Hermann Hauser in a recent article on Project Syndicate, entitled “The Struggle for Technology Sovereignty in Europe” argues for “the UK and EU to jointly establish a €100 billion ($120 billion) Technology Sovereignty Fund to counter the $100 billion that the US is spending on its technology sovereignty and the even larger amounts China is mobilizing”. I argue here, that we should be thinking that 27+1 countries could create much larger funds in a world where single individuals like Masayoshi Son can create funds of that order.

Hermann Hauser became an entrepreneur right after finishing his PhD in the Cavendish Lab (Cambridge University, UK) around 1978 – on the same lab bench in the Cavendish as myself – and is arguably Europe’s first and most important technology venture investor. Hermann Hauser can be seen as the initiator of Europe’s VC industry. Hermann Hauser is also one of the co-founders of ARM and many other high-tech companies. For a discussion with Hermann see:

The thought of a €100 billion Technology Sovereignty Fund is of course a fantastic plan. As a starting point, thats of course a great idea, however in my opinion, much much more is needed. My thought would be that for European Technology Sovereignty, five or ten, or even more funds of that €100 billion size will be needed. In my opinion, better not only by governments, but by private individuals like European versions of Masayoshi Son.

Three thoughts, which I will illustrate below

a €100 billion fund for 27+1 countries is a lot smaller than the US$ 391 billion the single man Masayoshi Son is estimated to control (Vision funds plus three companies)

a €100 billion fund for 27+1 countries is much smaller than the sovereign funds of very much smaller countries:

Singapore (5.7 million people), sovereign funds: US$ 715 billion

Norway (5.3 million people), sovereign funds: US$ 1327 billion

My third point is that the assets in question (ARM) in Hermann Hauser’s Project Syndicate article would already use a large part of the proposed €100 billion fund.

To put a €100 billion fund for 27 EU Countries + UK into context:

Just one single man (Masayoshi Son, from a Korean immigrant family to Japan) controls at least two funds + and to some extent several companies, worth in total on the order of US$ 391 billion as follows:

the current “fair value” of the first + second Vision Funds is reported as US$ 154 Billion.

In addition, Masayoshi Son also controls (to some extent) the listed companies, which he often uses as acquisition and finance vehicles:

SoftBank Group Corp [TSE: 9984]: market cap = US$ 130 billion

SoftBank Corp [TSE: 9434]: market cap = US$ 67 billion

Z Holdings Corp [TSE:4689]: market cap = US$ 40 billion (includes Yahoo Japan Corp + LINE)

That is just one single man, who created all this from zero, not 27+1 countries.

Or as another comparison, Singapore has built at least two sovereign funds in total estimated to be worth US$ 715 billion. Singapore is one single relatively small country compared to 27+1 European countries (population of Singapore is about 5 million, about the same as Norway, and about the same as the Berlin region)

Singapore Sovereign Wealth Fund GIC estimated value US$ 488 billion

Temasec Holdings US$ 227 billion

Norway’s sovereign funds (population about 5 million):

Sovereign Pension Fund – Foreign US$ 1300 billion assets

Sovereign Pension Fund – Norway US$ 27 billion assets

My third point is that a single €100 billion fund is of comparable size of developed assets in question. eg. ARM’s current value would be a substantial part of a potential €100 billion fund. This means that after acquiring two or three companies of the value of ARM this fund would already be exhausted.

As another example, the strategic German mRNA company BioNTech (which among other therapies developed the BioNTech Covid Vaccine in cooperation with Pfizer) has a current market cap of US$ 51 billion. If a situation would arise that such a Sovereign fund would acquire a company such as BioNTech, that would again use up a large fraction – if not almost all of this fund. In my opinion, although of course a €100 billion fund investing in European technology companies in addition to existing substantial VC and investment funds would be great, this is not huge – even relatively small – compared both to the value of many assets in question, and also to the funds some private individuals (eg Masayoshi Son) or 5 million people countries (like Singapore or Norway) manage to build.

So I think many more than a single €100 billion fund would be needed for Technology Sovereignty – I hope circumstances will develop where even more can be invested in European ventures than today. Hermann Hauser’s proposal is certainly a great step in the right direction- many more such steps would be great!

Former President of the EFTA Court, Carl Baudenbacher

Former President of the EFTA Court, Carl Baudenbacher

Gerhard Fasol: Professor Baudenbacher, could you explain in simple terms, what the EFTA Court and your work leading the EFTA Court for many years, means for businesses in Europe, and also businesses in Japan.

Carl Baudenbacher: The EFTA Court is the second tribunal in the European Economic Area (EEA) next to the Court of Justice of the European Union (ECJ). The EEA consists of the EU and its 28 (soon 27) Member States which form one pillar and the three EFTA States Iceland, Liechtenstein and Norway which form the other pillar. Businesses from these countries have access to the EFTA Court. That includes Japanese companies which are active in Europe. I should add that a group of leading Japanese professors from the universities of Waseda, Tokyo and Kyoto have for many years been doing research concerning the EFTA Court.

Gerhard Fasol: Can you illustrate the impact of the EFTA Court with an example? What do you consider your most important case?

Carl Baudenbacher: In Fosen-Linjen (E-16/16), we decided that a public authority which awards a public contract to the wrong bidder, may be liable for a simple breach of public procurement rules and not only for a serious breach. This judgment may have an impact on the jurisprudence of the ECJ, but also of the highest courts, say, in the U.K., Sweden, Norway, Denmark. It could also be that it influences a Japanese court.

Our most important case was probably Icesave (E-16/11) where we held that in a systemic financial crisis a State is not liable for the incapability of its banks’ deposit guarantee scheme to compensate depositors in other countries.

Gerhard Fasol: Do I understand correctly, that the EFTA Court is focused on the relationship between Governments and business. Surely the impact is bigger and beyond Government and business only?

Carl Baudenbacher: The EFTA Court decides cases involving the relationship between Governments and business, for example concerning ownership in energy companies or concerning taxation but also between businesses, for example conflicts between banks and insurance companies and consumers.

Former President of the EFTA Court, Carl Baudenbacher

Gerhard Fasol: Professor Baudenbacher, you devoted your life to lead the development of international business law, which is at the core of the post WW2 rule based global system, which is now faced with stronger nationalism, in particular the Trump presidency.

Can you explain us what you see as your main achievements, and do you feel these achievements are now in danger in view of recent political developments?

Carl Baudenbacher: I have been a university professor in Switzerland, Germany, the US and Iceland, an author, arbitrator, corporate and political consultant, and a European judge. As a professor, I have founded the post graduate program Executive Master of International Business Law of the University of St. Gallen. This autonomous global program entertains cooperations with American and Asian universities. In Japan, Waseda is our partner. My main achievement has probably been the positioning of the EFTA Court as a voice to be heard. The establishment of international courts, such as the ECJ, the EFTA Court or the WTO Appellate Body has been called the “judicialisation” of international law. This has been beneficial for businesses. With the Trump presidency, there is the risk that the rule based global system will be replaced by archaic mechanisms such as retaliation. Free trade has already suffered and will further suffer.

Gerhard Fasol: While we do see this emergence of nationalism, important major trade agreements between the EU and Japan, between the EU and Canada and many others have been agreed. From your experience leading the EFTA Court, do you think we will see a future of several ECJ or EFTA-type courts for different regional trade groups? Or will we go back to national courts, driven by renewed nationalism?

Carl Baudenbacher: What we are seeing is in all likelihood more than a crisis of the post WW2 global trade system. The former German Foreign Minister Joschka Fischer speaks of the end of the Pax Americana. I leave the question open whether the EU has done its homework as regards its trade balance. A natural reaction to the American move would be that Europe and Asia move closer together. If global trade is in peril, regional trade agreements come to the fore. In my experience, regional courts such as the ECJ and the EFTA Court offer a lot of advantages. But the judges must be aware that they cannot interfere excessively with the sovereignty of the Member States. At the same time, going back to national courts is in my view no solution.

Former President of the EFTA Court, Carl Baudenbacher

Gerhard Fasol: You often refer to judicial dialogue. Why do you think judicial dialogue is so defining for your work at the EFTA Court, what is its importance beyond? How do you see criticism?

Carl Baudenbacher: What I mean with judicial dialogue is the dialogue between high courts. In Europe, we see such interaction between the ECJ, the EFTA Court and the European Court of Human Rights. National Supreme Courts may also be involved. Let me give you an example. In many countries around the globe dockers have been able to impose collective agreements on ship owners that give them a priority right to load and unload ships. In 2016, the EFTA Court ruled in the landmark case Holship (E-14/15) that such a system is incompatible with competition law. The Supreme Court of Norway has followed the EFTA Court. The Norwegian unions have now brought the matter before the European Court of Human Rights. At stake is, inter alia, the right of businesses to employ non-organised dockers. Sooner or later, this question will also arise in the ECJ. Obviously it could also end up before any other high court in the world. Then it would be natural for that court to look into how other courts have resolved the problem.

Gerhard Fasol: How do you see the developments between EU, UK, EFTA and Switzerland? You are actively promoting the EFTA court, and by extension EFTA for a possible future home for the UK. Where do you see the advantages for EFTA and UK – keeping in mind that EFTA was co-founded by UK.

Carl Baudenbacher: The UK intends to leave the EU because it wants to limit integration to economic matters; it doesn’t want to be part of a political Union. EFTA which was founded under British leadership is an intergovernmental club which focuses on trade. The EFTA Court has in its case law upheld EFTA values such as free trade, open markets, efficiency, a modern image of man.

Gerhard Fasol: Finally, here in Japan many business people are concerned with Brexit – especially Japanese manufacturing and financial companies have a strong presence in the UK. How do you see Brexit – from your neutral Swiss viewpoint, and from your EFTA Court viewpoint – both outside the EU. How do you see Europe develop?

Carl Baudenbacher: The Brexit decision of June 2016 was obviously a shock for Japanese businesses which had used the UK as a gateway to the EU. I have already elaborated on this at Keidanren on 1 September 2016 and then again in September 2017 at RIETI. But the British people have spoken. In my view it would be crucial for Britain to retain access to the EU single market. This would also be important for Japanese investors. The countries which are members of the EFTA Court do have this access. If Britain would subject itself to the EFTA Court, Switzerland might do the same. We would then have two structures in Europe and consequently a certain systemic competition.

Former President of the EFTA Court, Carl Baudenbacher

Carl Baudenbacher – Profile

Professor Dr. iur. Dr. rer. pol. h.c. Carl Baudenbacher has served as a judge on the EFTA Court in Luxembourg from September 1995 to 9 April 2018. From 2003 to 2017 he was the Court’s President. Baudenbacher was the Judge Rapporteur in many of the Court’s landmark cases.

From 1987 to 2013, Carl Baudenbacher was the Chair of Private, Commercial and Economic Law at the University of St. Gallen (Switzerland). Between 1993 and 2004, he was a permanent visiting professor at the University of Texas at Austin. In 1996 he founded the global autonomous program Executive M.B.L.-HSG of St. Gallen University which has a foot in Japan.

On 9 April 2018, Baudenbacher stepped down from the EFTA Court bench. He will open his own firm focusing on arbitration and corporate and government consulting. His special fields are EU and EEA law, Brexit and the relationship Switzerland – EU.

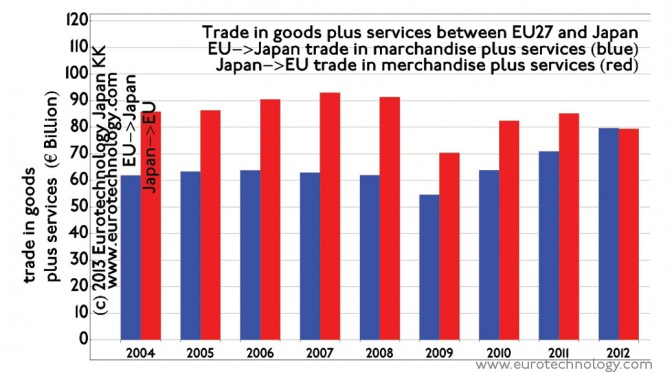

EU-Japan Free Trade Agreement and Economic Partnership Agreement nearing conclusion, maybe this summer.

EU and Japan started to prepare for Free Trade Agreement (FTA) and the political framework Economic Partnership Agreement (EPA) at the 20th EU-Japan Summit in May 2011, three years after Japan and USA had jointed the Trans-Pacific Partnership (TPP) negotiations.

For several years, TPP was catching headlines, Prime Minister Shinzo Abe saw TPP as a core component of his Abenomics program to restarted Japan’s economy from 20 years of stagnation. The EU-Japan FTA and EPA negotiations always seemed to be in the shadow of TPP.

In the meantime, President Trump has decided to withdraw from TPP, and the UK seems to be on the way to BREXIT.

The EU-Japan FTA and EPA negotiations have moved to the center of attention, and seem to near conclusion.

Trade in goods is only one of 14 different working groups – a modern FTA is very complex

Trade in goods (including Market Access, General Rules and Trade Remedies)

Non-Tariff Measures and Technical Barriers to Trade

Other issues (General and Regulatory Cooperation, Business Environment, Animal Welfare)

Trade and Sustainable Development

Dispute Settlement

General, Institutional and Final Provisions and Transparency

Don’t be blinded: Free Trade Agreements reduce business costs and risks and create access – but they don’t guarantee business success

the Free Trade Agreement will open new sectors previously closed to any foreign company in Japan, e.g. railways procurement, and reduce many barriers, however, top-class leadership, deep Japan knowledge at all levels of management, sufficient investments, and products or services with a large competitive advantage remain crucial to success in Japan.

Free Trade Agreements reduce business costs and risks, but do not eliminate them.

More about the EU-Japan Free Trade (FTA) and Economic Partnership Agreements (EPA):

Japan’s economy grows five quarters in a row, and Japan Post books losses of YEN 400.33 billion (US$ 3.6 billion) for an acquisition in Australia

Japan GDP growth, growth of 2%/year. Still, Japan’s economy is the same size as in 2000, while countries like France, Germany, UK today are double the size as in the year 2000

Japan GDP growth: We have seen 5 quarters of economic growth in Japan, for the January-March 2017 quarter the consensus is that the Japanese Government is likely to announce economic growth corresponding to an annual growth rate of around 2%/year (update: Japan’s Government announced an annual growth rate of 2.2%/year).

Generally the business mood in Japan is optimistic now, personal consumption and industrial orders are growing. We see investments in preparation for the 2020 Olympics. Venture start-ups and venture investments are growing, while still at a low level, we see venture businesses developing not only in Tokyo, but also in regional centers around Japan.

One mid-term risk to Japan GDP growth is the potential implementation of the postponed consumption tax rate increase.

The big picture however is, Japan’s economy today is approximately the same size as 17 years ago in 2000. During the same 17 years most major economies, e.g. France, Germany, UK have doubled in size. France, Germany, UK’s economies today are about twice the size as in 2000, while Japan’s economy today is about the same size as in 2000. Quarterly GDP figures just measure the short term fluctuations of this long term behavior.

Rico Hizon: so what would Japan have to do to restart long term growth?

Gerhard Fasol’s answer

Japan would have to do three things to restart economic growth long term:

Population: Implement policies to make it easier for families to have children, shift spending from the aged to children, improve eduction, shorter work hours, build children’s day care centers, gender equality

Implement Prime Minister Abe’s “third arrow”, the reforms. Deregulation not just in a few “special zones” but nation wide.

Improve corporate governance to improve company’s growth, globalization and management.

Japan Post trips up on globalization: books YEN 400.33 (US$ 3.6 billion) losses due to an acquisition in Australia – with a Toshiba connection

Japan Post announced a loss of YEN 400.33 (US$ 3.6 billion), and a resulting net loss of YEN 28.98 billion (US$ 260 million) for the fiscal year ending March 31, 2017.

Japan Post Holdings was launched on the Tokyo Stock Exchange with the IPO on Nov 4, 2015.

Investors expect major growth of Japan Post Holdings into a global business, such as Deutsche Post has with privatization and later the acquisition and merger with the global logistics group DH about 20 years ago.

Around the time of the IPO Japan Post announced the acquisition of the Australian logistics group Toll for about YEN 620 billion (US$ 5.5 billion), while Toll’s market cap previous to the acquisition was about YEN 410 billion (US$ 3.7 billion).

Japan Post’s recent write-down at Toll is about equal its pre-acquisition market cap, or about 65% of the acquisition prize.

The deep problem of Japan Post’s steep write-downs at the Australian acquisition Toll, is that this casts doubts on Japan Post’s developments into a global business.

The Toshiba connection: Japan Post’s former CEO, Taizo Nishimuro (西室 泰三), previously served as CEO and Chairman of Toshiba

CEO of Japan Post at the time of the questionable Toll acquisition was no other than Mr Taizo Nishimuro (西室 泰三), former CEO and Chairman of Toshiba, now honorary advisor of Toshiba, who spent all his career at Toshiba, working at Toshiba since 1961. Toshiba is currently in severe difficulties caused primarily by Toshiba’s acquisitions of US nuclear construction firms, however Toshiba’s fundamental problems go back much much longer.

Japan Post Holding [6178]

Japan Post Holdings was founded on 23 January 2006, following the path to privatization of Japan’s national Post Office initiated by Prime Minister Koizumi.

Japan Post Holdings is listed on the Tokyo Stock Exchange (No. 6178), IPO was on 4 November 2015, and has five divisions (since October 2012 three divisions):

Japan Post Service (日本郵便株式会社): mail delivery. Merged on October 1, 2012 with Japan Post Network to form Japan Post Co. Ltd.(日本郵便株式会社). Japan Post Co. Ltd is a 100% subsidiary of Japan Post Holdings (Tokyo Stock Exchange: 6178)

(Japan Post Network (郵便局株式会社): Post Offices = retail and real estate. Merged with Japan Post Service to form Japan Post Co., Ltd. on October 1, 2012).

Bill Emmott is an independent writer and consultant on international affairs, board director, and from 1993 until 2006 was editor of The Economist. http://www.billemmott.com

Gerhard Fasol is physicist, board director, entrepreneur, M&A advisor in Tokyo. http://fasol.com/

A conversation about Japan’s future

Bill Emmott:

I came first to Japan in 1983 as Economist Tokyo Bureau Chief, staying until 1986. Then in 1988 I came back on sabbatical leave and wrote “The sun also sets: why Japan will not be number one”, which against my expectation when it was published in 1989 found big resonance in Japan. The stock market was plunging, and mine was the most immediately available explanation. Ever since, journalists have constantly asked me what the sun is doing now! It also meant that even when I became editor in chief of The Economist in 1993 I spent much more time focused on Japan than I had expected, visiting as often as I could to keep track of the post-bubble developments, and wrote a book that appeared only in Japanese translation called “Kanrio no Taizai”, or the bureaucrats’ deadly sins. But later, with Prime Minister Koizumi consolidating reforms, and the banking system at last getting cleared up, I sent myself back in 2005 to research and wrote a much more optimistic special supplement for The Economist which became a book, “The sun also rises”.

Throughout the 35 years since I first came to Japan, I have both been fascinated and struck by the fact that although this is in so many ways an inward-looking self-contained nation, foreign observers are listened to and even have a chance of having a positive impact.

One element that had featured consistently in my writings ever since the 1980s had been observations and expectations for a growing role for women in employment and power. This seemed logical given that, at least before the bubble burst, Japan was heading for a labour shortage, but also the Equal Employment Law of 1986 had led to more females being recruited by major organisations. Japan’s excellent education surely meant that the underused half (= women) of the adult population would soon be used more productively.

Of course, this has developed a lot more slowly than I expected or hoped, partly for cultural reasons but also because Japan has not in fact had a labour shortage, until now.

I wanted to meet you, Gerhard tonight because we both are fascinated by the role Japanese women have in making Japan such a fascinating country, and how the many really strong Japanese women could have key roles in bringing growth and dynamic change back to Japan.

Could Japanese women have bigger roles for the development of Japan?

What is holding women back in Japan?

Who are the role models?

I am making interviews with high-achieving Japanese women to try to find answers, and plan to compile them into a book later this year. What would you say, Gerhard? And anyway, how did you end up here?

Gerhard Fasol:

My path to Japan is quite different than yours, Bill. I came to Japan first in 1984 as Fellow of Trinity College Cambridge, and scientist at the Max-Planck-Institute in Stuttgart, part of a project to build a research cooperation with NTT’s R&D labs. I saw that Japan was very important in technology and weakly linked to the outside – and still is today, I think. So in 1984 I decided to make Japan my second professional focus in addition to physics and electronics. Like you – the deeper I get into Japan, the more I learn about Japan, the greater my fascination, and my motivation to contribute.

Now I am working on many different projects, working on international technology M&A projects, and I am also one of a microscopic number of foreigners on the Board of Directors of a stock market listed Japanese corporation – reforming Japanese corporate governance hands-on.

Could Japanese women have bigger roles for the development of Japan?

Gerhard Fasol:

I think that the equal participation of women in leadership is directly linked to the population issue, ie the number of children born.

while in Sweden 44% of Members of Parliament are women,

37% in Germany and

26% in France –

the world average is 23% women in Parliaments.

In Japan the ratio of women in Parliament has increased from 1% in 1990 to 10% in 2016, so there is progress. If we extrapolate, and if the trend continues, then it might take another 30 years or so until Japan reaches world average in terms of women bringing women’s views into Parliament, and taking part in making the laws. And it might take Japan 100 years to reach Scandinavian standards of women’s participation in making the laws of the land – unless there is some acceleration in Japan.

Japan’s most powerful Ministry, the Ministry of Finance, did not hire any women into career positions for a period of about 10 years!

At the 2015 New Year event of Kyoto Bank, Keidanren Chairman Mr Sadayuki Sakakibara showed that Japan’s spending on aged people is dramatically higher than spending on children, and that this ratio is increasing with time, Japan spends more and more on aged people and less and less on children. There are two ways to look at this situation:

one way is to say: we have an aging society, therefore its only natural to spend more on

the aged, and less for children

the opposite way to look at the same situation is to say: we are spending less and less for children, no wonder we have fewer and fewer children. If we did more for young people, maybe people will have more children….

Actually most Japanese women I talk to want 2-3 children, but many cannot for financial reasons.

By nature, women give birth to children, not men, so more women in decision making positions including Government and Parliament will bring children’s issues into decision making.

As an example, child birth costs in Japan are not covered by health insurance, while they are everywhere in Europe. There are many other open and hidden costs of having children in Japan compared to Europe.

The most important factor are mindsets. The key to give more power to women in Japan is to change mindsets, to change the way of thinking.

As an example, the Prefecture of Kanagawa in 2015 created the “woman act” committee, under the slogan “women, step by step, take more responsibility”, however this committee both in 2015 and also in 2016 consisted of 11 men – not one single woman leader: http://www.pref.kanagawa.jp/osirase/0050/womanact/

here archived with photographs on the wayback-machine/ internet archive

Why not create a committee of 11 women leaders to lead efforts on gender equality in Kanagawa Prefecture? Why not promote women to leadership positions in Kanagawa Prefecture?

Another factor holding women back are the very long working hours common in Japan. As an example, at a recent EU-Japan gender equality conference, the Danish polician Astrid Krag, who was Minister for Health and Prevention at the age of 29 – 32 years, and who has two children, explaned that in the Parliament of Denmark the decision was taken not to take any vote after 4pm, so that Members of Parliament can be back home by 5pm, collect children from daycare centers in time etc. So in the Parliament of Denmark it is guaranteed that Members of Parliament can leave at 4pm. In today’s Japan such action is unthinkable, age 29 – with young children – would be unbelievably young for a Government Minister in Japan. https://en.wikipedia.org/wiki/Astrid_Krag

Late-night or overnight sessions at work, including Parliament, makes life incredibly difficult in Japan for parents with young children, doubtlessly contributing to the small number of women in top positions in Japan.

Who are the role models?

Gerhard Fasol:

Despite these difficulties, there is a substantial number of very strong women in Japan, who have worked their way up into leadership positions.

Examples are the Mayor of Yokohama, Ms Fumiko Hayashi, who succeeded in a very distinguished business career, and the Governor of Tokyo, Ms Yuriko Koike, who won the election on her own as an independent candidate, because she did not receive the backing of her party.

Bill Emmott:

That is great, as I have now interviewed Koike-san and plan to interview Hayashi-san during my next visit. Personally, as well as admiring women who have made it to the top in the tough political world I also admire and am interested in women succeeding as entrepreneurs and as executives in entrepreneurial companies. By starting and building their own companies, women can really create new realities, showing that new organisational cultures are possible in a Japanese context. Do you agree?

Science is also an interesting area. We have women leaders in Japanese medicine, I invited some for the Ludwig Boltzmann Forum on women’s development and leadership http://www.boltzmann.com/forum/2016-womens-leadership/

The tantalizing issue is that the key is to change mindsets, and thats at the same time superficially easy, but at the same time incredibly hard. Thus outstanding strong Japanese women – and there are many of them – have a choice either to work their way up to the top in Japan, start their own company in Japan, or on the other hand to move to Europe, elsewhere in Asia, or to the USA – I know several strong Japanese women, including several Japanese medical doctors, who have moved to Europe or USA. They might of course come back to Japan at a later stage bringing global views and experiences to leadership positions in Japan in the future. I am very optimistic for the future of Japan – sometimes I wish things were moving faster.

Bill Emmott:

I agree entirely. I see Japanese women as both victims of the slow speed of change and as solutions to it. They really could make the Japan of 2030 look quite different, in all sorts of ways. It will be fascinating to watch.

Bill Emmott and Gerhard Fasol met at the restaurant MusMus in Tokyo

left to right: Gerhard Fasol, Ms Atsuko Konta (Manager of the restaurant MusMus), Bill Emmott

Copyright (c) 2017 by Bill Emmott and Gerhard Fasol. All Rights Reserved.

NTT Docomo announced the start of i-Mode on February 22, 1999 at a press conference in Tokyo

Today, 18 years ago, on February 22, 1999, Mari Matsunaga, Takeshi Natsuno, and Keiichi Enoki announced the start of the world’s first successful mobile internet service to a small number of people who made it to NTT Docomo’s press conference in Tokyo.

For many years, Japan was the global hotspot for mobile internet, mobile broadband, fixed net broadband (FTTH), there is a very long list of inventions, innovation, new services and products which were successfully brought to market in Japan, and in some cases it took 10 years or longer for these same services to succeed elsewhere in the world.

Examples of services and products which saw their invention, or first successful global mass market introduction in Japan include:

first successful mobile internet services (i-Mode, EZweb, and JSky)

Inventing the mobile internet vs capturing global value

Undoubtedly the biggest success story emerging from Japan’s pioneering mobile internet days is SoftBank

After Vodafone acquired a controlling stake in Japan Telecom, it took Vodafone at least one year to realize that instead of a far east backwater waiting for Vodafone, Japan’s mobile market was actually years ahead of Europe at that time. By the time Vodafone realized that instead of sailing into an easy market, they had actually entered the world’s most ferociously competitive market, it was too late, Vodafone sold its Japan operations to SoftBank, which turned out the failing Vodafone-Japan within a few months of intense efforts. SoftBank’s acquisition of Vodafone-Japan and the successful turn-round became the basis for SoftBank to implement Masayoshi Son’s plan to create one of the world’s most important companies.

Other Japanese success stories resulting from pioneering the mobile internet

Beyond games, Japan has created a vibrant sector of internet and mobile ventures, founded in the wave of Japan’s mobile internet and FTTH broadband adoption. However, because of Japan’s well known Galapagos syndrome, few have made it into global success stories yet. However, its not too late.

eMoji made it into MoMa, and the iPhone.

QR codes are all over China, however not monetized by Denso Wave, the Toyota family company which invented QR codes for automotive parts management.

This morning 7:30am I was interviewed on BBC TV Asia Business Report about an update of Toshiba’s ongoing crisis, which has been 20 years in the making.

Here some notes in preparation for my interview.

What is Toshiba’s situation now?

Toshiba’s market cap today is YEN 1024 billion = US$ 9.6 billion.

Toshiba is expected today to announce write-off provisions on the order of US$ 6 billion.

Toshiba owes about US$ 5 billion to main banks as follows:

Mizuho YEN 183.4 billion

SMBC YEN 176.8 billion

Sumitomo Mitsui Trust Holdings YEN 131.0 billion

BTMU YEN 111.2 billion

Total YEN 602.4 billion = US$ 5.3 billion

Toshiba is on notice for delisting by the Tokyo and Nagoya Stock Exchanges, and faces the risk of being delisted by March 15, 2017, i.e. in about 4 weeks from now.

Toshiba is trying to raise capital e.g. by seeking investment in the IC/flash memory division, however, Toshiba seeks to keep control, so Toshiba is trying to raise a minority share, or non-voting shares or similar, in order not to lose control.

How did Toshiba get into a situation to potentially need to write off US$ 6 billion?

Toshiba acquired 87% of the US nuclear equipment manufacturer Westinghouse.

While Westinghouse is a famous name, what Toshiba actually acquired seems to have gone through a period of restructuring.

In 2015 Toshiba acquired the construction company SHAW’s assets from the Chicago Bridge & Iron Company CB&I for US$ 229 million plus assumed liabilities. CB&I had acquired SHAW for US$ 3.3 billion in July 2012, and SHAW has on the order of US$ 2 billion annual sales.

Why did Toshiba acquire a company for US$229 million, which has US$ 2 billion annual sales, and which was in 2012 acquired for US$ 3.3 billion? Which factors reduced the value of this company from US$ 3.3 billion to US$ 229 million within the 3 years from 2012 to 2015?

Presumably because there are large liabilities arising from nuclear construction, which Toshiba now seems to have to assume.

What is likely to happen now with Toshiba? Is Toshiba too big to fail?

Difficult to say what will happen. Toshiba is a huge corporate group with about 200,000 employees and many factories in many countries, so clearly Toshiba is not going to disappear without trace.

The immediate risk is that Tokyo Stock Exchange carries out its warning, and delists Toshiba, which will further increase Toshiba’s ability to raise capital. In the case of a delisting, private equity, and/or government might invest and restructure, and Toshiba might be split up. For example, Toshiba’s nuclear Westinghouse division is totally separate from its very successful flash memory division, there is not much business logic in having both under one holding company.

Impact on UK

Toshiba acquired 60% of UK based NuGeneration with the view to build nuclear power stations in the UK. This project requires Toshiba to contribute to the funding of the nuclear project, for which Toshiba would probably need a financially healthy partner.

What is the big picture? How did Toshiba get into this crisis?

Toshiba’s crisis has been building up for 20 years, and is in my view a consequence of corporate governance issues over a long time.

Essentially, Toshiba should have been reformed 20 years ago from the top down.

Japan’s 8 electronics giants have had essentially no growth and no profits for 20 years. This tragedy has been obvious for many years now, and was a big contributing factor for Japan’s government to reform Japan’s corporate governance laws and regulations, see:

Toshiba’s Board of Directors was exchanged in September 2015, and now includes several very capable and experienced Japanese independent Board Directors, but unlike Hitachi, even today neither Toshiba’s Board of Directors, nor Toshiba’s Executive Board include one single foreigner.

One might think that a huge global group like Toshiba with complex businesses around the globe might benefit from a variety of view points and experiences from different countries at Supervisory Board and Executive Board level – not all just from one single country. Japanese corporations including Hitachi, SoftBank, Nissan and a small number of others are now recognizing the benefits of diversity of experience and viewpoints at Supervisory Board and Executive Board level.

We can only hope that Toshiba’s executives and Board Directors have the experience and ability to solve the extremely complex issues deep inside the bowels of the US nuclear construction industry – far away on the other side of the world.

The global mobile internet revolution started with Docomo’s i-Mode on February 22, 1999

i-Mode, Happy Birthday!

i-mode menu NTT docomo

Today, exactly 17 years ago, on February 22, 1999, NTT-Docomo launched the world’s first mobile internet service, i-Mode, at a press conference attended only by a handful of people.

NTT-Docomo created the foundation of the global mobile internet revolution, and i-Mode is still a cash-cow for Docomo in Japan, but Docomo did not succeed to capture global value.

i-Mode pioneered many business models, which are today monetized by Apple and Google (mainly via Android).

i-Mode also contributed to make Japan the world’s biggest App market in terms of cash revenues, and helped Japanese app companies to be among the world’s largest and top grossing.

the future of Japan’s US$ 600 billion electronics sector, which dominated world electronics in the 1980s but failed to keep up with the evolution and growth of global electronics.

To survive Japan’s old established electronics conglomerates have two choices:

focus on a small number of key products (remember Apple CEO Tim Cook showing that all of Apple’s products fit on one small table)

actively managed portfolio model

however, for Japan’s economy to prosper, Japan needs many more young fresh new companies in addition to the old established conglomerates.

Interviews for BBC-TV and French Les Echos

Last week I was interviewed both live on BBC-TV and also by the French paper Les Echos about SHARP’s future:

In summary, I said that its not just about SHARP’s current predicament, but its about corporate governance reform in Japan, about reinventing Japan’s electronics sector, and that its more likely at this stage that Japan’s Innovation Network Corporation (INCJ) will take control SHARP, since INCJ is not just concerned with SHARP but with the bigger picture of restructuring Japan’s electronics sector.

INCJ has concepts for combining SHARP’s display division with Japan Display, and has plans for SHARP’s electronics components divisions, and for the white goods division, and other divisions.

SHARP governance: How and why did SHARP get into this very difficult situation?

Essentially SHARP assumed that the world market for TVs and PC displays will continue to demand larger and larger and more expensive display sizes, and thus took bank loans to build a very large liquid crystal display factory in Sakai-shi, south of Osaka.

In addition, SHARP, has a huge portfolio of many different products ranging from office copying machines and printers and scanners, mobile phones, high-tech toilets, liquid crystal displays, solar panels, and hundreds of other products. SHARP keeps adding new product ranges constantly expanding its portfolio of businesses, and rarely sells loss making divisions.

Effective and strong independent, outside Directors on the Board might have asked questions during the decision making leading to the building of the Sakai factory. They might have asked for a Plan B, in case the global display market takes a turn away from larger and larger and more expensive displays, or if the competition heats up and prices start decreasing, they might have asked about SHARP’s competitive strengths, they might have also questioned the wisdom to finance an expensive factory via short-term bank loans as opposed to issuing shares to spread the risks to investors.

Its not just outside Directors, shareholders could have also asked such questions.

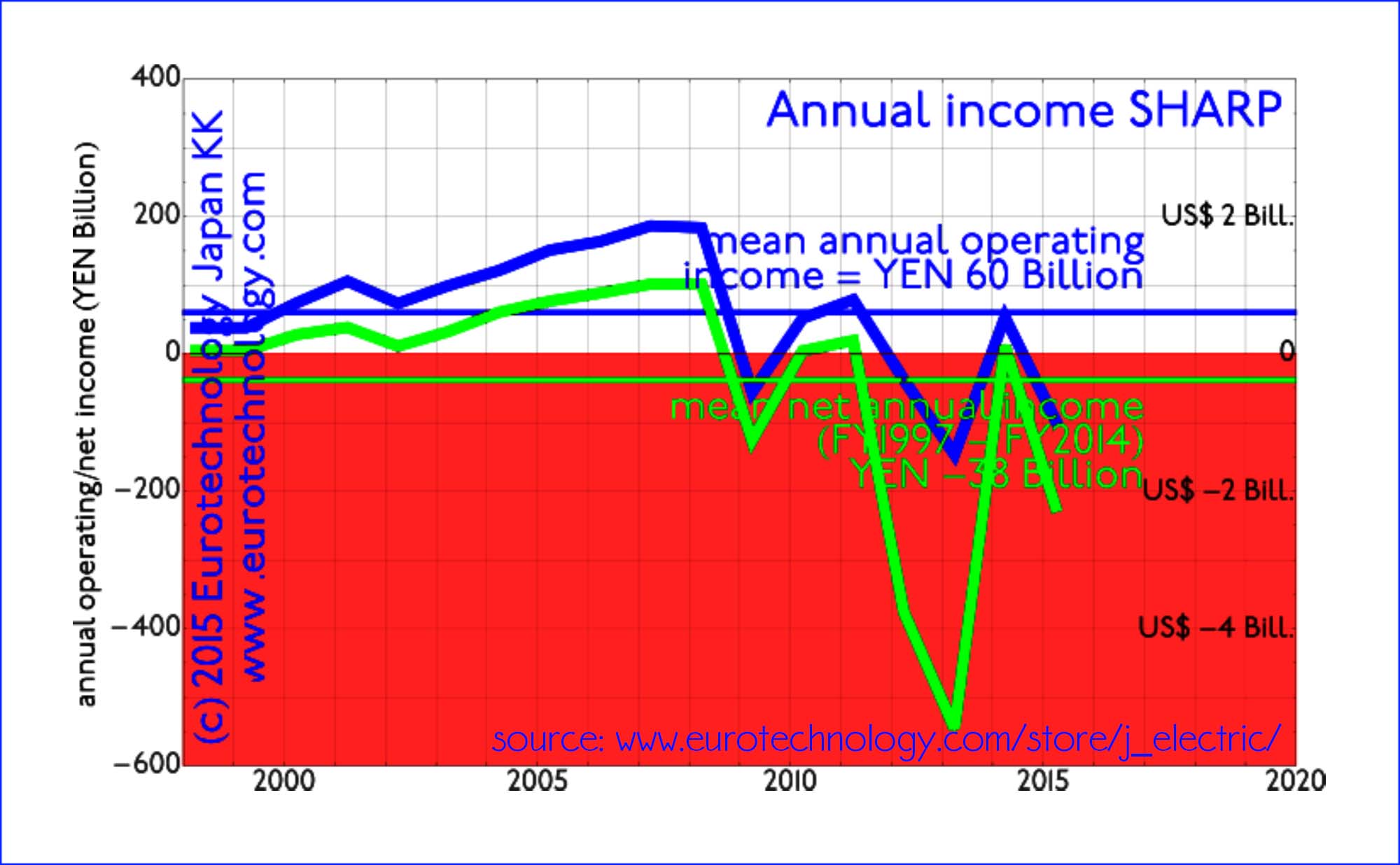

SHARP has about YEN 678 billion (US$ 5.6 billion) debt, most is short-term debt, and in a few weeks, in March 2016, SHARP needs to repay about YEN 510 billion (US$ 4.2 billion), and needs to find this amount outside.

SHARP is a Japanese electronics company, founded in 1912 by Tokuji Hayakawa in Tokyo as a metal workshop making belt buckles “Tokubijo”, and today one of the major suppliers of liquid crystal displays for Apple’s iPhones, iPads and Macs.

SHARP today has about 44,000 employees, many factories across the globe, sales peaked around YEN 3000 billion (US$ 30 billion) in 2008, and show a steady downward trend since 2008.

Revenues (profits) peaked in 2008, and have fallen into the red since.

SHARP’s revenues (sales) peaked in 2008 around YEN 3000 billion (US$ 30 billion), and show a downward trend ever sinceAveraged over the last 14 years, SHARP shows average annual net losses of around YEN 38 billion per year (US$ 380 million per year)

What future for SHARP? Focus vs portfolio company

SHARP (or rather, its creditors, the two “main banks” Mizuho and Mitsubishi-Tokyo-Bank, and others controlling the fate of today’s SHARP) needs to decide whether it focuses on a group of core products, in which case it needs to be No. 1 or No. 2 globally for these products. Successful examples are Japan’s electronic component companies.

Or on the other hand, SHARP could be a portfolio company, in which case this portfolio must be actively managed.

What future for Japan’s US$ 600 billion electronics sector?

combined have sales of about US$ 600 Billion, similar to the economic size of The Netherlands, but combined for about 15 years have shown no growth and no profits. They are poster children for the urgent need for corporate governance reform in Japan.

These 8 electronics conglomerates are portfolio companies, and they need to manage these portfolios actively, such as General Electric (GE) or the German chemical industry are doing. Germany’s large chemical and pharmaceutical industries started active and drastic product portfolio management in the 1990s, and are continuing constant and active portfolio optimization via acquisitions, spin-outs, and other M&A actions, and so is GE.

Why “let zombie companies die” is beside the point

Concerning SHARP some media wrote headlines along the lines of “let zombie companies die”. Thats easy to write, however, SHARP is a group with 44,000 employees, many factories, about US$ 30 billion in sales annually.

“Let this zombie die” is not an option, SHARP has 100s of products, and divisions, and the best solution for each of these divisions is different. And that is exactly what the Innovation Network Corporation of Japan seems to be considering in its plans for SHARP.

I think the way forward is not “to let zombies die”, but to develop private equity in Japan

I think the move of Atsushi Saito, one of the key drivers of Japan’s corporate governance reforms, from CEO of Tokyo Stock Exchange/ Japan Exchange Group, to Chairman of the private equity group KKR is a tremendously important one in this context.

Will there be native Japanese private equity groups with sufficient know-how and ability to take responsibility of restructuring Japan’s electronics sector? Thats maybe the key question.

Why its not really about nationalism

Some media bring a nationalist angle into SHARP’s issues. However, Nissan was rescued by French Renault, UK’s Vodafone acquired Japan Telecom, and there are many other examples, where foreign companies acquire Japanese technology companies.

I don’t think nationalism is an issue here. The key issues is to create and implement valid business models for Japan’s huge existing electronics sector, and more importantly, create a basis for the growth valid new companies – not just reviving old ones.

Economic growth: Almost everyone agrees that economic growth is preferred over stagnation and decline. Fiscal policy and printing money unfortunately can’t deliver growth.

Governments best help economic growth by reducing friction, and by getting out of the way of entrepreneurs building, turning-round, and refocusing companies.

Some required action is counter to intuition: for example, in many cases reducing tax rates increases Government’s tax income, a fact known for many years. Effective education and research are key to create, understand and apply such non-obvious knowledge.

Companies need efficient leadership, leadership needs feedback, wise and diverse oversight by Boards of Directors, who ring alarm bells long before a company hits the rocks, or fades into irrelevance. Corporate governance reform may be the most important component of “Abenomics”. Read a Board Director’s view on Japan’s corporate governance reforms:

Japan’s electrical conglomerates are some of the poster children motivating Japan’s corporate governance reforms. In an interview about Toshiba’s future on BBC-TV a few days ago, I explained that Japan’s electrical conglomerates showed no growth and no profits for about 20 years, and the refocusing Toshiba has announced now should have been done much much earlier, 10-20 years ago (“Speed is like fresh food“). Refocusing Japan’s established corporate giants will release resources for start-ups, spin-outs and growth companies.

Japan can be very good at restructuring and turn-rounds, e.g. see

Corporate governance reforms in Japan are one component of “Abenomics” to bring back economic growth to Japan.

Corporate governance reforms in Japan are driven at least in part by the spectacular stagnation of Japan’s top 8 electronics conglomerates, which 25 years ago dominated world electronics, but largely failed to adapt to the changes driven by much more agile Silicon Valley or South Korea based competitors. The right type of Board Directors, could potentially have rung the alarm bells much earlier, and woken up executive management under their supervision.

A welcome factor is that corporate governance reform costs Japan’s heavily indebted Government almost no money – unlike public works programs, and similar traditional ways of stimulating the economy.

The speed with which Corporate Governance Reforms in Japan are being implemented surprised even one of their main promoters, emeritus Group CEO of the Japan Exchange Group, Atsushi Saito, as expressed in his recent talk.

In March 2014 the shareholders appointed me as independent Board Director of the Japanese cybersecurity company GMO Cloud KK, which is listed on the First Section of the Tokyo Stock Exchange. Our main business are internet security solutions, cybersecurity, digital identity management solutions, and cloud hosting and related services and solutions.

The Corporate Governance Code of the Tokyo Stock Exchange (TSE), issued on June 1, 2015, “Seeking Sustainable Corporate Growth and Increased Corporate Value over the Mid- to Long-Term”

Japan’s Stewardship Code, issued by Japan’s Financial Services Agency (FSA) on February 26, 2014, “Principles for Responsible Institutional Investors ≪Japan’s Stewardship Code≫- To promote sustainable growth of companies through investment and dialogue”

Japan’s Corporate Governance Code, which was issued by the Tokyo Stock Exchange on June 1, 2015, defines Corporate Governance as “a structure for transparent, fair, timely and decisive decision-making by companies, with due attention to the needs and perspectives of shareholders and also customers, employees and local communities”.

The subtitle of Japan’s Corporate Governance Code is its mission statement: “Seeking sustainable corporate growth and increased corporate value over the mid- to long-term”.

Corporate governance has been analyzed in great detail in Professor John Kay’s analysis of UK’s capital markets: “The Kay Review of UK Equity Markets and long term decision making“, which was triggered by certain M&A transactions among other factors, and published on 23 July 2012.

The Kay Review analyzes UK’s capital markets in depth, and argues that its companies’ duty to be successful in the long-term, and its only the success of companies that brings wealth to all stake holders and people who invest in companies, in many cases pensioners. Over the years a fine grained system of specialized service providers has developed between companies on one side, and individual investors on the other side. Professor Kay argues that this system of intermediaries (fund managers, analysts etc) can be seen as “overhead” and needs to be as efficient as possible.

Overall the capital market system needs to be built on long term trust and stewardship, not on anonymous one-time monetary transactions.

Martin Lipton, of the NY law firm Wachtell, Lipton, Rosen & Katz, in an article published on the Harvard Law School Forum on Corporate Governance and Financial Regulation blog encourages the US Securities and Exchange Commission (SEC) to keep the UK developments in mind, when reforming the reporting requirements for US corporations, and also calls for an end to the requirement of quarterly reporting.

Why end the requirement of quarterly financial reports? Because short term focus on quarterly financial performance may cloud the view on long-term success and investment. Intense discussions between fund managers and management are strongly encouraged.

Will the end of quarterly financial reporting reach Japan?

Why Japan’s focus on corporate governance?

GNP as a measure of economic size has many flaws – however many signals, not just GNP, indicate that Japan is the only major economy that does not grow.

While there are many excellent Japanese corporations, overall it is no secret that Japan’s economy has the potential to do much much better.

Japan’s decline was even deplored by Keidanren and Toray Chairman Sadayuki Sakakibara at the 2015 Kyoto Bank New Year Gala event. Stanford Economics Professor Takeo Hoshi has analyzed the factors which caused Japan’s economy to stop growing after catching up with the developed economies, see Professor Hoshi’s recent talk about Abenomics for the Stockholm School of Economics.

There is much hope that outside directors supervising executive management will bring outside expertise, and improve the performance of company-insider executive management, and if necessary also insist on replacements.

The cheapest part of “Abenomics” – corporate governance reform comes at essentially zero cost to tax payers

Many measures of Premier Minister Abe’s “Abenomics” stimulation programs pump borrowed Government Bonds (JGB) money into the economy, thus cost money and ultimately increase Japanese very large Government debt.

By comparison, corporate governance reforms cost essentially zero cash and don’t further increase government debt.

Theory and practice

Non-diversity: about 0.6% of Japanese Board Directors of listed companies are non-Japanese

As of 17 December 2015 Japan has 3504 listed companies on the exchanges operated by the Japan Exchange Group:

TOKYO PRO Market: 14 (including 0 foreign company)

Total: 3504 (including 9 foreign companies)

In addition there are three regional exchanges:

Fukuoka Stock Exchange

Nagoya Stock Exchange

Sapporo Stock Exchange

Assuming there are about 10 Board Directors per company, there are about 35,000 Board Directors of listed companies in Japan. Of these approximately 200 are foreigners, ie. about 0.6% of Directors of listed Japanese companies are foreign (I am one of these).

Maybe 10-20 of Japan’s public companies are “Englishized” such as Rakuten or SoftBank, or hire simultaneous interpreters at Board Level (you’ll see Directors with headphones listening to the interpreted/translated version of what is being said – of course slowing and filtering understanding and communication)

All other approx. 3490 Japanese Stock Exchange listed companies are run 100% in Japanese language at all levels including Board level – and almost exclusively by Japanese men.

In a rapidly globalizing world, these companies desperately need global input from many nationalities, different backgrounds, and genders at Board level in Japanese language, but the number of people providing this depth of diversity, having the qualifications and being able to function at Board level in Japanese in addition to several other languages is severely limited – this is one of several factors limiting Japan’s growth after having caught up with developed countries in the 1980ies.

What are the main issues?

Diversity delivers better decisions and better results

Japan has many outstanding leaders, such as SoftBank’s founder Masayoshi Son, or Kyocera’s founder Kazuo Inamori, who also founded part of today’s KDDI, and who turned around Japan Airlines from bankruptcy in his 80s.

Some Japanese Executives are outstanding leaders, however, many are not, but function more like chief administrators – as in any other country.

Outstanding leaders don’t fear working with excellent people and will attract top leaders. However, chief administrator type executives will fear for their power and will assemble teams who fear to speak out, as can be observed in many recent corporate scandals in Japan, and many other major countries. Corporate scandals and corporate governance failures may happen anywhere, not just in Japan.

Diversity at top management levels and Board levels has many benefits, as has been proven in many studies. Diversity delivers better decisions and better results. Boards of Directors are one way to bring diversity to decision making.

Overcoming stagnation

Many major Japanese corporations show no growth and no income for the last 20 years.

A showcase example are Japan’s top-8 electronics conglomerates. Combined they are as large as the economy of the Netherlands, but contrary to The Netherlands, they have shown no growth for the last 17-20 years, as well as losing money on average over all these years. Of course, as a consequence the market capitalization = value of these top-8 electronics companies has decreased dramatically. While Japan’s top-8 electronics companies dominated 60% or more percent of the global electronics industry in the 1980, they have fallen steep. Clearly a dramatic example of failed corporate governance, and surely a big push for Prime Minister Abe to put so much priority on improving Japan’s corporate governance, together of course with the need to improve employment, and returns for pension funds to fund Japan’s aging population.

Three forms of corporate organization: splitting supervision and execution

Traditionally, executives supervised themselves at Board level

Traditional Japanese corporation have a Board of Directors composed of corporate executives, i.e. the executives supervise themselves without external supervision or input. Supervision is done by the Kansayaku Board (corporate auditor’s Board) which however has limited powers on corporate decision making.

Japan’s corporate government reforms now give Japanese companies options to split execution (executives, 執行役員) and supervision (Board Directors, 取締役).

Japanese corporations now can chose between three forms of organization

company with Kansayaku Board

company with Supervisory Board

company with three committees:

Nomination Committee

Audit Committee

Remuneration Committee

According to the new Corporate Governance Code, the Board (independent which of the three options is selected) has the following three duties:

setting the directions of corporate strategy

encourage and support appropriate risk taking by senior management

supervise Directors and executive management, including senior executives (執行役員)

Connecting the dots: the link between accounting issues and the space shuttle Challenger disaster

Space shuttle Challenger’s top management was insisting to keep the planned launch date fearing public relations issues, while the workers and engineers on the ground, “genba”, knew that they were not ready. But top management at space shuttle Challenger did not listen to “genba”.

My advice to Japanese corporations: embrace and learn to love diversity!

Embrace and learn to love diversity! Diversity delivers better results overall. We all learn from each other.

My advice to foreign investment funds seeking more influence on Japanese companies

Shouting at the CEO or Boards of Japanese companies will not help – many foreign activist investors have already proven this fact many times. Insisting on your superior knowledge will not make you many friends – as anywhere else.

You need to develop trust and relationships. You need to start by learning Japanese, understanding Japan, and earn trust and contribute with achievements, or partner with people who have: KKR hired Japan Exchange Group emeritus CEO Atsushi Saito.

There are no increasing numbers of examples, where outstanding Japanese corporations careful listen to outside advice from investors, and thus become even more outstanding: SONY and robotics maker FANUC come to mind.

My advice to foreign companies operating in Japan

Your subsidiary in Japan is a Japanese corporations and needs corporate governance. There have been a long list of corporate governance failures leading to huge problems and losses at foreign subsidiaries in Japan, in the financial sector, the elevator sector, the pharmaceutical sector and several others.

Make good use of the Board of Directors of your Japanese subsidiary corporation.

Dentsu dominates Japan’s media sector and advertising

Dentsu switches from JGAAP to IFRS accounting standards with big impact on KPIs

Dentsu dominates Japan’s advertising and media industries, and attracts some of the most creative Japanese talent, although Dentsu is not the first advertising agency in Japan – that priority belongs to Hakuhodo.

From April 1, 2015, Dentsu decided to switch to IFRS accounting standards from Japan’s JGAAP standards. For FY2014, Dentsu reports financial results both using IFRS and JGAAP standards, giving us the fascinating opportunity to compare both accounting standards for a major corporation.

So how big is Dentsu? For FY 2014 (April 1, 2014 – March 31, 2015) Dentsu reports (we have rounded the figures):

Net Sales (JGAAP) = ¥ 2419 billion (=US$ 19 billion)

Revenues (IFRS) = ¥ 729 billion (=US$ 6 billion)

For operating income, net income and other data IFRS and JGAAP measure quite different KPIs.

Disruption is on the way: CyberAgent based on blogs, Recruit based on classified advertising and HR, LINE based on sticker communications, and many more…

How big is Dentsu? US$ 37 billion, or US$ 19 billion or US$ 6 billion sales/year?

Managing Japan/West cultural issues via the Dentsu-Aegis-Network

As for many Japanese corporations, Dentsu’s challenge is to leverage a dominating position in Japan into a global business footprint, while managing the well-known cultural issues. Dentsu’s approach was to acquire the French/UK agency Aegis, and then via Dentsu-Aegis acquire a string of agencies all over Europe:

Dentsu dominates Japan’s advertising space, and is a very very strong force in Japan’s media industry sector, through control and management of major advertising channels with an overwhelming market share in Japan, and has been working hard to leverage its creative power and strength in Japan into a larger global footprint.

Only with freedom and democracy, the values of open society and professionalism can the investment chain function effectively

Japan Exchange Group CEO Atsushi Saito: proud of Corporate Governance achievements, but ashamed of Toshiba

The iconic leader of the Tokyo Stock Exchange since 2007, now Group CEO of the Japan Exchange Group gave a Press Conference at the Foreign Correspondents Club of Japan on June 12, 2015, a few days before his retirement, to give an overview of his achievements and to review the status of Japan’s financial markets today.

Atsushi Saito expresses his satisfaction and pride and surprise about the big improvements in corporate governance and the mind change happening in Japan now.

Atsushi Saito has worked as equity analyst in the USA, experienced the US pension fund debate, and when he was pushing for reform of corporate governance in Japan around 1990 was ignored or even criticized. He is surprised to see that these changes he has been keeping pushing for since 1990 are actually implemented now.

Atsushi Saito directly expressed his shame about the accounting problems recently revealed at Toshiba, and contracts Hitachi, which has independent outsiders, women and non-Japanese foreigners on the Board of Directors, with Toshiba which has not. Atsushi Saito directly said: “I am very puzzled why Toshiba is so lazy to check their accounting”.

Atsushi Saito – leading the Tokyo Stock Exchange since 2007

Leading the Tokyo Stock Exchange since 2007, Atsushi Saito aspired to create an attractive investment destination in Tokyo for investors from all over the world with the following achievements:

modernized the trading systems

developed a self regulatory body

merge with Osaka to create Japan exchange group

Reform corporate governance to improve capital efficiency and corporate value of Japanese companies

The most imperative challenge has been left untouched for far too long: reform of corporate governance in Japan to improve capital efficiency and corporate value of Japanese companies.

Recently we introduced the Corporate Governance Code and we see a shift of mindset in Japanese companies.

Structural impediments remain remain in Japan’s financial market

Structural impediments remain remain in Japan’s financial markets, indirect finance from Banks remain a significant force in corporate finance.

Japanese investment bankers continue to fall way behind European and US rivals.

The post financial crisis regime under Basel 3 puts breaks on excessive leverage.

When global economy returns to high growth, we are not able to rely solely on money centered banks – banks will not be able to provide enough capital satisfy demands in a growing world economy.

Foresee demands for international organizations WorldBank, ADB and new AIIB and private equity funds.

With FinTec, we expect unbundling across separate financial service lines

With fintec, combining financial services and technology, we expect increasing unbundling across separate service lines for banking services, between settlement, wire transfers, loans and other services.

We will see more financial services.

Over dependence on main banks, risk aversion, lack of sense of duty by corporate managers led to the death of Japanese equity as an asset class

In Japan, as a consequence of dependence on indirect finance by money centric main banks, deep involvement of the main banks in corporate management, Japanese companies grew increasingly risk averse shied away from dynamic investment, and ultimately damaged corporate value.

There was a demise of the sense of duty by corporate managers use equity capital efficiently, and as a consequence of these factors, we saw a global divestment from Japanese stocks, eventually leading to the death of Japanese equity as an asset class.

Pushing since 1990 for reform of corporate governance in Japan, Atsushi Saito was not only ignored but even criticized

Atsushi Saito working as an equity analyst in the USA, followed the US pension debate, and started to push for reform of corporate governance in Japan around 1990, he was not only ignored but criticized.

Japan’s recent miraculous turn on corporate governance took Atsushi Saito by complete surprise

Today Japan addresses corporate governance, there is a miraculous turn of mindsets and regulatory framework. We saw:

amendment of companies act

corporate gov code

stewardship code

That these changes could happen came as a complete surprise.

Atsushi Saito hopes that this momentum can be maintained, and fiduciary duties of pension fund managers towards beneficiaries will be strengthened to nurture greater professionalism among Japanese institutional investors, similar to The Employee Retirement Income Security Act of 1974, or ERISA act in the USA.

Only with freedom and democracy + values of open society + professionalism can the investment chain function effectively

Only with freedom and democracy, the values of open society and professionalism can investment chain function effectively. This pattern is what defines truly advanced economy

The recent transformation has brought Japan back into the focus of professional investors globally and a new dawn beckons for Japan.

All stakeholders must remain focused to follow through these early signs of change to ensure that Japan welcomes a brighter future.

Questions and answers

Q: Japan not joining the Asian Infrastructure Investment Bank (AIIB) will deprive Japan of opportunities?

A: The Japanese Government did not say that it will not join the AIIB, but today there is no clear set of rules for the AIIB, the governance structure is unclear. To use tax payers money our government needs to be prudent before they make a decision on investment. There are about 20 international banks and similar organizations, 19 of them have clear governance rules. All except AIIB have clear governance rules. In case of AIIB China will have about 30% holding. Probably our Government will wait before making a decision, and Atsushi Saito thinks this is reasonable.

Q: Will Tokyo Stock Exchange enter into international alliance?

A: Stock Exchange business is a very nationalistic business – only USA has multiple exchanges. All other states have one single Exchange totally under control, regulations, culture by single states. Theoretically Exchanges between different countries can merge, but none succeeded. We saw no case in the world were Exchanges from different countries merged successfully, all such cooperations failed.

Q: Plans of Toyota to have non-traded convertable shares?

Its up to their shareholders. Legally they did not violate any rule.

Japan does not have any priority on special stocks.

I see a discrepance in the USA: The US aggressively raises the voice for rights of shareholders, and corporate governance elsewhere. At the same time US companies are the largest issuer of special stocks for special owners, e.g. for Google or Facebook, more than 50-60% of voting power is dominated by the founders of these companies. –

I see a discrepancy, its an ironical discrepancy. I am talking to the leaders of US : US is very nosy about our corporate goverance, protection of shareholders, but how do they protect shareholders of Google or Facebook?

Q: What is your advice for Japanese economy to regain vitality and energy, for Japan to become No. 1 in the world?

A: I am very concerned about efficient capital use and corporate governance. When I was securities analyst in USA, I was always asked about financial data of Japanese corporations.

Fuji Film had huge cash on the balance sheet – their competitor, the yellow-color photo company was always diligent with share holders, paid dividends, did share buy-backs. Fuji spent much R&D on pharmaceuticals and diversification. The Yellow color photo company disappeared, and Fuji Film is very healthy. Accumulation of sleeping capital is useless. But efficient use of capital is crucial.

when GM went bankrupt it was discovered that they had great technology, like electrical car projects which had been stopped. GM had stopped these R&D projects, because shareholders had insisted to stop R&D spending, and pay hire dividends, and ultimately went bankrupt.

Toyota had 3 trillion yen cash. This was heavily criticized. Toyota was secretely developing electric cars – now LEXUS electric car is bestseller in USA.

We are concerned to respect shareholders, but shareholders’ short term wishes are not always best for the company.

Even BlackRock wants long-term enterprise development rather than short term cash benefits.

Q: Impact of weak YEN on Stock Exchange

A: Even with weak yen, our trade balance is negative. Yen rate is not pushing export from Japan. Japan is manufacturing outside of Japan. Trade account is negative, capital account is black, currency account is black. Overseas subsidiaries are sending dividends back to Japan at the yen rate of 120. Its smart return in the capital account. Our industry structure has changed, we are not exporting on the back of weak yen, so we are not criticized.

Q: plans after retirement

A: I decided: no job – I will take rest.

Q: Disclosure. Often financial data are exposed early in Nikkei or Japanese press prior to official disclosure.

A: I am often asked about this. I don’t know how the press gets their information, its a free market for the press. As long as they don’t do any insider trading or use this information privately, I don’t see anything wrong with early public disclosure. Its a competitive issue between journalists, we cannot critisize competition among journalists. Very sharp journalists pick up information, we are not the police we cannot stop them. Its a competitive world – even for journalists.

I live far outside from Tokyo, sometimes journalists wait at the door to my home in the suburbs. I think this is an invasion of my privacy, and I don’t tell them information at my home.

Q: Trust in the stock market, low Japanese retail investor participation.

A: Advanced states have 60-70% own domestic investors, not outside foreign investors.

Foreign professional investors have immediately responded to the logic of our corporate governance reforms. Especially US and UK pension managers have immediately responded to the improved efficiency of our markets. Investment professionals in London, New York, Scotland can evaluate the meaning of our regulatory changes.

Japanese professional or private investors could not understand the improvements we have done, they did not react.

Mutual funds however are at record hights and we have 8 million ELISA private pension investments in Japan now. People start to build their own pensions now, so retail investors are coming into the market.

We have a normal quiet market now here in Japan regarding sales of equities.

Q: Tokyo as a financial center?

A: If you ask the same question to London, they will say that with IT all transactions are global. There may be arbitrage on the prices. If you compare Shanghai and NY, the trading volume in Shanghai is higher than in NY, but Shanghai not a global financial center, because they are not liberalized in capital in and outflow, they are No. 1 only in volume.

The definition of Financial Center of the World has changed.

We want to be one of the better places in financial business globally. We want to offer convenient and friendly conditions for financial people to come to Tokyo, as one of the centers for financial business.

Tax plays a very important role to define financial centers. London or NY or Tokyo cannot follow a city state like Singapore. We cannot have the same tax system. Tokyo is far bigger than Singapore.

“Global financial center” is a vague subject for me.

Q: Do current prices accurately reflect corp performance. Foreign investors: speculative short-term gains? will foreign investors pull out when Bank of Japan money flush ends?

A: I don’t think the Japanese market is overheating at all. I think the short term speculators have already left Japan.

Long term investors have long asked for change in Japan, Japan did not listen, but now for the first time Japan is listening and changing, and I am feeling longterm investors are understanding this change. We have long term investors here now in Japan.

Q: is high-frequency trading a danger for Stock Exchange?

A: Flash Crash in US was due to the diversity of exchanges. There are 50-60 markets in US. Flash Crash artificially made, not becaue of speed of trading.

Our rules for pricing system here in Japan, we learnt this since the Edo era, we cannot have flash crash, we limit the price changes, we are cooling the trading. Our system of pricing is different than in the USA.

We have many high-frequeny traders from abroad, and they appreciate our system. US high frequency traders critized us up to 10 years ago, but today they appreciate our pricing system here in Japan, they want to learn our Stock pricing system. This has really been a big change for us.

Q: False accounting at Toshiba. Impact on trust in Japan’s stock market.

A: I feel very ashamed for Toshiba. Toshiba should be the mentor or leader of Japanese industry – not the opposite.

Hitachi is a huge contrast to Toshiba. Hitachi aggressively introduced outside board members, foreign and women board members. Hitachi is investigated by outside and foreign board members.

Toshiba is a total contrast to Hitachi.

I am very puzzled by that – why is Toshiba so lazy to check their accounting.

We hope that auditors and accounting houses are more professional and more serious. They told us that their subsidiaries have different accounting system. They must have intentionally checked that point.

My answer: my feeling is one of shame. We should definitely not repeat this type of thing.

Q: Why do Japanese company accumulate so much cash reserves.

A: One reason is that Japanese labor laws compel Japanese companies to have reserves to pay for restructuring. We introduced changes in corp governance, and many companies now use the cash for M&A to acquire foreign companies, or e.g. Fanuc has increased dividends.

I am optimistic for Japanese companies, because they are using cash more efficiently now.

The trick of course is the third arrow, the reforms. Read what Professor Takeo Hoshi has to say about Abenomics, Japanese economist, who has worked his way up US Universities, and has now reached the position of Professor of Economics at Stanford University. By the way, here is my talk at Stanford University – some years ago, but much of it still applies today.

Japanese people’s views on nuclear power are polarized, and its unclear and unpredictable when nuclear power stations will be switched on again in Japan. Read what the Governor of Niigata Prefecture has to say, who hosts the world’s largest nuclear power plant with 7 reactors and 8 GigaWatt capacity.

According to the Japanese Energy Fundamental Law, the Government has to publish an official Energy Basic Plan at regular intervals. You can read the 4th Energy Basic Plan published on April 11, 2014, and listen to a commentary on it for The Economist here on YouTube. The 4th Energy Basic Plan starts with the assumption that Japan is poor in natural energy resources, which of course is only true if we restrict “natural energy resources” to fossil resources. Japan is actually potentially very very rich in renewable energy sources, as the scenario plans developed by Japan’s Industry and Economy Ministry (METI) and Japan’s Environmental Ministry show.

Foreign companies in Japan, and Japanese companies overseas face a dilemma: expensive expatriates with limited local know-how, or local management? Japanese companies seem to have finally reached the conclusion that Japanese managers eg sent to Germany are in most cases not the best choice to lead a German-based multinational company – here are some great recent examples:

Docomo acquires a majority stake in net mobile AG, however net mobile AG remains a publicly listed company. Read details here.

NTT DATA acquires SAP solution provider itelligence AG, however itelligence AG remains an independently managed company under the founder’s management, and grows aggressively via acquisitions all over the globe. Read details here.

NTT Communications acquires a majority of Integralis, Integralis is renamed NTT Com Security AG, however NTT Com Security AG remains traded on the m:access market of the Munich Stock Exchange. Read details here.

Carlos Ghosn is very well aware of such multi-cultural management issues and how to solve them, however too many EU companies in Japan are not. If they were, EU investments in Japan could be at least 50% higher – as you can read here.

Free Trade Agreement (FTA) and Economic Partnership Agreement (EPA)

Preparations:

EU Japan FTA trade negotiations initiated: At the 20th EU-Japan Summit of May 2011 the EU and Japan decided to start preparations for both a Free Trade Agreement (FTA) and a political framework agreement (Economic Partnership Agreement, EPA).

May 2012: after one year of discussions, the EU agreed with Japan on an agenda for future negotiations covering market access.

On 18 July 2012, the EU Commission asked the EU Member States for agreement on opening Free Trade Agreement negotiations with Japan.

On 29 November 2012, the Council authorized the Commission to start trade negotiations with Japan.

The EU Japan FTA trade negotiations were officially launched on 25 March 2013 by EU President Jose Manuel Barroso, President Herman Van Rompuy and Japanese Prime Minister Shinzo Abe.

Impact Assessment of EU Japan FTA Free Trade Agreement, 18 July 2012 (pdf file)

In business the first-comer does not always win the game

Japan’s NTT-Docomo tested two types of wallet phones, manufactured by Panasonic and SONY with 5000 customers between December 2003 and June 2004, and introduced mobile payments and wallet phones on July 10, 2004 – over 10 years ago.