in the art of making tea and the service of others. Thereafter we attended almost every week for a year, and slowly learned to be less clumsy in the complex handling of cloths and utensils and better to master the numbing effects of sitting for four hours on our ankles.

After some months, what had been a pain yielded to appreciation of the surroundings, the shadows of leaves on the sunlit walls of the teahouse, and even the beautiful kimono of the younger female class members who usually started the afternoon round. Our teacher was the Sensei’s daughter, a wan lady who kept a steely eye on our sequence of movements, and admonished us and the other students kindly if our foot strayed onto the border of the tatami or our fukusa slipped out of our trouser belts. Thus a whole afternoon could pass in eight rounds of tea, and hardly a word would be said beyond the ritual appreciation of the received cup. By contrast, the mizuba, with its utilitarian sink and stone floor where the cups were washed would be a hive of chatter among the arriving and departing housewives or men students arriving after Saturday work. And when it was all over, we would walk with painful knees down the temple steps to re-join the noise and fumes of the motorcars and the ding dong of the railway crossing by Enkakuji, heading for the bar.

We were constantly encouraged to improve our Art, and always made welcome. We got used to the silence, and began to appreciate that mastering of the physical act of making tea could be a gateway to a sense of harmony, appreciation of nature and the seasons, and communion with a group of people united in performing this simple act of service as beautifully and selflessly as possible.

Being drawn into this world was genuinely precious and even cleansing, and in my mind became a metaphor for many aspects of Japanese life and organisation which are built on a preference for the group, harmony, equality, service, perfection and self-discipline.

But at the end there was always a real world outside.

Now of course I don’t suggest for a moment that traditional Japanese art and culture seeks only to create or perpetuate a perfect illusion, but there is a sense in which the British tradition has been to venture out and throw oneself wide open for better or for worse, while the Japanese is more comfortable with consensus, even silence, its own familiar peer groups and known relationships. Japan makes internal pacts and compromises, which for the purposes of this lecture go under the guise of the Art of Tea.

Foreign Policy and standing in the world.

Britain and Japan have very different philosophical traditions, part of which originates from the 250 years during which Britain went through maritime Empire and industrial revolution, while Japan remained cloistered under the Bakufu. Post-war Britain has remained confident of its place at the international top table, its close relationship with the United States, and its continuing network of international connections. Apart from a moment of hubris in the Suez invasion, it has justified or demonstrated this through its active role in the UN Security council, the retention of its nuclear deterrent and military participation, at a higher level at any rate than our other European allies, in international actions in Iraq and Afghanistan.

Japan too has been at its strongest when it has been open and looking outward. The isolation of the Bakufu was ultimately self-defeating, while Japan surged forward after the importation of Chinese scholarship in the eighth century, and became a successful modern state after the Meiji revolution. The post-war Constitution enabled Japan to re-establish itself internationally, and enjoy a period of high growth through access to foreign technology, domestic capital and world markets. It is distressing sometimes to hear the Constitution described as “anti-Japanese”.

Today’s Japan has established itself as a country with a peaceful foreign policy, an economic power house making an important contribution to international economic cooperation; opinion polls show Japan internationally much admired except in China and Korea. Japan has significant soft power based on its culture.

The baseline for the modern UK-Japan relationship can be set in the eighties and nineties, when Japan was the pre-eminent nation in Asia, and the UK still the leading pro-American voice in the EU. During this time a core UK-Japan agenda was developed, based on the very similar views of what kind of world we wanted to see after the collapse of the Soviet Union.

The elements of this agenda are built around free trade, the rule of law, peaceful conflict resolution and support for the United Nations. The UK and Japan were co-architects of the Kyoto Protocol on Climate Change in 1997. Britain enjoyed support at the UN from Japan on action on Iraq and Libya; the UK supported Japan’s first deployments of self-defence forces to the Gulf and Afghanistan.

This political relationship continued during the Blair-Koizumi period, predicated on strong support for our mutual ally, the United States.

Relations with the United States

The United States is a huge friend and guarantor for both Japan and Europe, but cannot be expected to defend us if we don’t defend ourselves. Noticeably it was the United States which flew sorties in the East China Sea not long ago after a particular Chinese threat to the Senkakus, just as it was the United States which did the same when the Russians recently made menacing noises towards the Baltic States. But with a Congress no longer so clearly internationalist or prepared to step into every security breach and rightly demanding more burden-sharing from its allies, Japan and Europe need to have the capabilities, and relationship with America, to fulfil our side of the bargain.

What I have described is, and should be, the base state of a UK-Japan relationship founded on cooperation between two closely aligned countries. As global number three and number six economies we each have an important voice – if we can use it effectively – and this in turn depends upon our economy, defence, and international friendships and alliances.

But since 2008, a number of clouds have passed across the European and Japanese skies. One is disillusionment with the consequences of the invasion of Iraq and the troubles in the Middle East; another big one the global financial crisis of 2008, which had huge consequences in the EU; and a third the rise, part opportunity, part threat, of China, together with heightened tension in East Asia as a whole. Viewed from Japan, an increased UK/European focus on China came at exactly the point that Japan-China relations began to deteriorate. These are among the factors which have caused both sides to become more preoccupied with issues close to home. Perhaps changes in the Japanese Government didn’t help either, but they are reasons why both sides may have questioned whether the relationship was really as important to the other as we traditionally maintained. The outstanding UK response, public and private, to the Great Tohoku Earthquake was a big affirmative, but even so these questions remain in the air.

Two nations in retreat?

Compared with our past, some people will ask whether in fact we are now looking at two nations in retreat.

The reaction in Britain to UK deployments to Iraq and Afghanistan, at the popular level, has been quite deep. Although both missions were partially achieved and people were very proud of our troops, these nonetheless exposed the difficulty for our relatively lightly armed forces in dealing with unorthodox warfare. Increasing resources had to be committed with diminishing political returns. Since the end of the Cold War, successions of defence reviews have eaten away at the numbers of personnel and front-line units in our forces. And our spending – though better than most Europeans, is perilously close to the minimum 2% of GNP level expected by NATO.

A second is the dominance of domestic issues in politics, and sudden concern about the future of Britain as a United Kingdom. We are now facing a general election. The battle-ground is likely to be the economy, where the two large parties – Conservative and Labour – in reality have not a lot dividing them on economic philosophy, and not a lot of room in any case for manoeuvre in trying to reduce the national deficit, but still appeal to the electorate daily in terms of what benefits they can deliver to their traditional followers – what Labour refers to as “ordinary people”, and the English middle class and better-off voters for the Conservatives. New promises over the health service, welfare provisions, taxation, university tuition and the like burst daily on the airwaves and then fizzle. This is a rather narrow-band form of politics over how to divide resources within the society to the benefit of one group or another, with very little search for consensus on these difficult issues. Since party membership has fallen dramatically, it is not certain how much core loyalty exists to these parties within the electorate. In the meanwhile an anti-European, anti-immigration party has been taking support from both major parties; and the Scottish National Party, after losing the referendum on independence by 55-45%, has bounced back and will certainly press for further separation should it hold influence in Westminster after 7 May.

This is not good news for anyone.

One plausible factor behind this fragmentation of current British politics is that globalisation has created different categories of winners and losers from those familiar in the traditional class divide, and that devolution has actually broken the Westminster system of politics. Regional disparities, particularly between London, the North and Scotland, are now accentuated by rhetorical politics. Another element is that across the country there are groups of people, mainly white, older or unemployed, with lower skills or shrunken pensions who feel threatened by immigration and the cutting back of the welfare state. Concepts of community and identity have become confused. While the Mayor of London can revel in the vigour of London’s “melting pot” society, in other regions the disparity of wealth and opportunity can create an anti-metropolitan, anti-traditional party backlash, resulting in a large increase in disaffected or floating voters.

The third is the UK’s relationship with Europe, and here again there is a parallel with Japan.

The founding purpose of the EU was to achieve peace in Europe after the Second World War through economic integration. It achieved this spectacularly well between France and Germany, together with rising living standards for the poorer agricultural regions of Europe. The same logic applied in the eighties and nineties, when enlargement was extended to Greece, Spain and Portugal who made the transition from dictatorship to democracies. Mrs Thatcher recognized this and argued not only that the Single Market should be accelerated, but that Europe should act together in international affairs whenever it could achieve more by speaking with a single voice in the world. She vehemently opposed the idea of one government for Europe, but in reality the major countries have never wanted that, and the threat disappeared when the EU was enlarged to 26 countries in 2004. Game set and match to Britain, you would have thought.

However, instead of celebrating the victory of Mrs Thatcher’s vision of Europe as a voluntary Union of sovereign member states, parts of the media and Conservative party have continued to brand the European Union as a conspiracy to take British money, to over-regulate our life, and limit the UK’s national sovereignty, and this drip, drip, drip of anti-EU argument from within his own party led Mr Cameron to open the Pandora’s Box of a referendum on our continuing membership in the next parliament, if he is re-elected.

The current bone of contention with the EU is on the impact of the free movement of people, a basic principle of the Union, which is blamed for excessive immigration, even though the UK economy has desperately needed foreign labour to function. The Government says it needs “reforms” to recommend a yes vote, but is not yet specifying what those reforms need to be.

We know what Japan thinks about this, because it has openly said that Japanese investment in UK is for the EU.

And the Americans have equally said they hope the UK will remain a strong voice in Europe.

Former Prime Minister John Major has argued, most cogently from the Tory side, that if outside the EU, the UK would be “much diminished” internationally, and would still have to conform to EU regulations while having no part in deciding them.

That is why I am not so pessimistic about the eventual result, but it is an issue we could do without when the Middle East is in tatters and the Russians are in the Ukraine.

Japan’s position in Asia

This invites comparisons with Japan’s position in Asia.

The rise of China gives China a weight very like that of Germany within the EU, in terms of regional balance, but unlike the EU, there is no regional framework to moderate tensions between Japan, China and Korea or build a collective Asian Economic Community.

A recent Gaimusho briefing I attended on Japan’s security environment gave great detail on the number of China’s incursions around the Senkaku Islands and unilateral moves in the South China Sea; but was designed to show Japan as the sinned-against party, and Japan’s self-restraint, with no discussion of possibilities for improving relations.

Maintaining balance with China requires patience and steel. Economically Japan cannot re-surpass China, nor can it take the support of South East Asian countries for granted should it come to a stand-off.

Given the speed of increase in China’s defence spending, a posture of increased preparedness on Japan’s part, and ability to cooperate more with allies, is certainly justified.

Even without constitutional change, Japan’s defence doctrine is evolving fast with regard to collective self-defence and military exports, though not the percentage of defence spending in the budget. The UK would I’m sure support Japan’s becoming a “normal” military power, but the manner in which it is done will have a considerable effect on the acceptance of regional countries and allies alike. If based upon deterrence and proportionate response to potential threats, it will be well understood. However Japan does suffer in the view of its allies whenever things are said and done politically which look like poking the adversary in the eye.

The counterpart of deterrence has to be engagement, and building structures for the long term which will moderate trilateral relations for the better. The economic interdependence between Japan and China is already such that both countries fortunately have a strong interest in keeping tensions within bounds, and this can be further built on. A Kohl/Mitterrand moment, when the two leaders held hands in a French war cemetery, looks a long way off in Asia, but Mr Abe is a strong leader and, though I know it is a much dismissed view here, there are useful lessons to be learned from the political achievements of the European Union. Benefits must also come from encouraging young people to travel between Japan, China and Korea.

Though I’ve discussed China, I haven’t found much so far to say about TEA!

The concern most frequently voiced among Japanese friends is lack of interest of young people in foreign study or travel, and the very poor level of attainment in languages among Japanese businessmen, politicians and academics, leading to Japan being discounted in international gatherings, and leaving the floor open to competitors, China particularly, to exploit.

We are here in a university with high standards in international communication, so I won’t stir that particular pot, but revert to the issue later in the context of business.

To summarize the story so far, I do think voters respond positively to politicians who have a long-term strategy for strengthening their nation and can articulate to their people where they want their country to stand in the world and what needs to be done.

Mrs Thatcher’s appeal to many beyond her own party was that she was prepared to confront the reasons for the UK’s economic decline and do something about it. And two very important points underlying her policies were pretty immutable truths of international affairs – the first being that a nation’s influence is in direct proportion to the strength of its economy; and the second, that in a world where threats can come from unexpected quarters, nations need to secure their own defences, through adequate armed forces and strong alliances.

Though we are geographically distant, it is very important that the UK recognize its interest in East Asian Security, and Japan continue to play its part in Europe. There would be no better way of symbolizing that than the early conclusion of the EU-Japan Free Trade Agreement.

Economy and Industry

Let us turn now to the economy. Here we see rather greater contrast.

Benefits of Globalisation for Britain

Britain has benefited hugely from globalisation. As I see it, Japan has been slower to adapt but has strength in depth.

As you know, Britain went through a severe economic decline in the 1950s to 70s when our largely nationalised heavy industries, and many of the people who worked in them, were cut back as a result of global competition, from Japan among others. The Thatcher government finally brought labour market reforms, privatisation of public assets, and encouragement of foreign investment into manufacturing. The liberalisation of financial markets established London as a global centre for financial and other services. Manufacturing has declined in volume, but improved in quality, and the UK remains a world centre for research and innovation in universities.

This structure continues to form the backbone of the UK economy, with the state sector – government, education, health and public services, accounting for 43 percent of GDP. The relative flexibility of our economy, and the ability of the pound to float against other currencies, account for our outperformance of other Eurozone economies in the last two years, though that is not to say that there are not considerable weaknesses as well, as I will come to.

I remember being chided by Japanese commentators for the “Wimbledonisation” of the UK economy – acting as host to foreign players but having very few national champions. And I remember a huge joy when for a while Japanese Sumo was dominated by Mongolian and Baltic wrestlers. However, whether you call it Wimbledonisation or having an open economy, it accords with British traditions and basically works for the UK.

It has continued apace, with the government welcoming Chinese investment in UK infrastructure, Tata buying our steel and automotive companies, Japan investing in UK energy, etc. It is open house.

And of course we have the advantage of English being the international language of business, the south side of Hyde Park being the recreational space for thousands of French families.

From an economic standpoint, our two major challenges are still the public finances and education/skills.

Japan and globalisation

Japan by contrast has been harder hit, arguably because it has protected its domestic market more.

In the manufacturing sector, Japan has huge assets at home – very high levels of engineering, a disciplined workforce, and is a global leader in quality. But it now has if anything too much hard productive capacity relative to the size of the domestic market. Twenty five years ago, protectionism in the US or Europe was a reason for Japanese companies to transfer production overseas, but now the reason is demographic contraction and the extreme difficulty of making substantial margins at home. In our own company, though everything has been done to avoid loss of domestic jobs, the ratio of workers in Japan to locals overseas within our workforce has fallen from two-thirds to nearer half.

Twenty years ago, it was already evident that Japanese companies trading abroad, and therefore exposed to global competition, could be extremely flexible even in the face of the yen moving from 100 to 70 to the dollar. On the other hand, domestic sectors – retail, banking, insurance companies – with only other Japanese firms as competition, were very slow to consolidate and restructure, and as a result suffered in some cases slow deaths by overcrowding and indebtedness.

In high tech one found not Wimbledon but Galapagos – whereby mobile phone companies for example took their domestic market to very high levels of specification, making it difficult for new entrants from outside to come in, but sacrificed the opportunity to determine the global standards being set in the international market, ceding the leadership in the process to the US and Korea.

Even now, Japan’s percentage of Foreign Direct Investment to GNP is the lowest for any OECD country, and with most markets matured and fully supplied by domestic incumbents, it is hard to see that changing.

The common thread behind many of these stratagems has been to avoid disruption to the Japanese market through having foreign competition within, and to maintain employment – in other words the policies of the TEA HOUSE. And yet these have not staunched the hollowing out and increasing disparity of wealth in rural Japan compared with the metropolis. What is far more likely to stimulate new domestic growth is more competition from new players, market reform to liberate new forms of industry – for example in high-volume agriculture – and population growth.

If the aim is to increase domestic demand, “where is the third arrow?” is still the key question. So far, it seems, quantitative easing has produced a short term benefit for large corporations in stock values and profits from overseas earnings, but these have not yet trickled through to wages and domestic consumption – and could be another example of a policy which produces contrary results by shrinking from reform.

Immigration is a hot topic

Given the UK’s shortage of skills, and Japan’s shortage of young people, it’s not surprising that Immigration is a hot potato for both countries.

Britain has always had open doors to immigration for economic reasons. During our post-war recovery, we accepted migrants from our former colonies to do low-grade jobs.

This was brought home to me when I acted as a part-time census officer in 1971, and discovered that a single road of terraced houses in inner London was neatly segregated between old white widows, with their cats and milk-bottles, the Mediterranean Italian and Greek migrants, never there to accept the census form because they were presumably out partying, Indian and Pakistani families fearful of the authorities and barely prepared to respond from behind a chained door, the old Caribbeans from Jamaica and Trinidad, unable to write the form themselves, but proud and welcoming to their tidy homes, and other black working class households, only scraping it together economically, and often working all hours.

Since then the Asian communities have spread to many Midlands and Northern cities and become middle class. They have high aspirations for the education of their children, who look like Asians but behave like their British peers. These communities are now becoming represented in local government, teaching, broadcasting, Parliament and even the Cabinet. They are increasingly the backbone of our medical services.

Because of the turmoil in the Middle East, there is a portion within the Muslim communities, which is prone to radicalisation by fundamentalist Imams or jihadi social media – and a constant worry to our security services.

Since the 1980s the Government has severely curtailed further immigration from non-EU countries, so that these communities are now to all intents and purposes indigenous and there is no way or intention to repatriate them.

A second source of immigration has been the European Union. Freedom of movement is a basic principle, under which many Brits have gone to work or retire in Europe, and many Europeans, primarily from Poland and Eastern Europe, have come to work in the UK. They come under a legal right, but in significant numbers. Net migration into the UK was 298,000 last year.

A third group are refugees from conflicts in Africa and the Middle East – Somalis, Kurds and North Africans, entering illegally from other parts of the EU. This is a humanitarian issue for the EU, with the burden falling much more heavily on France and Italy.

It is the inability to limit the second category of able-bodied and work-hungry immigrants from EU countries which arouses the most controversy, especially in the run-up to an election. Go into any British hotel or restaurant, and you will find Spanish or East European receptionists, waiters and cleaners. Look for a builder fix your house, and a Pole will probably be more reliable.

This shows a key weakness of the British economy, which is a shortage of skills, and also gives rise to complaints among the unskilled population that “foreigners are taking their jobs”. The right-wing UKIP party then lay this all at the door of the EU, claim that migrants are defrauding the social security system, and that our country, saved by our Forefathers from German invasion during the Blitz etc., is is now being taken away from us. Fortunately this is a war of words, rather than on the street, but still a powerful message to some older voters.

In reality EU residents in the UK, of whom there are 1.4 million, pay much more in taxes on their income than they consume in social benefits. And it is inconceivable that the health service could function, or all the public construction projects planned in the next decade be completed, without a heavy involvement of foreign labour. The government is seeking to provide more welfare to work and apprenticeship opportunities to young British people. But the danger is in the effect this could have in the short term if we are faced with an EU referendum.

Japan’s situation is completely different, but still has to confront the reality that Japan will inevitably decline unless it can find an answer to its ageing and shrinking population. It is hard to envisage permanent immigration from Asia to Japan of the sort Britain accepted two generations ago, even though the British example on assimilation is quite encouraging. It is equally implausible that artificial intelligence – robots that substitute for human workers – will be able to build roads, sewers, or power stations in the future. Emotion will have to give way to pragmatism. And more work permits for qualified foreign workers will have to be introduced to support industries like construction and transport and increased foreign tourism. When this happens on a significant scale, international marriages are bound to occur, and issues of nationality of husbands and children arise.

I came across such pragmatism ten years ago in Akita when a number of EU Ambassadors were invited by the Governor to give a seminar on attracting foreign investment into the Prefecture. In the evening he offered a splendid reception with three entertainments; first the local lads demonstrating the Kanto-matsuri with lanterns on poles; second a Japanese lady of advanced years performing an elegant geisha dance, and third a cacophonous bunch of Filipina wives of local farmers performing a bamboo dance.

So this topic is a slight deviation from the Anglo-Japanese theme but is critical to the future of both countries, and one that touches companies like mine who need to become more globalised.

Globalisation poses tough challenges for Japanese companies, but is the only way forward.

Now let me turn to the experience of my own company.

Hitachi, with its characters for the “rising sun” and its resonant creed of “Harmony, Sincerity and Pioneering Spirit” has often been taken as a proxy for Japan itself, and its production did indeed exceed 1% of Japanese GNP thirty years ago.

Today it is very good example of a company having to make a profound transition in order to grow within the global economy.

Hitachi started out as late as 1910 as a motor-winding outfit for the mining industry in Tohoku, but quickly advanced into power generation, electrical control and traction equipment. These elite divisions were the breadwinners and training grounds for generations of Presidents. The company creed was monozukuri – perfection in manufacturing – and ochibo hiroi – wasting nothing and learning from experience. Hitachi also prided itself on its research capability, clustered in leafy campuses on the Ibaragi hillsides. So large was the company in the area, that when the Tohoku Earthquake hit in 2011, it suffered structural damage to 2000 buildings.

When I joined I was impressed by the Hitachi’s serious ethos, and by the dedication to quality of product. I am a proud employee and would always risk my shirt on the company’s ability to deliver a product. I did however notice that the grand men who ran the company back then seemed very out of touch with the international world, that the organisation was very hierarchical, that a company of 380,000 people worldwide behaved as if it were a universe in itself, and for all its technological excellence, it produced rather modest profits.

This great company was not just a tea pot, it was a TEA PLANTATION! I say this to emphasize how far things have come since then.

Much has been written about the contrast between Japanese and UK companies, most notably Ronald Dore’s book “British Factory, Japanese Factory” of 1970 contrasting Hitachi and GEC, and a much more recent book by Inagaki and Whitaker in 2005 called “The New Community Firm” . This also charts the rise and decline of Hitachi as a classic Japanese “community company”, with very little diversity, but in which loyalty was repaid by security. By the late ‘90’s the need to globalise to survive was already being internally articulated, but the authors found that the policies touted to achieve that were implemented with lip-service only. Comparing Hitachi with its American equivalent GE, then under Jack Welch, it concluded that a company dedicated to looking after its core community of Japanese permanent employees would really struggle to introduce the degree of performance management and profit-oriented decision-making of a western enterprise.

This was the company I joined in 2004 as the first foreigner made responsible for proposing and implementing an overseas regional strategy. This job has given me many excitements, and a ringside seat in understanding the roots of the company and the huge changes and sacrifices which it has had to make to get to today’s position.

For example, at that time we were making televisions. Rather than have other people assemble them locally to our design, using components taken from the market, our management had invested huge sums in a modern factory in Miyazaki, employing thousands. One by one the shining models came out, each supposedly a winner, but never at a price at which we could make a profit in the European market. The simple fact was that there was global over-supply, and though we could make supremely good products, others could do so for half the price or less.

This story was repeated in semiconductors, displays and hard disk drives, leading in 2008 to losses at a level never seen by any Japanese company, and was the origin not only of a decision to exit these commodity sectors, but also to bring in a new management which reset the company’s strategy to the provision not of products but of solutions, not in the consumer, but in the global social infrastructure market.

Slowly this is paying off, but again it requires a shift in organisation and management which challenges every tea-drinking tenet of the so-called community firm.

To explain what I mean,

In value creation, the key is no longer production, but innovation: this requires individualism, and the breaking of internal silos. It needs teamwork and people with a combination of disciplines, rather than those who have perfected a single one. Monozukuri still matters, but is no longer a winning ingredient.

Japanese companies are very technology rich; but to take that technology overseas in the form of infrastructure projects requires a whole new range of skills which do not exist within a traditional manufacture and export organisation. Local political knowledge, commercial, project finance and management capability, and usually a local engineering base for customisation of technology; and the development of local supply chains to match global or local prices.

It requires the whole factory-led power structure to be turned inside out, and authority shifted to the front line, where the customer is. This is a complete break with the tradition whereby power resided with the factory side in Japan, to one where more commercial people outside Japan should become the key decision-takers. Sales units which previously handled foreign markets from Japan become redundant. It also means that the system of promoting domestic engineers over a lifetime into the leadership of the big business units will also evolve, marking a huge shift in career expectations.

In total, a gene pool heavily weighted to engineering needs to become multifaceted, and above all, international. This means changing the system whereby operations overseas are managed by expats on two or three year tours; it means promoting non-Japanese into leadership positions; it means measuring performance objectively, and promoting people with leadership potential much earlier in their careers; and recruiting young people with different backgrounds and skills. Implementing such change takes a long time.

One of my annual duties was to lecture the new intake of 800 young Japanese for 30 minutes on what it is to be “global”. My message was simply to travel, absorb, and think for yourself. “Talk to them in English” the Chairman said – “it will be good for them”. Well I tried, but since language was never among the entry criteria, the result was a predictable blank wall. Reverting to Japanese, I then joined the other executives for a walkabout among the new recruits at the drinks which concluded the induction ceremony. I pitched in to a group of young men, who shied away from me as if I had the ebola virus. I persisted in English for a while, but finally said to them in Japanese, “oh well then, what business group are you due to join?” “Ah, we, we’re the baseball group!” came the reply. The community firm lived on. More encouragingly I found two young girls who seemed more anxious to engage me in conversation. Not realising their nationality to begin with I engaged them in Japanese, whereupon they explained that they were foreign graduates, one Korean and one Chinese, from technical universities in the Kansai. “Goma-san”, they said, still in perfect Japanese, and looking around the room of 800 future colleagues. “What should we do to survive in a company like this?” I thought this question was a sign of great promise, and advised them to win respect as professionals, and voice their own opinions, firmly and politely.

Diversity is a weak point in many organisations, not only in Japan, but often proves in practice to be liberating for all concerned. The most enjoyable team I ever worked in was the UK Mission in New York in the 1990s where over half of our front line negotiators and the entire legal team were women. It is part, but only part of creating a healthy atmosphere of camaraderie and internal competition within a team. Unfortunately the role of many good women in the company is still to make TEA.

Governance is another vital topic, in the light of the Olympus and other similar failures. Part of the greatness of the Chairman who rescued the company from its disaster of 2008 was to bring diversity into the Board of Directors. I was quickly followed by three other non-Japanese Board members, two Americans and one Singaporean, all eminent in their fields. The Japanese Directors too were business men and women of deep experience. Simultaneous interpretation was provided, but it soon happened that conversation would flow spontaneously into English as well. More than that, with the introduction of foreigners who thought it was their duty to speak their opinions in Board meetings, the Japanese members also perked up and became much more interested in debate. It was a huge leap forward. By any international standards, the Board was a model. But my conclusion was that it is not the composition of the Board, but its degree of oversight and influence which is the real issue. The key shift is to move from a situation where the Board simply gives legal authority to decisions already made by the Executive, to one where the Board also debates strategy and can examine the management of the company.

In other words, governance should be not TEA, but SPARKLING WATER.

Huge contribution of Japanese companies to the UK economy.

Japanese companies have made a huge contribution to the UK economy and to the Government’s aim, still only half achieved, of rebalancing the economy towards manufacturing. It is estimated that they provide 140,000 jobs, and most notably the surplus in automotive exports that the UK now enjoys is in large measure due to Japanese (and now significantly Indian) investment.

Hitachi’s two largest overseas projects are coincidentally in the UK, and both very visible and vital from the point of view of renewing the country’s rail and power infrastructure. There isn’t time to go into detail, but in September we will open a factory in North East England to build the next generation of intercity and commuter trains; and the second is to plan and hopefully build a privately owned and operated nuclear power plant based on our latest Japanese operating design.

As a Brit of course, I’m very proud that the company is prepared to commit such huge investment to the British market. But from a company point of view, what is most encouraging are that these are transformational projects in the company’s journey towards becoming globally competitive.

In the rail case, the decision has been taken to put the global headquarters of the rail business in the UK. Even Japan now comes under this organisation. And that is the consequence of the exceptional foreign leader brought into the business twelve years ago.

In the nuclear case, it was a courageous decision to take a business which after the Fukushima earthquake had suffered a sudden domestic collapse, and re-orient it towards the global market. It is anything but simple, but a hugely motivating challenge.

Conclusions

On Japan-UK relations

On the UK-Japan relationship, I believe there is a huge reservoir of good will, common interest and complimentary talent. To sustain it we should focus not on sentiment but on what we can do together to address today’s issues – trade, conflict prevention, international development, anti-terrorism, and including now collaboration in defence preparedness.

With Japan there is a bond of trust, magnified by the contribution Japan continues to make to the UK economy and its support on international issues. This, and our common values, should be reflected in a special quality of political relationship and cooperation. Frequent dialogue and mutual openness, even in addressing our problems, is hugely valuable.

We must commit to burden-sharing with the United States through having sufficient readiness to look after ourselves in the first instance.

As far as Britain in Europe and Japan in Asia are concerned, retreat into isolation is an illusion and a dead end. We need to make these relationships work, and business should lead both countries to sensible policies.

More generally on world affairs.

With regard to globalisation and management

Putting the inner community first is a very natural and admirable human instinct, but as a principle of politics or business organisation it does not work.

Because we live in a globalised and competitive world, we have to be strong and efficient. More good and strength comes through openness and letting talent rise and lead.

There are many ways of binding an organisation together. The greatest is shared pride in success. Community, charity and compassion is precious but belongs at level of local and personal life.

Good politicians and business leaders are those who allow creativity and diversity to flourish, but can also articulate a sense of direction and what is right and wrong.

Finally