Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

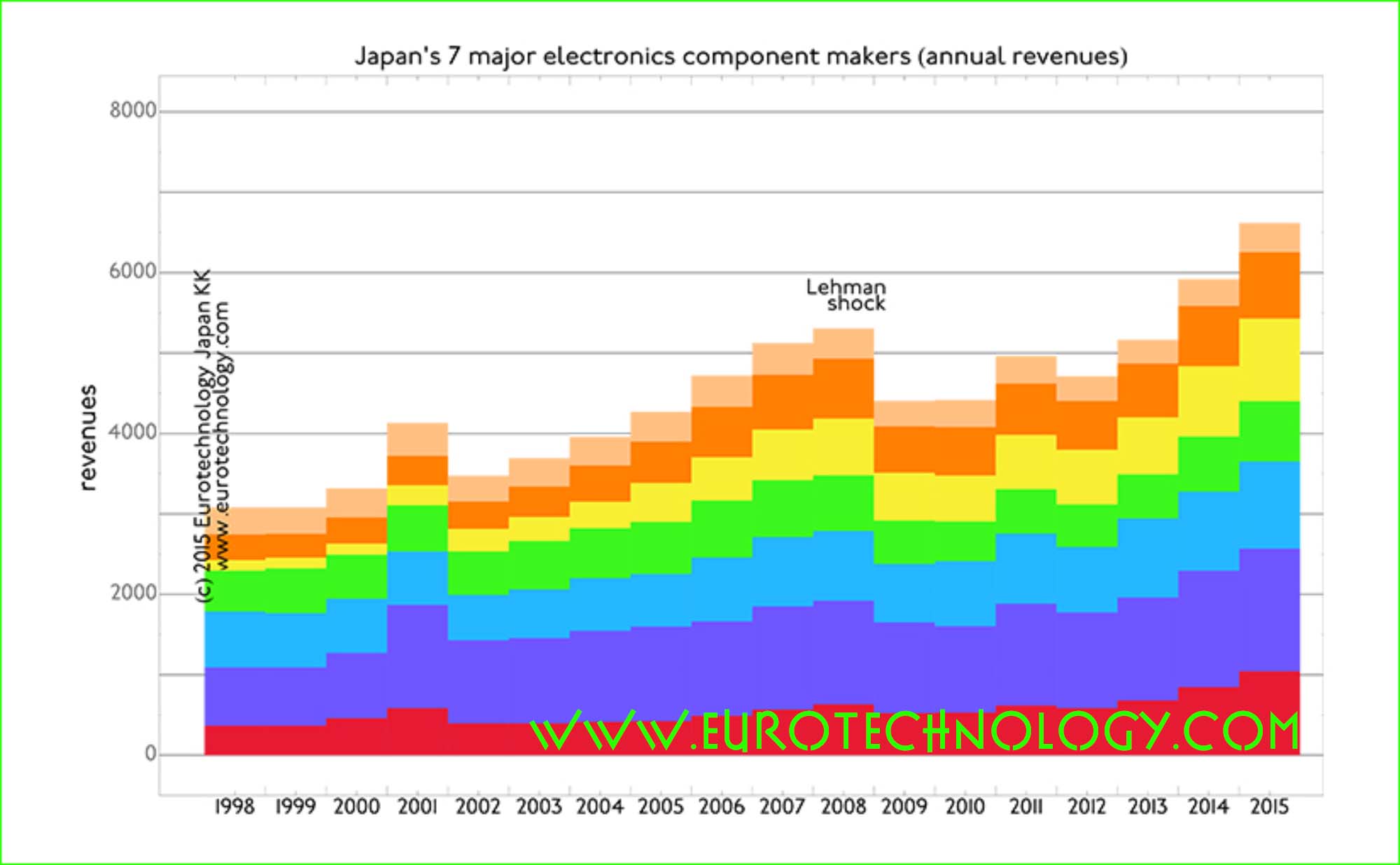

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

Nokia strengthens No. 1 market position in Japan’s mobile phone base station market!

Japan’s mobile phone base station market

Japan’s mobile phone base station market is about US$ 2.6 billion/year and for European companies Ericsson and Nokia the most important market globally, although certainly also the most difficult one.

Nokia is No. 1 with a 26% market share, and Panasonic is No. 5 with 9% market share.

European investments in Japan

Nokia acquiring Panasonic’s network division is one of many investments and acquisitions in Japan by European companies. For more details, see the EU-Japan M&A register.

Panasonic to focus on core business, Nokia to expand market share in Japan

Panasonic, after years of weak financial performance, is focusing on core business. Nikkei reports that Panasonic is planning to sell the base station division, Panasonic System Networks, to Nokia.

Succeeding in Japan at the second try, learning from initial failure:

We see a pattern here: after failing spectacularly trying to build a mobile phone business in Japan for almost 20 years without success, Nokia is now winning the second time round.

It can be hard for foreign companies to build a business in Japan, and many fail. Interestingly, there is a long list of famous companies that succeed on their second attempt after initial failure, this list includes:

IKEA: failed first time in 1974, succeeds now

DAIMLER: failed spectacularly first time with Mitsubishi Motors, now successful with Mitsubishi Fuso trucks – read the time line here

NOKIA: failed first time after trying for 20 years (1989-2008) to sell mobile phones in Japan, now successful with mobile phone base stations and network infrastructure

Our analysis of Japan’s mobile phone base station market shows, that Nokia became No. 1 in Japan’s base station market with the acquisition of Motorola’s base station division. Acquisition of Panasonic System Networks will expand Nokia’s NSN to expand market leadership in Japan’s mobile phone base station market.

I believe without success in Japan’s mobile phone base station market, there is a big chance Nokia as a company, or at least Nokia’s NSN division would not exist any more at all today.

With a market share of 26%, approx. US$ 700 annual sales in Japan, Nokia is No. 1 market leader in Japan followed by Ericsson on 2nd position. With the acquisition of Panasonic’s base station division, Nokia should be able to expand its market share beyond 26%+9% = 35% and expand its leadership, especially via Panasonic’s deep relationship with Docomo.

Because Docomo with its very deep pockets, is traditionally the first globally to develop and bring to market the most advanced radio technologies, a deeper relationship with Docomo will also help Nokia to develop and bring to market new communication and radio technologies. Thus I believe the impact on Nokia will be far more than an increase of the market share in Japan from 26% to 35%.

Panasonic System Networks

Panasonic System Network’s market share is estimated at around 9% of Japan’s mobile phone base station market, while international sales are essentially non-existent. Thus Panasonic System Network’s global market share is negligible, giving Panasonic little possibility for the scale necessary to operate a stable profitable longterm base station business.

Japan’s mobile phone handset makers and base station makers have for many years focused on serving Japan’s internal market only, and in particular have focused on Japan’s No. 1 mobile phone operators NTT Docomo. This gave Japan’s mobile phone base station makers a temporary home advantage, however with the value shift from hardware to software, they lack scale, and are subsequently uncompetitive globally. More about Japan’s Galapagos effect here.

Over the last 15 years since 1998, Panasonic has shown no growth in revenues, and average net losses of YEN 85 billion (US$ 0.85 billion) per year, as typical for most of Japan’s top 8 electronics companies and as we analyze in detail in our report on Japan’s Electronics Industries.

Panasonic is on 5th rank with about 9% market share in Japan’s mobile phone base station markets, and has little chance and not the capital to scale its base station and mobile phone businesses globally. For Panasonic in it’s current very limited financial situation, focus on core business areas is very prudent.

The context: EU investments in Japan

While Japanese investments in Europe are booming, recently European investments in Japan have been stagnating after Vodafone’s withdrawal from Japan, and there are very few new European investments in Japan. Could it be that Nokia’s investment in Japan starts a new trend of renewed European investments in Japan?

Understand Japan’s telecommunications markets

Report on Japan’s telecommunications industry

(approx. 270 pages, pdf file)

TowerJazz acquires three of Panasonic’s large written off wafer fabs for around US$ 100 million

Massive market entry to Japan for TowerJazz

Nikkei (the world’s biggest business daily, see our J-Media report) reported as their top headline yesterday, that TowerJazz is planning to acquire interests in three of Panasonic’s reportedly largely written-off semiconductor fabs valued at about US$ 100 million.

Nikkei reports that Panasonic plans to spin out three fabs into a separate company, to be owned 51% by TowerJazz and 49% by Panasonic:

Uozu-shi in Toyama-ken (富山県魚津市)

in Tonami-shi in Toyama-ken (富山県砺波市), and in

Myoku-shi in Niigata-ken (新潟県妙高市)

TowerJazz entered Japan’s market by acquiring the Nishiwaki semiconductor fab near Nishiwaki-shi in Hiyogo-ken near Kobe.

TowerJazz is a leading Israel-USA foundry company traded on NASDAQ. TowerJazz in 2011 acquired a semiconductor fab in Nishiwaki-shi in Hiyogo-ken (兵庫県西脇市). The Nishiwaki fab was initially built by a joint-venture between Texas-Instruments and Kobe-Steel, and was later acquired by Micron. TowerJazz acquired the Nishiwaki-fab from Micron in 2011.

We believe that the driver for these transactions are both PUSH and PULL:

PUSH:

Panasonic’s need for capital

Panasonic’s need to withdraw from loss-making operations (Panasonic’s semiconductor operations reported YEN 20500 million (US$ 200 million) operating losses for revenues of YEN 184 billion YEN (US$ 1.8 billion) and need to focus on a smaller number of core businesses

need for investments in the semiconductor fabs to upgrade equipment and Panasonic’s difficulties to supply such capital

In the past Matsushita (Panasonic was previously named after its founder) was nick-named “Matsushita Bank” because of its solid financial situation. However on October 31, 2012, President Kazuhiro Tsuga announced that “Panasonic is an unusual company” referring to Panasonic’s financial predicament: Panasonic had reported YEN 754.2 billion (US$ 7.5 billion) net losses for FY2012 (ending March 31, 2013). At the same time, President Tsuga also announced a program to revive Panasonic. This event is known as the “Panasonic shock”.

Moving semiconductor fabs from Panasonic to TowerJazz management or co-management/co-ownership is a good example of how Japanese management can be globalized.

Japan’s electronics giants: as large as the economy of Holland, but 17 years of stagnation. No growth & no profits.

Daniel Loeb: SONY’s uninvited guest gives Japan’s business culture a jolt

Japan’s electronics giants combined are as large as the economy of Holland, but did not grow for about 17 years, and on average lost money all these years: no growth – no profits.

SONY abruptly created global headlines (e.g see New York Times), because US activist investor Daniel Loeb publicly encourages SONY’s CEO to speed up change. Mr Loeb’s Third Point LLC fund is SONY’s biggest shareholder at this time – surprising many, maybe even surprising SONY’s CEO, Mr Hirai. Mr Loeb’s encouragement was well timed: Mr Hirai’s will present SONY’s new strategy on May 22.

As we analyzed in our newsletter a few days ago and in more detail in our Electronic Industry Report, which was picked up by EE-Times and by the BBC, SONY recently earns its income, and offsets losses from the electronics and mobile phone businesses, mainly from asset sales and from subsidiary SONY-Finance – which sells life-insurance and credit cards. Therefore many believe that iconic SONY is undervalued, and needs much deeper and more fundamental change.

Japan’s iconic Big-8 electronics giants posses amazing technologies and engineers. However, their current situation is very much less than amazing, indicating huge opportunities. A few days ago the Big-8 all announced their results for FY2012, which ended on March 31, 2013 – lets look at the results together here.

long slow path to recovery for Japan’s “Big-8” electronics giants

Japan’s electronics giants: Averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year

Subtracting losses from profits, and averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year (US$ 1 Billion losses/year)

For the last two financial years the Big-8 created net losses as follows:

Financial Year ended combined net losses

FY2012 March 31, 2013 YEN 1143 Billion (US$ 11 Billion)

FY2011 March 31, 2012 YEN 909 Billion (US$ 8.9 Billion)

Hitachi’s smart transformation

Hitachi’s smart transformation (find an overview in our report) indicates that change can bring rapid improvement.

Japan’s “Big-8” electronics makers combined are about the size of Holland’s economy – with one difference: Holland’s economy grows, but Japan’s electrical giants shrink and lose money at the same time

No growth

No growth: combined revenues of the Big-8 fell by YEN 1510 Billion (US$ 15 Billion) in the 15 years between FY1997 and FY2012 (assuming constant value YEN)

Many expect that “smart transformation” and globalization, and opening-up to the global society – combined maybe with a rejuvenation of “the Japanese model”, can release the potential for growth, which has been held back for 15 years.

In our electronic industry report we compare the Big-8 electronics companies with the Big-7 electronic parts manufacturers and show that their situation is much better, however the parts manufacturers face decreasing margins, also indicating the need for changing the business models and/or operations.

Japan’s “Big-8” may be seen as undervalued

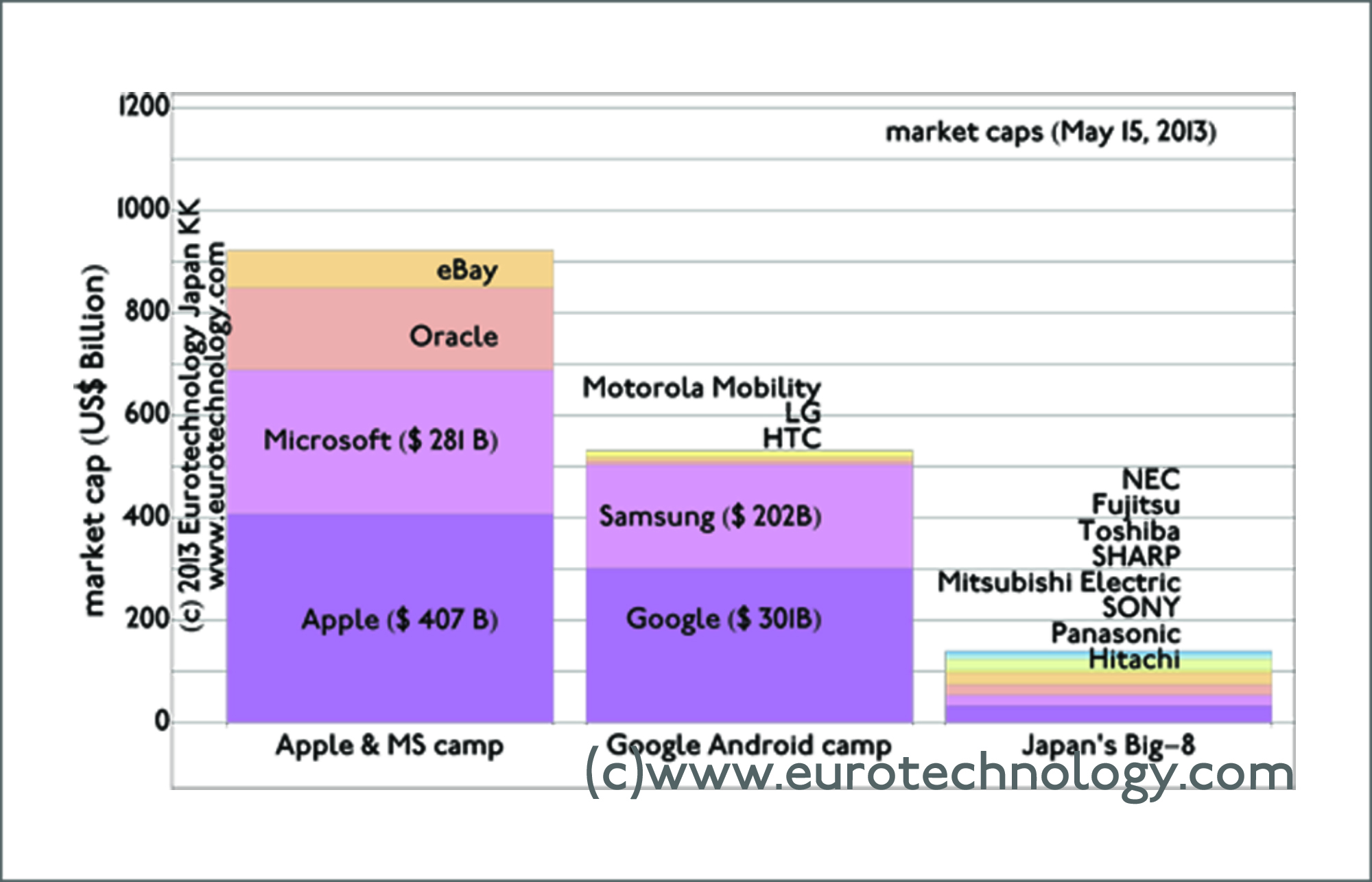

Japan’s Big-8 electronics makers combined have far lower market capitalization than Apple, Microsoft, Google or Samsung

We produced the figure above for the presentation at the Foreign Correspondents Club in Tokyo about the “Apple-Samsung Patent War and Impact on Japans Industries”. We used the figure above to visualize the might of the Apple and Google/Samsung camps vs Japan’s Big-8 today. 15 years ago, the power of Apple vs Samsung vs Japan’s Big-8 was exactly opposite.

There is no reason why Japan’s electronics sector cannot regain global strength and value – IF absolutely necessary changes are made. This situation represents outstanding opportunities, which no doubt are attracting Mr Loeb and his Third Point fund, and others.

Understand Japan’s electronics sector: top 8 giants, and top electronic component makers

Study our report “Japan electronics industries: mono zukuri” (approx. 230 pages, pdf file)

Japan’s top 8 electronics companies combined are as large as the Netherlands economically, but have shown zero growth and zero income over the last 14 years – thus represent “sleeping giants” – or dinosaurs, depending on the point of view, and depending on whether these companies succeed to reinvent themselves.

We have updated our report on “Japan’s electronic manufacturers: mono zukuri” to analyze Japan’s electronics manufacturing sector, and to explain who the winners and who the losers are. Read a short summary in this newsletter below.

apan’s electronics companies combined are as large as Holland economically

Japan’s top electronics companies combined are as large as the Netherlands economically, but have not shown any revenue growth over the last 14 years

Japan’s electronics sector still today is largely guided by national industrial policy, and by the management principles created long ago by charismatic founders such as Matsushita and Ibuka.

Intellectual Japan: smart transformation at Hitachi led by the CEO and by the Chief Transformation Officer CTrO

Hitachi’s “Chief Transformation Officer” (“CTrO”) at a recent presentation, explained that until 2 years ago Hitachi benchmarked its financial data purely domestically – until 2 years ago, Hitachi only compared performance with competitors such as Panasonic and Toshiba.

Only 2 years ago, Hitachi started to benchmark performance with global competitors such as GE and Siemens.

Japan’s top 8 electronics companies combined lose YEN 50 billion/year since 1998

Japan’s top 8 electronics companies lost an average of YEN 50 billion/year over the last 14 years

Intellectual Japan: electronic component makers

Japan’s electronics component makers, such as Kyocera or Murata, which is on the official supplier list of Apple, report positive income – although margins are declining and the component industry sector is much smaller than the top 8 electronics manufacturers.

Drastic transformation is necessary to revive Japan’s electronics industry sector. Drastic change will happen one way or another and represents important opportunities. More details in our electronics industry report

Over the last 15 years, their combined annual sales growth was zero, and their combined annual loss was YEN 50.6 billion/year (= US$ 0.6 billion/year).

Compelling evidence that new business models for Japan’s electronics sector present a huge opportunity – as explained in this BBC interview.

Sales growth of Japan’s “Big-8” electrical manufacturers vs top 7 electronics component makers

Contrasting Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC) with Japan’s 7 electronic parts makers (Murata, Kyocera, TDK, Alps, Nidec, Nitto, ROHM)

Over the last 14 years since FY1997, the combined growth in revenues (=sales) of Japan’s “Big-8” electronics groups was zero. The compound annual growth rate (CAGR) of Japan’s top 7 electronic parts makers combined was +3.1%.

Net income/losses of Japan’s “Big-8” electronics giants vs top-7 electronics components makers

Net income (profit) of Japan’s “Big-8” electronics groups vs top-7 electronics parts makers

Over the last 14 years since FY1997, Japan’s “Big-8” electronics groups combined showed average losses of YEN 50.6 billion/year (=US$ 0.6 billion/year), while Japan’s top 7 electronic parts makers combined earned YEN 196 billion/year (= US$ 2.4 billion/year).

Net income/losses of Japan’s top electrical groups

Net after tax income of Japan’s “Big-8” electronics groups

This figure shows net after tax income for Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC), for the years since FY1997. For 5 of these 14 years the industry sector reported combined losses, which in total exceeded the profits achieved in good years. As a result, averaged over all 14 years, the industry sector shows combined losses on the order of US$ 0.6 billion/year.

Creating new business models for this very large industry sector (of similar economic size as the Netherlands) is a huge opportunity.

et income/losses of Japan’s top-7 electronic component makers

Net income of Japan’s top 7 electronic parts makers

Japan’s top 7 electronic parts makers are in a much better financial situation than Japan’s electrical groups.

Over the last 14 years since FY1997, this industry sector only showed a net overall loss one single time – in the year following the Lehman shock, but showed combined net profits during all other years, resulting in average annual net profits on the order of US$ 2.4 billion/year.

BBC interview: “New business models for Japan’s electrical groups needed”

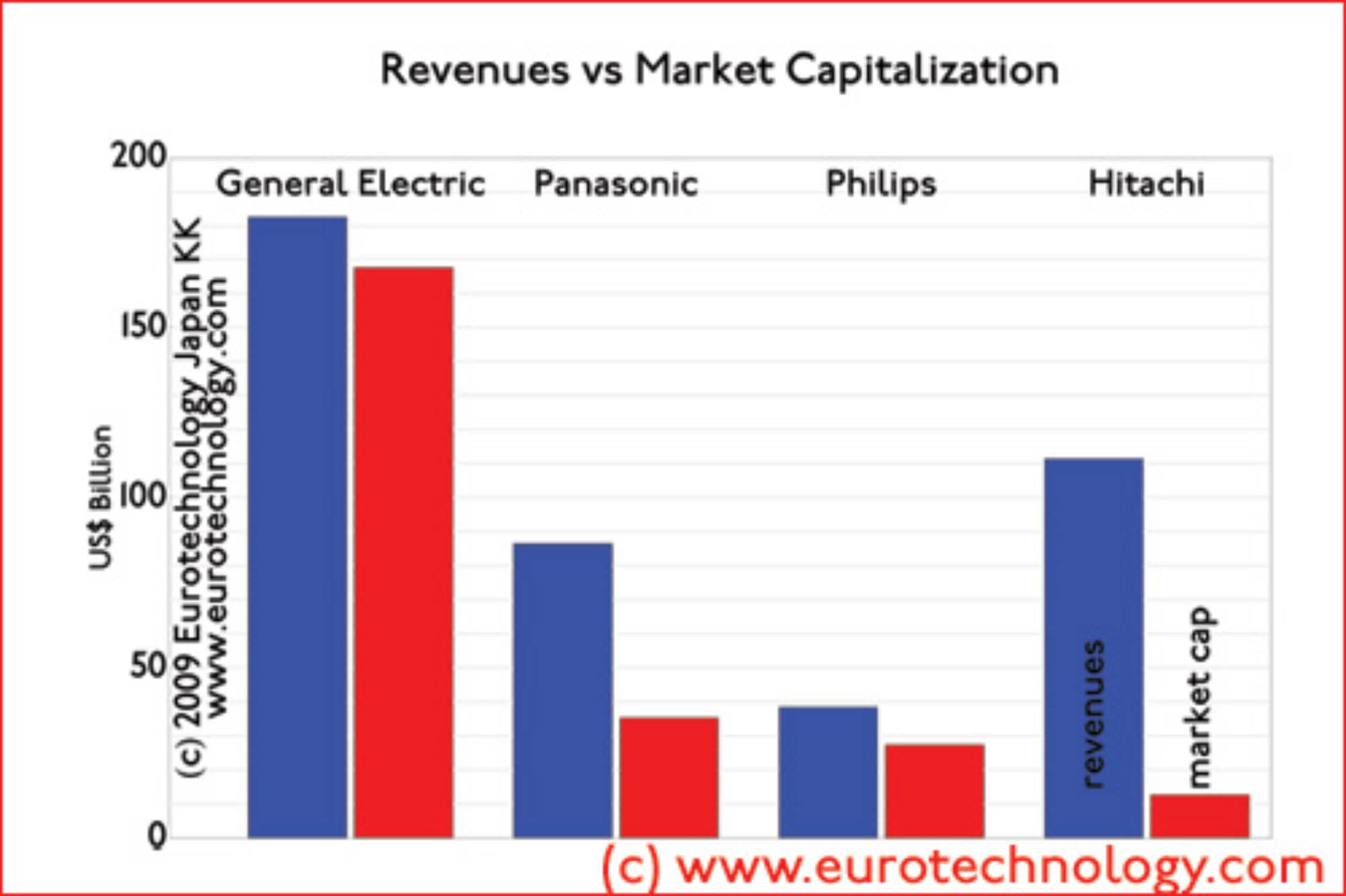

Japan’s electronics giants market caps are remarkably low

General Electric’s market cap is about 13 times higher that of Hitachi

Some of Japan’s electrical corporations have remarkably low market capitalizations: General Electric has 1.6 x more sales than Hitachi, but has 13.3 x the market capitalization. Philips has 1/3 x Hitachi’s sales, but has 2.2 times higher market cap.

Low market values do not help big recent public share offerings: Hitachi raising YEN 250.7 Billion (US$ 2.8 Billion), Toshiba raising YEN 298.7 Billion (US$ 3.3 Billion), and NEC raising YEN 115.5 Billion (US$ 1.3 Billion).

Low valuations increase the pressure for change in Japan’s electrical sector, and the SANYO-Panasonic merger is an indication of changes to come.

In the “post-Galapagos committee” we are working with some of Japan’s brightest leaders on understanding the reasons and on how to drive this change.

Benchmarking Japan’s electrical companies – Philips= 1/3 x Hitachi’s sales and 2.2 x Hitachi’s market cap:

GE= 1.6 x Hitachi’s sales and 13.3 x Hitachi’s market cap

Japan Galapagos effect: “Why do Japanese companies make so beautiful mobile phones with fantastic functions, and have almost no global market share?”

I asked this question back in 2003 to NTT-DoCoMo’s CEO Dr. Tachikawa (see my article “Leadership questions of the week” in Wallstreet Journal of June 12, 2006, page 31), and offered several proposals to Dr. Tachikawa, of which he accepted one.

A related question is: “why can Samsung, LG and Apple beat Japan’s initially far more advanced mobile phone makers, and why have Japan’s phone makers taken no effective action to build global business in order to avoid extinction?”

Now six years after my initial presentation to DoCoMo’s CEO, I have been invited as the only non-Japanese to work on Japan’s “Post-Galapagos Committee”. For most of this year our small group of industry CEOs, academics, government officials and other leaders have been working on understanding the reasons for Japan’s “Galapagos effect” and how to overcome it.

The “Galapagos effect” has not been created by a single factor. Instead a collection of choices by the management teams of Japan’s electrical conglomerates have prevented leverage of their domestic success stories into global success stories. These choices can be overcome. In our “Post-Galapagos committee” we have worked all-year on how to overcome these choices.

Unfortunately the “Galapagos effect” is only one symptom of the crisis of Japan’s electrical giants: most have shown little or no growth in sales over the last 10 years, while at the same time margins tend to be small or negative. Over the same period, General Electric has increased sales by a factor of about three, while at the same time earning healthy margins.

Overcoming this crisis will create many opportunities. If at least some of the conclusions of our “Post Galapagos Committee” can be realized, then our committee’s hard and totally voluntary work during most of this year and many late nights will not be wasted.

For an analysis of Japan’s electrical industry sector see our

Why does it make sense to compare electronics giants with game companies? In many areas, especially home electronics and personal portable devices these two sectors compete for exactly the same consumer spending budgets and mind share.

We also take a look at specialist ROHM, which used to have outstanding margins because of the focus on highly specialized electrical and electronic components. ROHM’s shareholder proposals recently made headlines.

Germany based Siemens and Japanese giants Panasonic and Hitachi in the 1990s all had net margins close to zero. However, while Panasonic and Hitachi maintained their margins close to zero since the 1990s, Siemens clearly aims for US level margins – and achieved a slow and steady upward trend.

Very dramatic restructuring would be necessary to bring Japan’s electric giants onto such a path. I think it is quite obvious exactly which restructuring is necessary. I also believe that if carried out it will actually create more employment in Japan than maintaining the existing structure of Japan’s electrical industry sector. However, actually carrying such restructuring will require superhuman effort… will this happen?

Resistor maker ROHM

Rohm is another interesting story – and a fascinating Kyoto-culture company (with headquarters not so far from superstar Nintendo). Rohm was founded in 1958 by today’s CEO Sato Kenichiro to make resistors, and he later changed the name to R.ohm and then ROHM – today 80% of products are semiconductors. With increasing competition ROHM’s initially very high margins melted away. To counter the trend towards commoditization, ROHM invests heavily in R&D with technology centers around the world. Last week ROHM made global headlines: US fund Brandes had proposed a US$ 157 million share buy back, which was rejected at the shareholder meeting. Looking at ROHM’s margin over the years, its clear that action is required to bring margins again from today’s zero to the previous 20% level. I can sympathize with shareholders who think that a Shuji Nakamura / Nichia-type R&D breakthrough would be more likely to deliver such a comeback rather than a share buy back.

Note that not all shareholder proposals by US or European funds are rejected summarily at Japanese company shareholder meetings… some well prepared proposals have actually been accepted successfully.

Margins of Panasonic, Hitachi, Rohm with Siemens and GE

Starting from similar positions in the 1990s:

GE, Siemens, Hitachi and Panasonic all four had almost the same size in terms of annual sales back in the 1990s – today GE is twice the size of Hitachi or Siemens and 2.5 the size of Panasonic

Today, GE is about twice the size as Hitachi or Siemens, and about 2.5 the size of Panasonic. It seems that successful globalization is a necessary factor to achieve GE-style growth – necessary, but not sufficient… (see: our analysis of dramatic differences in globalization of Japan’s electric groups). The current crisis is a big opportunity for further growth by strong companies.

Revenue growth of Hitachi and Panasonic compared with SIEMENS and GE

Japan’s top 20 electronics companies combined are about as large as The Netherlands economically, and have big impact on the world economy. Our analysis shows how dramatically Japan’s electronics companies have been hit by the current crisis (except for Nintendo). We suggest that full recovery to 2008 (FY2007) levels may take until 2016 – about seven years in terms of income, and about 3-4 years in terms of revenues.

The crisis has thrown Japan’s electrical companies back to 2002 in terms of combined annual net incomes. It has taken Japanese electricals 7 years to climb from the 2002 crisis to the 2008 (FY2007) boom. Since Japan’s electrical companies have made relatively soft adjustments, but not a full fundamental industry restructuring yet, we think that it is likely that developments will proceed along a similar path as in the past: following such an analysis we think that it will take about 7 years from 2009 (ie. until 2016) for Japan’s electrical companies to work their way back up to 2008 net income levels. (Find detailed financial data and analysis in our report on Japan’s electronics industries)

net income of Japan’s electronics companies

Back to FY2003:

Combined annual sales for the financial year ending March 31, 2010, are at a similar level as in FY 2003, ie Japan’s electrical industry has been taken back 6 years in terms of revenue growth. Again, since a dramatic and fundamental industry restructuring has not yet taken place, we believe that we can expect it will take about 4 years for Japan’s electronics industry to grow again to 2008 (FY2007) size in terms of annual revenues.

net revenues of Japan’s electronics companies

The crisis spreads the field…

During the “good” years of FY1997 – FY2007 the differences between top and bottom performing electrical companies became steadily smaller: the field narrowed.

This figure shows that during the current crisis the spread between best and worst performing companies became more than twice as wide. The crisis clearly differentiates winners (Nintendo) from losers in terms of operating margins.

operating margins of Japan’s electronics companies

One of our clients in the financial industry asked me several trend questions:

Q1: Biggest surprises in Japan in 2008?

Collapse of Japan’s mobile phone handset market (read our blog). In this context the Japanese telecom equipment makers association invited me to give a presentation, which was booked out 2-3 weeks ahead – about 100 Japanese telecom equipment maker managers attended! The General Affairs Vice-Minister / Secretary of State attended….

The dramatic increase of acquisitions by Japanese companies:

SANYO suffered from Niigata Chuetsu earthquake of Oct. 23, 2004

Panasonic attracted to SANYO’s battery and energy technologies

On November 7, 2008 Panasonic (“Ideas for Life”) and Sanyo (slogan: “Think GAIA”) announced that they entered negotiations which can potentially lead to an acquisition of Sanyo by Panasonic to form one of the largest electronics groups in the world. Sanyo’s market capitalization is currently US$ 3.9 billion and Panasonic’s is US$ 38 billion, combined sales are about US$ 110 Billion.

The Niigata Chuetsu earthquake of Oct. 23, 2004 caused an estimated total of US$ 30 Billion in damages, damaged Sanyo’s semiconductor factory and contributed to large losses at Sanyo. As a consequence Daiwa Securities SMBC Co, Sumitomo Mitsui Banking Corporation and Goldman Sachs hold preferential shares in Sanyo with voting rights corresponding to 70% of outstanding shares. The current global financial crisis contributes to the potential acquisition, since Daiwa, Sumitomo-Mitsui and especially Goldman Sachs are motivated to sell their preferred shares when contractually possible, and it is also these three financial institutions which will have strong influence on whether this transaction will take place. Goldman Sachs is reported to have said that the price will decide.

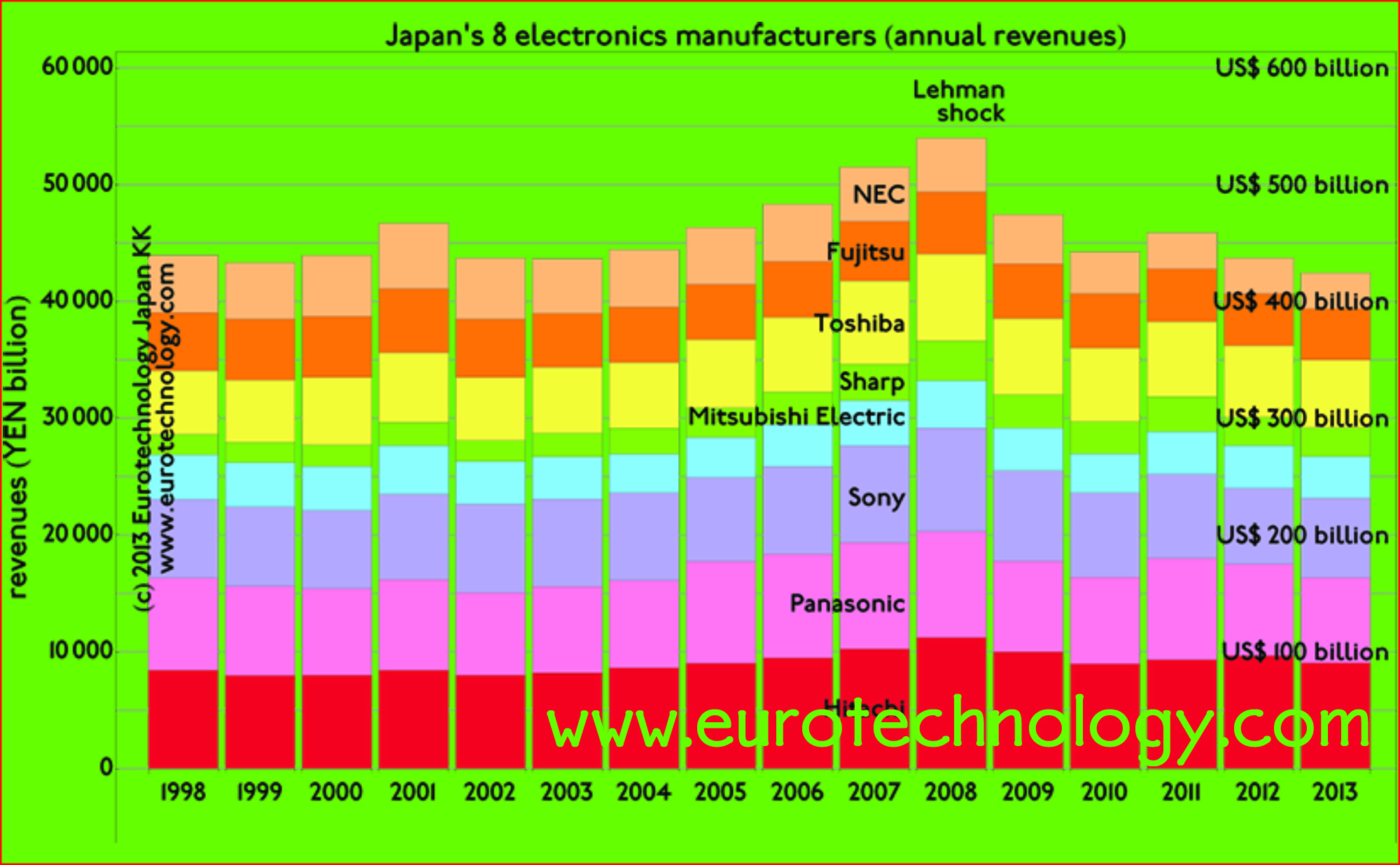

Annual revenues of Japan’s electrical groups:

Panasonic and Sanyo combined (red curve in the figure below) will be one of the largest electrical groups globally. Note that Japan’s electrical groups showed strong growth from FY 2003.

Revenues of Japan’s top electronics manufacturers

Annual operating margins of Japan’s electrical groups:

Panasonic’s high operating margins helped Panasonic to reach a position of financial strength, enabling this acquisition. Expect more acquisitions by Japanese electrical companies.

Electrical differentiation:

High margin (> 5%) vs low margin (The figure below shows that there is a clear differentiation of Japan’s electrical groups: Mitsubishi Electric, Sharp and Panasonic have high margins – above 5%.

The other electrical groups (Fujitsu, Toshiba, Sanyo, Hitachi, Sony and NEC) have chosen a low-margin path (margins below 4%).

There is a clear gap (4% to 5%) separating these two fields. Panasonic’s margin will suffer with a Sanyo acquisition – expect Panasonic management to bring Sanyo up to Panasonic margins.

Operating margins of Japan’s top electronics manufacturers

Globalization of Japan’s electronics groups:

With 36.8% of sales outside Japan, Sanyo is more globalized than Panasonic. NEC, Fujitsu and Mitsubishi Electrical still have much way to go to globalize.

Globalization ratios of Japan’s top electronics manufacturers

Presentation at the CEATEC Conference, talk NT-13, Meeting Room 302, International Conference Hall, Makuhari Messe, Friday October 3, 2008, 11:00-12:00.

The emergence of iPhone, Android, open-sourcing of Symbian, and the growth of mobile data services are changing the paradigm of the global mobile phone business opening new opportunities for Japanese mobile phone makers. Japan’s mobile phone handset makers have missed most opportunities during the first wave of mobile phone opportunities. The developing paradigm change opens new opportunities for Japanese makers. The talk will explain the paradigm shifts and trends of the global mobile phone handset market, and resulting opportunities for Japanese mobile phone makers, and will indicate how these opportunities can actually be realized.