A few days ago the New Context Conference was held here in Tokyo, mainly about social network systems (SNS), top executives including CEO of LinkedIn, Facebook, and some exciting new photo, video conference and e-learning companies discussed market entry to Japan.

Japan’s two markets

Takeshi Natsuno, one of the three key DoCoMo managers who together started i-Mode and arguably started the world’s mobile internet revolution launching i-Mode back in February 1999 gave the keynote discussion. Natsuno shared his very interesting observation, that Japan consists of two markets:

new Japan = people below 50 years age and

old Japan = above 50 years age

…and having managed i-Mode (today: 48 million paying subscribers) for almost 10 years Natsuno-san is certainly one of the best to know. (Natsuno-san’s main job today is to make Japan’s very cute equivalent of YouTube profitable – read more about this in a future issue of our newsletters).

New Japan vs Old Japan in my talk at Stanford University

Actually, you’ll find a similar observation about “old Japan and new Japan” in my presentation entitled “New opportunities versus old mistakes: foreign companies in Japan’s high-tech markets” which I gave some years ago at Stanford University to faculty, students, alumni and silicon valley managers.- (You can view and download the slides of the presentation below.)

Natsuno-san talking at the New Context conference in Tokyo about old Japan, new Japan, the future of the mobile internet, and the mobile industry. Natsuno-san is one of the three inventors of i-Mode.

New entrant challenging Japan’s mobile incumbents Docomo and KDDI and SoftBank. A discussion between Dr Sachio Semmoto and Dr. Gerhard Fasol

Dr Sachio Semmoto: one of Japan’s most successful serial entrepreneurs

eMobile is Japan’s newest & fastest growing mobile operator, focused on mobile broadband – currently at HSDPA speeds up to 7.2 Mbps and HSUPA/EUL upload speeds up to 1.4 Mbps from Nov 20, 2008 (possibly upgraded to 5.7 Mbps from 2009) covering all major urban areas of Japan. Read an exclusive interview with eMobile’s founder and CEO, Dr. Sachio Semmoto below. eMobile‘s start is a resounding success: subscriber numbers will soon reach 1 million, and in October 2008, eMobile could attract 102,500 new subscribers – three times more than market leader DoCoMo (32,700) and two times more than KDDI (46,700). eMobile‘s market share is growing. eMobile was founded by Dr. Sachio Semmoto on January 5, 2005, and obtained the 3G spectrum license after a tough “beauty show” from Japan’s General Affairs Ministry on November 9, 2005 – almost exactly 3 years ago. At that time the Ministry gave new 3G spectrum licenses to three companies, however eMobile is the only one which actually built a new 3G network – the two other licensees returned their licenses to the Government unused.

Dr. Sachio Semmoto has very kindly agreed to an exclusive interview for our newsletter – read Dr Semmoto’s interview below. We are very grateful to Mr Takashi Igarashi of eMobile for his help and assistance in producing the interview. Dr. Semmoto is an extremely successful Japanese multi-entrepreneur. He is one of the co-founders of DDI (today part of KDDI), he founded the ADSL provider eAccess, and in 2005 he founded eMobile. Read Dr Semmoto’s interview about eMobile below.

In September 2008 eMobile attracted three times more new users than NTT-DoCoMo, and two times more new users than KDDI. eMobile will soon reach 1 million subscribers.

eMobile subscription numbers

Dr. Sachio Semmoto co-founded DDI (today part of KDDI), he founded ADSL provider eAccess and in 2005 he founded eMobile. He is Chairman and CEO of eMobile. Read Dr. Sachio Semmoto’s interview below.

Dr. Sachio Semmoto, Founder and CEO of eAccess and eMobile

Dr. Gerhard Fasol: Your company’s main product are 7.2 Mbit/sec data connections at about YEN 6000 (US$60, EURO 50)/month without any usage limitation at all – even if your subscribers upload or download enormous amounts of data including Skype and VOIP, or watch or upload movies all-day you do not reduce such users connection speed, and you do not charge extra. In Europe such totally unlimited data subscriptions do not exist to my knowledge – in addition most European telecom operators exclude VOIP or Skype from mobile data subscriptions – they even talk about “unfair usage” in their subscriber contracts. European telecom managers tell me that unlimited data subscriptions are impossible because of network capacity limitations and high electricity costs etc. What is it the “secret” that enables eMobile to offer unlimited data plans – without any usage restrictions at all?

Dr. Semmoto: We at EMOBILE have successfully developed and constructed a low cost, but high quality mobile network from scratch, based on leading-edge 3.5G/HSDPA technology base stations. HSDPA technology improves the usability of spectrum and network performance. We also have rich experience in fixed broadband markets like ADSL through eAccess, our group company.

Our “secret” is very simple:

1) high usability of network based on state-of-the-art technology, competitive low cost construction and operations, and 2) operational know-how from fixed broadband market (through eAccess).

Incumbent carriers offer flat-rate data service only because competition forced them to. We believe we have great competitive advantages against incumbent carriers.

Dr. Gerhard Fasol: What were the main difficulties you had to overcome to start eMobile?

Dr. Semmoto:

Financing. We are a completely independent venture company with no financial support from big corporations. We won the confidence of international qualified financial institutions like Goldman Sachs, and Temasek of Singapore, and succeeded to attract funding as large as 3.6 billion US$. This was before our business launch, therefore all we had to show to investors was just our business model and our management team, and our plans for a successful future business.

Dr. Gerhard Fasol: What was the most surprising experience for you building a new mobile operator from scratch?

Dr. Semmoto:

1) We were very fortunate that we could complete full funding back in 2006 for the following 5 years until 2011, before the current worldwide financial crisis 2) We won a business license and spectrum allocation from the government in 2005 after a tough beauty contest.

Dr. Gerhard Fasol: I remember the Japanese government wanted to have three new mobile networks and gave three new licenses, and your eMobile was the only company which actually succeeded to build a new network from scratch as desired by the Government (SoftBank acquired Vodafone including Vodafone’s license, and returned the new license to the Government and IP-Mobile could not find the finance) – congratulations!

Dr. Semmoto: You are completely correct. Softbank and we were fighting against each other for 15MHz in the 1.7GHz band. But the government had not decided the number of licensees initially, that means it was possible that only one company would win the whole 15MHz. As a result of the beauty contest, Softbank and we were both qualified and won 5MHz each, and the other 5MHz was reserved for additional allocation.

Dr. Gerhard Fasol: One of the key issues for telecom operators is often said to be to “avoid becoming a dumb data pipe”, i.e. to avoid commoditization and ever decreasing ARPU. What is your strategy that your company and your network does not become “a dumb pipe”, a commodity?

Dr. Semmoto:

We are confident in providing “a pipe”. It is a pipe but a GREAT pipe, mobile broadband service, and it is what customers are willing to use. I believe other Japanese mobile carriers are “too intelligent”, too far from real customer needs. High speed, flat-rate mobile broadband data is in itself a differentiated service. We will maintain competitiveness by continuously upgrading our data service from 3.5G to next generations (HSPA+ and LTE).

Dr. Gerhard Fasol: Assuming an ARPU of YEN 5000 for 1 million subscribers we can calculate that eMobile has sales of about YEN 60 Billion for 2009, i.e. about US$ 600 Million. Is eMobile profitable now or if not, when do you expect eMobile to become profitable?

Dr. Semmoto:

We expect to achieve 85 billion yen (about US$ 850 million) revenue with an accumulated subscriber number of approx. 1.4 million by the end of March 2009. eMobile has not turned to profit as of today. Under our projection we expect eMobile to break even on an annual EBITDA basis in fiscal year ending March 2010, then break even on net profit basis in fiscal year ending March 2011.

Dr. Gerhard Fasol: Your investors will expect eMobile to show profits and growth. In which areas do you like eMobile to grow? Are you planning to bring your experiences in the world’s most advanced market to other markets – international growth of eMobile? What is your long-term growth strategy for growth?

Dr. Semmoto:

eMobile plans to acquire 5 million subscribers by March 2012, and assumes Japanese mobile penetration to grow to over 100%. In line with our corporate mission of “providing a new and more efficient broadband life for all”, we focus on the Japanese mobile broadband market, which has more than 100 million subscribers. We consider that the whole broadband market will be the mobile broadband market in the future. As for further expansion into other markets, eMobile started a data card bundling service with the UMPCs (Ultra Mobile PC) in July 2008. UMPC is a type of PC that very much relies on internet connection. As we provide high-speed, reasonable-priced mobile internet connection environment, we have already built a win-win relationship with the PC market. Therefore, our strategy will always focus on mobile broadband. Meanwhile, we firmly believe that we will create a brand new potential market following the growth of PC and smart phone market. We do not have a plan to go to international markets for the moment.

Dr. Gerhard Fasol: Many people think that Japan has the world’s most advanced mobile phone market. Do you agree? And why do you think Japan could achieve this?

Dr. Semmoto:

I dare say, NO. Mobile phone rates in Japan have not been declining regardless of rapid market growth for the past decade, due to lack of competition. ARPU has not been declining much for a decade before new licenses were permitted in 2005. After Softbank and EMOBILE’s entry into the market for the first time after 1994, ARPU started to decline. The nominal undiscounted voice call charges of approx. 40YEN/min. are high and quite stable. Data speed was slow just before we started our business and, as I stated above, Japanese incumbent mobile carriers are emphasizing “value added services” too much. Penetration rate remains 80%, ranking as low as 50th globally.

Japanese mobile phone manufacturer lost their international market because Japan adopted non-standard technology, PDC, in 2G.

We need to introduce more competition, standard technology and “big-boned” telecommunication. When I say “big-boned” telecommunications, I don’t mean additional “added value” services, but the essentials of telecommunications: connection and transmission with reasonable price and high speed.

Dr. Gerhard Fasol: Many countries have decided to use one single radio technology path: GSM and in parallel 3GSM / UMTS. Japan and US on the other hand take the view today that the government should not pick technologies, and you find several competing radio technologies in Japan: wCDMA, CDMA2000, PHS, now soon Wimax. What do you think is better for a country: one single radio technology without competition, or a “technology shoot out” like in Japan, where companies compete in a pretty free market with different technologies?

Dr. Semmoto:

Competition among technologies is not bad in itself, but the most important thing is that those technologies are worldwide standard and adopted by many operators. When Japan adopted an internationally isolated technology, like PDC for 2G mobile, its market would became “Galapagos Islands” (ie local Japanese products cannot be exported to other markets, and products from other markets cannot be imported, creating beautiful but dead-end product lines). In this sense, I doubt the future of CDMA2000, PHS and WiMAX because major worldwide operators are going to GSM/W-CDMA/LTE as the mainstream technology.

Dr. Gerhard Fasol: for many years I have been puzzled by the fact that so many fantastic mobile services, handsets, i-Mode, mobile commerce have been developed in Japan, but there has been almost no success by Japanese companies (and foreign companies) to build a global business based on these technologies. For example, Japanese companies build fantastic mobile phones, but have no sales success outside Japan. If Japanese mobile phone makers would ask you how to succeed to sell Japanese made mobile phones outside Japan, or if DoCoMo would have asked you how to succeed with iMode outside Japan, what would your advice be for them?

Dr. Semmoto:

The reason why Japanese mobile phone makers have no success outside Japan is simple. They were based on non-standard technology, PDC (which is Japan’s 2G standard, which was not used in any other country outside Japan. Still today, more than 10 million PDC 2G mobile subscribers remain in Japan). DoCoMo’s i-mode is also a closed business model. Both cases have “non-openness” in common. Broadband data service is more like “Internet” and needs open service, open business models and open technology.

Dr. Gerhard Fasol: On the other hand, DoCoMo tightly controls most aspects of mobile phone handsets – which makes the production very expensive, and many handset producers have stopped making phones for DoCoMo: Mitsubishi, SONY-Ericsson have stopped, and SANYO sold the handset division to Kyocera. What do you think is the future of DoCoMo’s model of controlling mobile phone specifications? And what is eMobile’s handset strategy? Do you want to accept as many handsets as possible on your network, which seems to be SoftBank’s strategy?

Dr. Semmoto:

We emphasize standardized technology and open business models. It is not our strategy to control mobile phone specifications too much by committing the purchasing numbers, and by subsidizing developing and manufacturing costs because this would lead us to lose cost competitiveness. We are willing to adopt high-quality, worldwide standard and state-of-the-art handsets.

Dr. Gerhard Fasol: What do you think about the current trends in mobile handsets?

Dr. Semmoto:

Current trends in handsets are in two directions: simple phones and smart phones. Firstly, Japanese incumbent carriers have to change their strategy to place more emphasis on customer retention, therefore, the shipment of handset is decreasing in Japan. Both carriers and phone makers cannot support heavy product costs therefore the retail prices are increasing. Customers choose simple and easy-to-use handsets. Secondly, mobile broadband requires more open, multi-function handsets like smart phones.

Dr. Gerhard Fasol: What do you think mobile communications markets will look like in 10 years from now? What is your vision for the industry?

Dr. Semmoto:

the mobile market will become more data-focused, furthermore, broadband focused, which we already have experienced in the fixed telecommunication market (from narrowband data/voice to broadband internet). We will see through these mega trends and we will enforce our competitiveness in order to create brand new markets.

“New Age” mobile operator eMobile started with a “green field” nationwide HSDPA 3G network offering commercial services since March 31, 2007. By August 2008, eMobile has attracted more than 750,000 subscribers. eMobile‘s network covers about 85% of Japan at this time.

At an investors conference, eMobile‘s CEO recently explained, how his company could reduce the costs of the radio network and base stations down to 1/5th – 1/8th of the costs his competitors pay, by carefully selecting the two best base station manufacturers/vendors. Read who these two base station manufacturers are (one of them may be an unexpected choice) in the newest edition of our eMobile – report.

The US$ 1 laptop:

eMobile offers a US$ 1 (YEN 100) laptop – in combination with a 2 year 7.2 Mbps true flat-fee data subscription.

(note that this flat data fee plan has absolutely no data limit. Totally unlimited data plans for laptops are uncommon in Europe and US, where most “flat” data plans come with a very low “fair use” limit above which prices increase dramatically). Low priced laptops are a huge market success in Japan and put pressure on traditional laptop makers. eMobile offers subsidized Asus EEE’s / ASUSTeK EEE’s – and many other laptops, including also iBooks.

Digital mobile TV started in Japan in 2005 – about 3 years ago: KDDI/AU sold the first phones with digital mobile TV starting in October 2005, at the same time mobile TV was available for public testing. The official commercial service of mobile TV started on April 1, 2006.

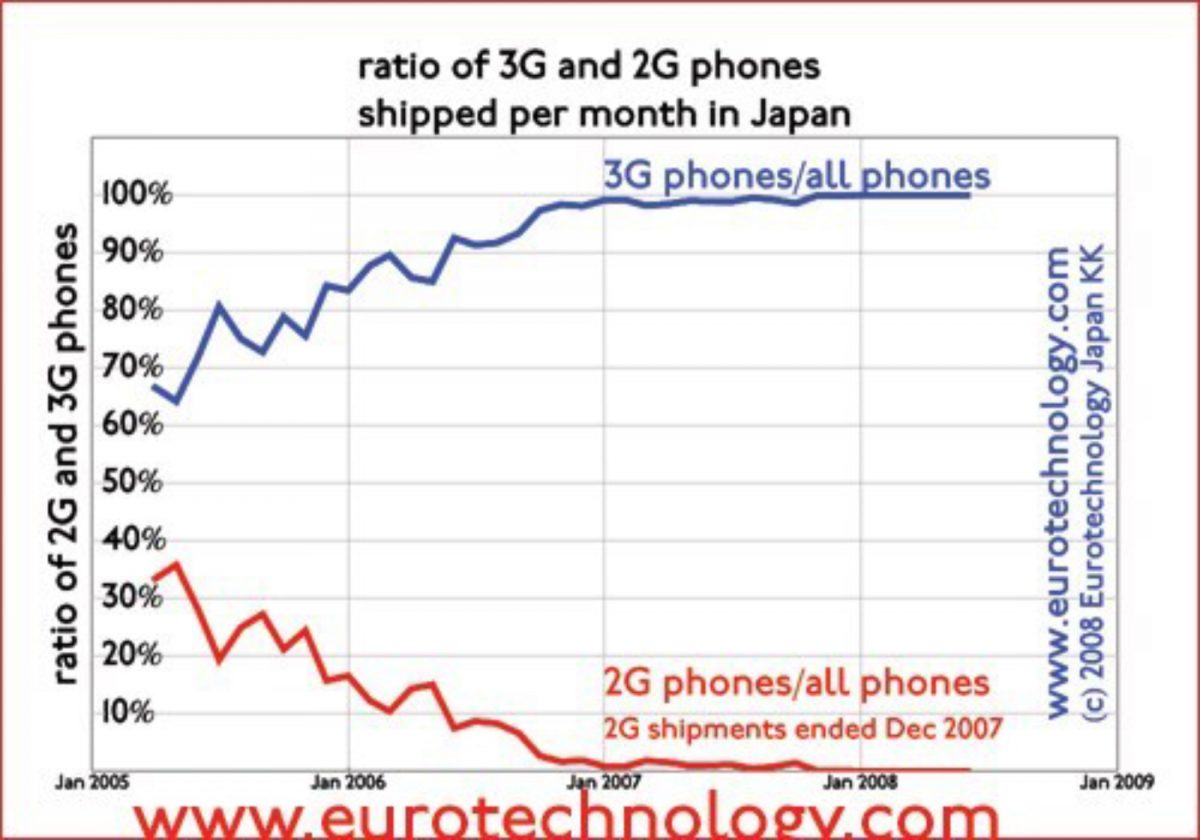

Today more than 75% ship with 1-seg mobile digital TV tuner and software, and the percentage is rapidly increasing as the figure below shows. Quite soon, almost all mobile phones in Japan will ship with digital mobile TV.

Percentage of Japanese mobile phones shipped with 1seg mobile TV built in2G vs 3G phones in Japan

KDDI/AU switched off 2G radio network in March 2008, Docomo and SoftBank to switch off 2G networks in 2009

Second generation (2G) phones silently bowed out of Japan’s market 8 months ago: the last 2G phones in Japan were shipped in December 2007. KDDI/AU switched off their 2G radio network in March 2008, this year, and both DoCoMo and SoftBank announced that they will switch off their slow and expensive 2G networks in the very near future (about 2009). Almost all other countries in the world either depend on legacy 2G networks only, or keep legacy 2G going while building out third generation in parallel. (Today’s 3G HSDPA phones transmit data up to 250 times faster than 2G phones did on a good day).

2G vs 3G phones in Japan

The last 2nd generation (2G) phones shipped in Japan in December 2007. Almost all other countries keep legacy 2G networks running – Japan just switches them off. More in our JCOMM report.

Tetsuzo Matsumoto (Senior Executive Vice-President and Board Member of SOFTBANK MOBILE Corporation), Gerhard Fasol (CEO, Eurotechnology Japan KK) and Dennis Normile (Japan Correspondent of SCIENCE Magazine, and FCCJ) discuss about the future of Japan’s mobile phone market.

“Will the iPhone trigger a turning point in Japan’s mobile phone industry?” (Foreign Correspondents’ Club of Japan, Tokyo Wednesday, August 13, 2008, 12:00-14:00)

(Photo: Copyright Foreign Correspondents’ Club of Japan, used with permission)

panel discussion at the Foreign Correspondents’ Club of Japan on the topic “Will The iPhone Trigger A Turning Point In Japan’s Mobile Phone Industry?”

How many iPhones did SoftBank sell in Japan during July?

Our estimate: between 75,000 – 125,000. Read on about how we arrived at this estimate.

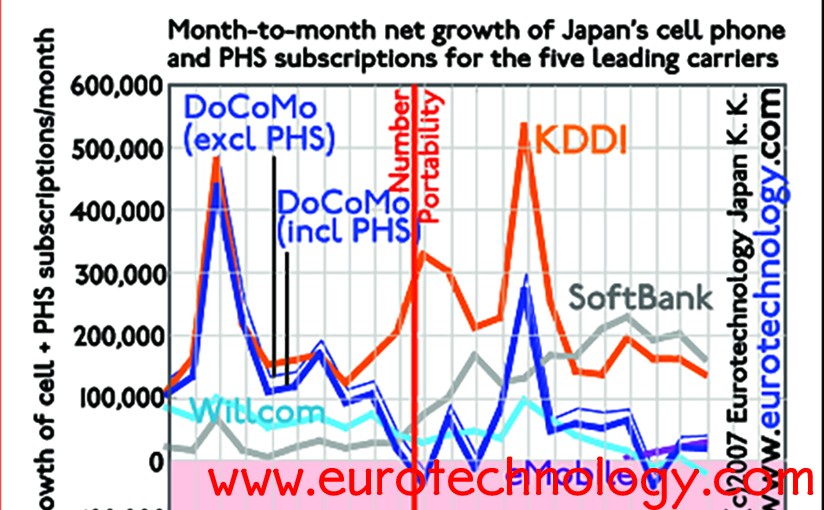

Net growth of mobile subscription numbers in Japan (Japan’s mobile market grows by about 5.5 million per year – for more analysis read our JCOMM-Report).

Growth/loss of mobile subscriptions of Japan’s mobile operators during the period 2006-2008

How did we arrive at the estimate of 75,000-125,000 iPhones sold in Japan during July?

When we analyze the Figure above, we can see that SoftBank‘s subscriber numbers increased by 158,900 during June 2008, and the monthly increase jumped to 215,400 during July 2008. We can also see that for no other month except for March 2006, March 2007, and March 2008 was there such a jump (in Japan March is the month of peak mobile phone sales, because new jobs traditionally start with the beginning of the financial year on April, 1). Since SoftBank did not introduce any other spectacular phones during July 2008, we can safely assume that most of the 56,500 net increase jump from June to July are iPhone sales to new subscribers, or new subscriptions for second phones, or number portability users moving over from DoCoMo or KDDI. However, this number would not count current SoftBank subscribers who are upgrading existing subscriptions from a previous older phone to an iPhone. Since we are not aware that SoftBank announces this number, we need to estimate it. If we assume that there were equal numbers of new subscriptions for iPhones as replacements, we would arrive at an estimate of 100,000 iPhones sold during July 2008 in Japan. If we estimate, that this second assumption has a +/- 50% error margin, then we arrive at an estimate of between 75,000-125,000 iPhones sold in Japan during July 2008.

Our estimate: about 640,000 – 1 Million iPhones may be sold in Japan during 2008:

If we assume that iPhone sales in Japan will continue at the current rate, then we can estimate that between 640,000 – 1 Million iPhones could be sold during the remaining part of 2008 in Japan, which would be about 1.2% – 2% of mobile phones sold during 2008.

NTT Data and BMW agreed today, that NTT Data will acquire 72.9% of outstanding shares of Cirquent GmbH

NTT Data thus gains BMW as largest customer in Europe

Today, August 1, 2008, NTT Data and BMW agreed, that NTT Data will acquire 72.9% of the outstanding shares of Cirquent GmbH in order to globalize.

Cirquent was part of the BMW Group, and is Germany’s 7th biggest system integrator

Between 1992-2008 Cirquent was part of the BMW Group. Cirquent is No. 7 in the Luenendonk ranking of German system integrators. Among Cirquent customers are BMW, Deutsche Boerse, Muenchner Rueck (reinsurer), and T-Mobile Germany. Cirquent has about 1800 employees and achieved sales of EURO 286 Million in 2007.

Cirquent share ownership ratios after this acquisition:

72.9% NTT Data

25.1% BMW AG

2% Cirquent GmbH employees

After this acquisition, BMW becomes NTT Data’s largest customer in Europe. We consider this acquisition an excellent move by NTT Data, NTT Data acquired Germany’s 7th largest system integrator, including about 1000 highly qualified employees, and at the same time also gained BMW as largest customer in Europe, together with a number of other blue chip customers such as Deutsche Boerse, Muencher Rueck and T-Mobile Germany.

Read more about Japan’s telecom sector in our J-COMM report.

In a terse one-line press announcement “SoftBank today announced it has signed an agreement with Apple to bring the iPhone to Japan later this year”. (Of course we are talking about the 3G i-Phone, because Japan has almost switched off the 2G networks, and has essentially stopped selling 2G phones for a couple of years now. The current initial 2G iPhone uses GSM and therefore cannot work in Japan, which has no GSM).

iPhone’s main competitors in Japan will be SHARP and KDDI’s design series, at least for the forseeable future – an entirely different story than in any other country in the world… read below.

Japan’s mobile phone handset market size and market shares in 2008 compared to the world market

About 25% of the global cellphone market in terms of cash value is in Japan. – Why? Japanese users want a lot more functions (navigation, mobile payment, QR code, mobile shopping, mobile music and video, mobile TV, …), and are happy to pay much more per phone. Japan is a totally different game: while NOKIA has about 40% of global market, NOKIA’s marketshare in Japan is almost zero.

Competing in Japan will be an entirely different story for the iPhone

Japan’s cell phone is entirely different than anywhere else in the world – recently some people including Japanese Government officials have used the nickname “Galapagos islands” for Japan’s insular and very advanced cellphone market. Indeed, our company in a project for the European Union Government documented in details how Japan’s cellphone services are 3-5 years ahead of Europe’s, ie a large range of cellphone services common in Japan have not yet been introduced in Europe.

For this reason, while the current 2G iPhone is at the high priced top-end in the US or in Europe, in Japan the 2G iPhone does not even work, because Japan has no GSM and essentially has not been selling any 2G phones any longer for a couple of years now. Many mobile services, which Japanese phone users have become accustomed to, are missing from the current 2G iPhone. Japan therefore will be a benchmark, and we expect that selling the iPhone in Japan together with Japanese customer feedback will help Apple to dramatically accelerate iPhone development. Competing in Japan will make the iPhone stronger we believe.

There are two YAHOO!s – YAHOO! Inc and YAHOO! KK. (ヤフー株式会社)

Yahoo! KK, ヤフー株式会社 is a Japanese corporation listed on the Tokyo Stock Exchange

Yahoo! KK (ヤフー株式会社) is not a full/100% subsidiary of Yahoo Inc, but Yahoo! KK is a publicly traded company, listed on the Tokyo Stock Exchange.

Ownership of Yahoo! KK (ヤフー株式会社)

35.45% by SoftBank

6.42% by SoftBank subsidiary SBBM

34.74% by Yahoo Inc.

23.39% other shareholders via Tokyo Stock Exchange

100% Total

Thus effectively:

SoftBank (SoftBank + SBBM) holds 41.87% of Yahoo! KK (ヤフー株式会社) shares

Yahoo Inc. holds 34.74% of shares

History background of Yahoo Japan

Masayoshi Son was one of the first and major investors in Yahoo Inc., and obtained the rights to build Yahoo Japan with part investment and license to trade marks and technology from Yahoo Inc.

Masayoshi Son and his SoftBank Group founded Yahoo Japan on January 31, 1996, and built Yahoo Japan into one of Japan’s most successful media and internet companies.

Yahoo KK started trading on the Tokyo Stock Exchange (Code 4689) with the IPO on October 28, 2003.

Market cap and size of Yahoo Inc vs Yahoo Japan

Yahoo Inc and Yahoo KK (ヤフー株式会社) are traded totally independently on different Stock Exchanges. Therefore share price and market capitalization are not directly related.

There are days when Yahoo KK (ヤフー株式会社) has higher market capitalization than Yahoo Inc minus the holding of Yahoo KK shares.

Yahoo Inc and Yahoo KK (=Yahoo Japan) market cap before and after Microsofts’ bidYahoo Inc vs Yahoo KK (Yahoo Japan) revenues and income

Preview – SoftBank today and 300 year vision report:

Our Report on “SoftBank today and 300 year vision” (approx 120 pages, pdf file)

Google, Apple, Nokia, HTC, Vodafone and are winning the driver’s seat of the global internet revolution. DoCoMo, KDDI and SoftBank essentially stay inside Japan for now – limiting their growth prospects and leaving global opportunities to others.

Market caps of Japan’s telecom operators compared to global telecom and internet companies

GOOGLE with Android and APPLE with iPhone are reaching for the driver’s seat of the global mobile data revolution. Global companies including GOOGLE, Vodafone, Apple and NOKIA grow to US$ 100s Billion valuations, while local companies NTT, DoCoMo, KDDI and SoftBank remain essentially limited to Japan’s market for now. Smartphone maker HTC increases impact – including in Japan.

SoftBank from 4th to 1st position within less than 12 months… SoftBank‘s turn-round of x-Vodafone-Japan, went faster than many expected. Within less than 12 months SoftBank went from last place to first place in customer sign-ups, overtaking even KDDI‘s super-popular AU.

Willcom recently suffers from SoftBank‘s revival, as well as from eMobile‘s flat rate data services.

Month-to-month net subscription growth/decline for Japan’s mobile phone operators during the period when mobile number portability (MNP) was introduced

In the last few days NTT, NTT-DoCoMo, KDDI and SoftBank announced their first half financial results. SoftBank and KDDI are the winners both for market share and for profits, while DoCoMo‘s results and market shares are sinking, and pulling the NTT-Group down at this time. Extrapolation indicates that DoCoMo‘s net profits may fall into the red about one year from now, drastic action is taken soon.

Net after-tax income of Japan’s top three mobile operators NTT-docomo, KDDI and SoftBank. Currently docomo’s net profits follows a downward trend, and risks to drop into the red, unless docomo takes drastic measures.

The thin lines show linear interpolations of quarterly net profit data. Our extrapolation seems to indicate that DoCoMo‘s net profit might fall into the red towards then end of calender year 2008 unless drastic action is taken. If current trends continue, SoftBank‘s net profits might exceed DoCoMo‘s mid-2008. We expect DoCoMo to take dramatic action before this happens.

Net after-tax income of Japan’s top three mobile operators NTT-docomo, KDDI and SoftBank. Currently docomo’s net profits follows a downward trend, and risks to drop into the red, unless docomo takes drastic measures.

People who want to participate need to register and link their plastic SUICA card, or their mobile SUICA (wallet phone with installed SUICA application) with a registered mobile or PC email address.

Whenever a registered participants touches the SUICA reader/writer on the side of a poster, links to a campaign homepage, coupons, event announcements or other information is sent to the registered PC or mobile phone email address.

The SuiPo system puts interactivity into posters and allows the advertiser to build an opt-in data base of interested people and to interact with them.

SuiPo = SuicaPoster: linking mobile phones and smartphones to posters for interactive advertising

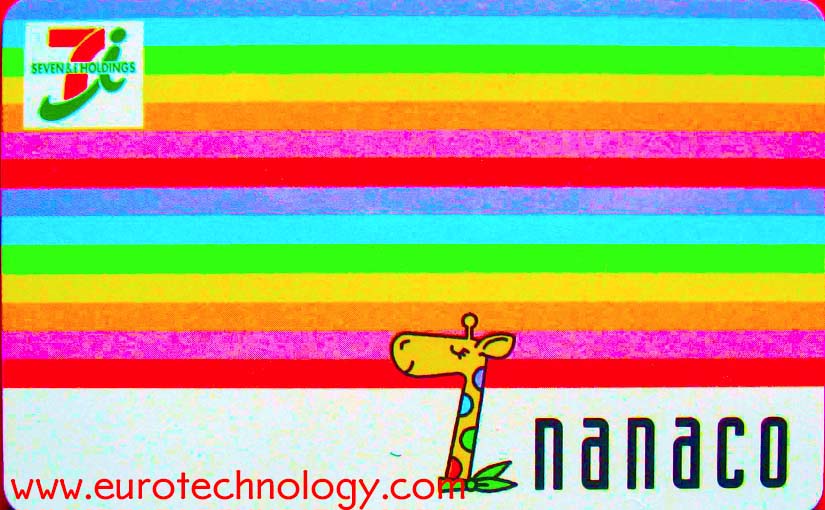

Seven-Eleven rolls out national electronic money and mobile payment system

Retail chain AEON follows with WAON e-cash and mobile money

This week two of Japan’s largest retail chains roll out electronic and mobile cash: Monday April 23rd, 2007 the Seven & I Holdings Group started “nanaco” and tomorrow, Friday April 27th, 2007, the AEON retail group will start “WAON”.

At first sight the massive roll-out of electronic cash and mobile payments systems during March and April this year here in Japan has been smooth and without problems (except for PASMO underestimating the success and running out of cards). However, when we look below the surface, clouds of a competitive storm are brewing. This storm might be followed by consolidation. Here are some examples:

PASMO cards were sold out within the first three weeks, and PASMO is now losing market share (and commission payments) to SUICA day-by-day – PASMO became a victim of it’s own success.

Seven-Eleven’s nanaco and AEON’s WAON use different business model variations

7-11’s “nanaco” offers twice as much discount as AEON Group’s “WAON”. Clearly “nanaco” is on a more aggressive course than “WAON”. We expect competition to heat up.

By the way- on Wednesday April 25th, 2007, two days after Seven-Eleven’s national roll-out of their e-money and mobile payment system, our company Eurotechnology Japan KK arranged a meeting between Seven-Eleven’s Chief e-Money architect and manager with the top-management of one of Europe’s most important mobile operators to enable the European operator to almost live experience an important global mile-stone in the development of e-money and mobile payments. To this day, to our knowledge, there is nothing like Seven-Eleven’s nanaco e-money and mobile payments system in Europe.

E-cash business model schematics

Schematic of Seven-Eleven’s nanaco e-money and mobile payment system

On March 31, 2007 eMobile will start high-speed (3.6 Mbps, HSDPA) mobile data services in Tokyo, Osaka and Nagoya, bringing disruption into the mobile data market in Japan.

While Willcom offers a flat data rate of YEN 9000 (US$ 77) per month for unlimited data transmission at 128kbps, eMobile will offer 30 times higher speed at about 1/2 the price:

3.6Mbps for PDAs, laptops and PCs for YEN 4980 (US$ 43, EURO 32) per month flat rate without any data limit (and n.b. no “fair use limit” as many European operators impose in the fine-print). …. and yes- you can probably also do wireless VOIP or Skype if you set this up yourself.

The established mobile operators (DoCoMo, KDDI/AU and SoftBank) do not offer any flat data rate to connecting PCs and laptops at this time.

(By the way- did you ever wonder why new entrants love flat rates? it’s because telecom billing systems are so expensive and complex. Flat rates are one of many competitive weapons new entrants have over incumbents…)

eMobile went to market with a splash in Japan – the first terminal was an HSDPA / wLAN and mobileTV equipped pre-smartphone smartphone

On Sunday, March 18, 2007, about 100 transportation companies in the Tokyo region switched to the near-field electronic money and payment system PASMO. Electronic money is a new battle field which JR-East pioneered with SUICA. Seven & I is still to throw it’s weight into the battle – read about today’s status of the electronic money marketplace in our “Mobile Payment and Keitai Credit” report.

A new multi-billion dollar power? Here is the character for PASMO: with an antenna on the hat, a pocket on the chest to store PASMO away, and wheels on the shoes, and in cherry-blossom pink… Does this cherry-blossom-pink guy look like he represents a new US$ multi-billion economic power?

PASMO – near field smart card for fare payment in Tokyo region – started Sunday, March 18, 2007 and exceeded all expectations

In his presentation, Dr. Fasol will explain the essentials of Japan’s mobile phone market, why and how it is so different to Europe’s. He will also talk about some of the reasons why it is so difficult for European companies to succeed and uncover opportunities and the keys to success for European companies in this important market.

Gerhard Fasol “Help – my mobile phone does not work!” – Why Japan’s mobile phone sector is so different from Europe’s, at the Finnish Chamber of Commerce in JapanGerhard Fasol “Help – my mobile phone does not work!” – Why Japan’s mobile phone sector is so different from Europe’s, at the Finnish Chamber of Commerce in JapanGerhard Fasol “Help – my mobile phone does not work!” – Why Japan’s mobile phone sector is so different from Europe’s, at the Finnish Chamber of Commerce in Japan

Example: mobile payment for the world’s busiest train line

CLSA – Asia-Pacific Markets – last week organized the “CLSA Japan Forum” here in Tokyo. About 800-1000 investment bankers, portfolio managers, investors, analysts came together. Since last year interest of global investors in Japan has increased a lot.

Eurotechnology Japan KK participated actively, and on Friday March 2, 2007, gave a presentation on:

Disneychannel places advertisements with huge QR-code on Tokyo’s roofs. People passing by point their mobile phones at Mickey’s QR-code, and the mobile phone takes them to Disneychannel’s mobile site.

QR codes were developed in the 1990s by Toyota affiliate Denso-Wave to manage car parts – today they are by far the best way to link mobile phones to almost anything. In many applications QR codes are cheaper, easier, more flexible and more secure than RFID and NFC.

QR codes were developed in the 1990s to manage car parts – today they are by far the best way to link mobile phones to almost anything. In many applications QR codes are cheaper, easier, more flexible and more secure than RFID and NFC.

The European Central Bank (based in Frankfurt) manages the EURO, is one of the world’s most important central banks, and uses QR-codes to link traditional PC-webpages to mobile pages.

Mobile Payment workshop and Global 3G Evolution Forum in Tokyo – Makuhari

3GPP, UMTS-Forum, Verizon and Docomo and others

22-25 January 2007 MarcusEvans organized the “Global 3G Evolution Forum” in Makuhari near Tokyo.

Speakers included:

Takanori Utano, Executive Vice-President and CTO of DoCoMo,

Takehiro Nakamura of NTT and Vice-Chairman of 3GPP

Jean-Pierre Bienaime, Chairman of the UMTS-Forum,

Gaston Ormazabal of Verizon Labs

and many other leading mobile communications managers from all over the world.

Jointly with Jan Larsson, General Strategy Manager of TeliaSonera International Carrier division, I chaired all sessions all day on Wednesday January 24, 2007.

Workshop on mobile payments

On Monday, January 22, 2007, I held a three hour workshop about “Mobile Payment”.

Mobile payment Japan, e-money and mobile credit report:

Japan’s mobile subscriber numbers grew by about 5 million in 2006. Because of the much higher ARPU, Japan’s mobile market again grew by a couple of Finlands during 2006. A growing number of people have more than one mobile phone, to take advantage of the best rates, eg for mail, voice and data. We expect growth to continue. Our analysis below shows that KDDI’s and AU’s gains are a lot larger than a superficial view of the statistics reveals – see our Figure below. Find a detailed review in the latest edition of our JCOMM-Report.

During 2006 Japan’s mobile subscription base grew by about 5 million – KDDI gained about 4.2 million new subscriptions and is the clear winner, despite shutting down its TuKa 2G service during this period

KDDI‘s subscriber gains during 2006 are much bigger than a superficial analysis reveals (see figure above):

KDDI’s AU mobile service gained about 4.2 million new subscribers during 2006 – more than twice as many than DoCoMo’s cellular service, which gained about 1.8 million new subscriptions.

Currently, KDDI is shutting down it’s TuKa 2G service, and DoCoMo is shutting down it’s PHS service. Both services together lost more than 2 million subscribers during 2006 – this is a much larger movement than due to number portability introduced on Oct 24, 2006.

KDDI offers both number portability and mobile email portability, and reports surprise that many former low-end TuKa users moved to top-end high-speed WIN (2.4 Mbps) data services.

For KDDI, enticing TuKa subscribers to move to high-end/high-speed AU services was an excellent preparation for number portability, and helped KDDI win in the first stage.