Steve Jobs and SONY: why 180 degrees opposite decisions?

Steve Jobs donates history to Stanford University in order to focus on the future

Steve Jobs and SONY – when Steve Jobs when returned to Apple in 1996, and now SONY are faced with the same question: what to do about corporate archives and the corporate history museum? Interestingly Steve Jobs, and SONY reach exactly 180 degrees opposite answers to the same question:

Steve Jobs donates Apple corporate archives and company museum to Stanford University

SONY sells headquarters building, and keeps SONY corporate archives and company museum

Why opposite answers to the same question? Could it be good advice for SONY, to learn from Steve Jobs, and donate SONY-Museum and SONY-Archives to a University, and focus much more on the future?

Apple donates history collection to Stanford University:

On the Galapagos islands, Charles Darwin noticed a number of species which were extremely beautiful, had evolved on the Galapagos islands locally, and were not able to live anywhere else.

Similarly, due to language, culture, comparatively small interchange between Japan’s markets and foreign markets, some technologies and some products evolved in Japan differently than in other markets.

In part, Japan chose unique Japanese technology standards (e.g. PDC and PHS for mobile phones, 1-seg for mobile TV, FeliCa for RFID contactless and mobile payments) in the hope to achieve global adoption of these Japanese standards, and at the same time to make market penetration of Japan’s markets more difficult for foreign companies in these fields – thus giving an competitive advantage to Japanese companies in their home market Japan.

Japan Galapagos effect: Telecom industry

Japan’s telecommunications industry for a long time used wireless communication standards, and mobile data standards, and frequency bands quite different than those used in other parts of the world. This had several effects:

Foreign companies hoping to enter Japan’s market, had to invest and develop mobile phone and other equipment specifically for the Japanese market, which could not be marketed anywhere else. Thus competing Japanese mobile phone makers and base station makers had a (temporary) competitive advantage in their home market, Japan. However, because of Japan’s limited market size, this competitive advantage in their home market seduced these Japanese companies to neglect global business development. As R&D costs, and especially software development costs increased, lack of global scale made it more and more difficult for these companies to continue viable business.

Because of high investments, and the will of consumers to spend large amounts on mobile communications, and because of Japan’s innovative power and other factors, many mobile technologies and business models were invented in Japan, or came first to market in Japan. These include:

Japanese handset makers and mobile phone base station makers were until recently protected in Japan’s market, Japanese mobile phone operators preferentially purchased Japanese equipment. Japanese mobile phone handset makers and base station equipment makers were not able to compete in the much larger global market.

Necessary consolidation did not take place, so Japanese mobile phone handset makers and base station equipment makers did not scale globally.

Japan Galapagos effect: Galapagos phones (Galake, ガラケ)

Japan introduced mobile internet in February 1999, much earlier than any other country. “Galapagos phones” (Galake, ガラケ) are mobile phones (“feature phones”) typically based on the legacy Symbian operating system, and including a very rich set of features:

Mobile operator specific services, such as DoCoMo’s Concierge services

and more

Galapagos-phones are losing market share against iOS/iPhone and Android smartphones, and we expect Galapagos-keitai (galake) to disappear from the market within a few years to be replaced by iOS, Android, and other smartphones.

Kei car, K-car, 軽自動車 (meaning “light automobile”) is an automotive class, which exists only in Japan. Kei-cars enjoy tax advantages, and Japanese automobile manufacturers are creating very innovative and attractive Kei-cars, however this class of automobile is only restricted to Japan at this time, and cannot achieve global scale at this time.

Positive aspects: Japan Galapagos effect as an opportunity

Mobile internet, electronic money, camera phones and many other advanced technologies were invented and/or first brought to market in Japan, earlier than in all other countries, because of the positive aspects of the Galapagos effect. Japanese companies could develop and bring these new products to market without being slowed down by global standards. Creativity can run free in Japan because of Japan’s Galapagos effect.

Japan post-Galapagos effect working group

The “Post-Galapagos working group” was organized by Takeshi Natsuno (one of the three developers and long-years manager of DoCoMo’s i-Mode mobile internet service) during the years 2008-2009.

The Post-Galapagos working group consisted of about 15 Committee members (Gerhard Fasol was the only non-Japanese Post-Galapagos working group member), met once a month for about one year, and in mid-2009 prepared an released a set of reports with recommendations for

Gerhard Fasol: The Galapagos Effect (talk given for the American Chamber of Commerce in Tokyo, Tokyo Westin Hotel, July 12, 2010, 12:00-14:00), read the article here in the ACCJ Journal

NEC is one of NTT’s traditional four equipment suppliers

NEC is one of NTT’s traditional suppliers of telecom equipment, and one of Japan’s flagship electronics companies. In the early days of the PC age, NEC dominated Japan’s PC market with the 98 series of PC, which had a NEC-proprietary variation of MicroSoft’s MS-DOS operating system.

NEC was the first ever Japanese joint-venture company with foreign capital: NEC started as a joint-venture with Western Electric Company

Interestingly NEC originally started as a joint-venture with Western Electric Company of the United States – NEC was the first Japanese joint-venture company with foreign capital.

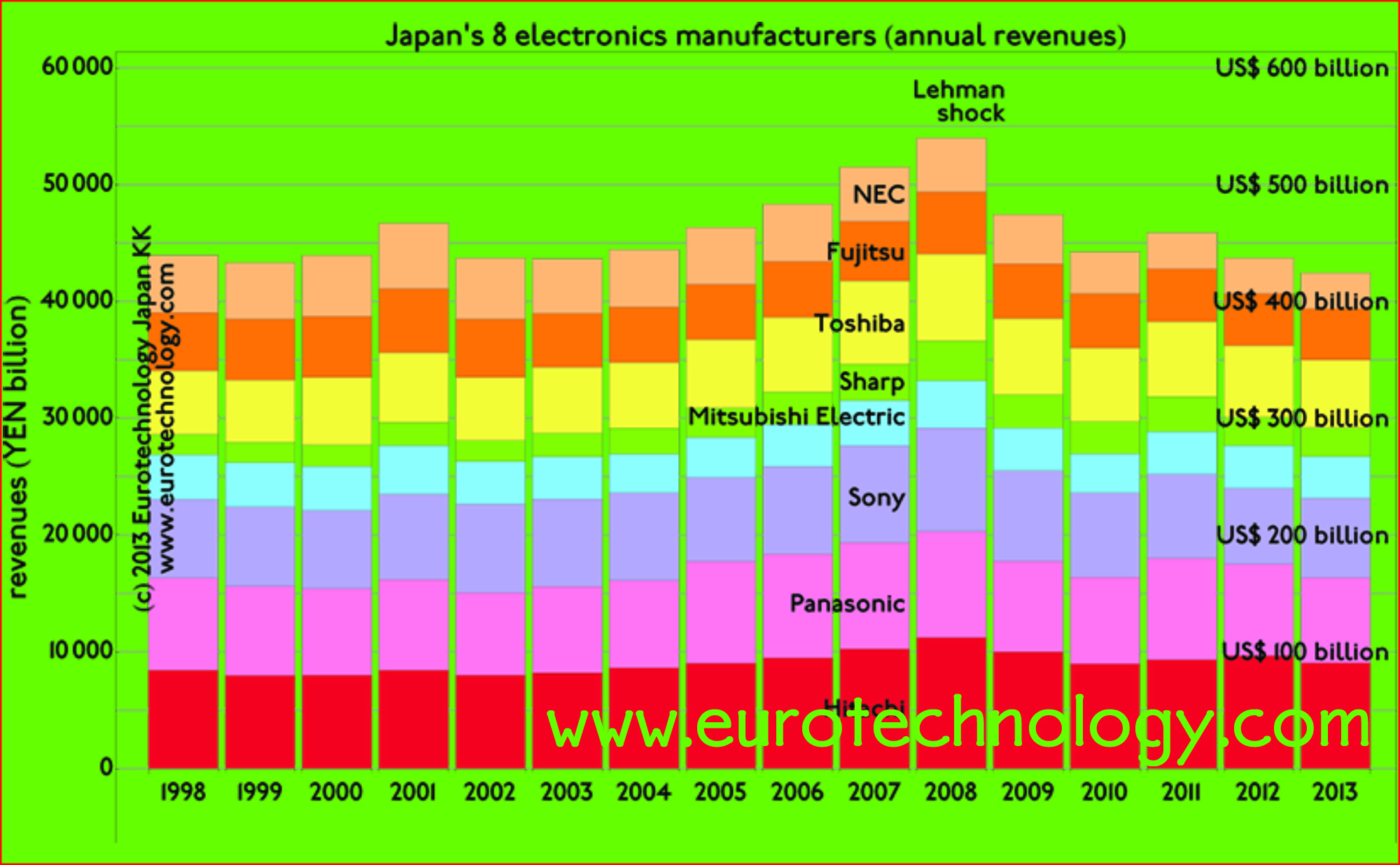

NEC revenues and income overview

Here is an overview of NEC’s financial performance over the last 15 years, the period FY1998 – FY2012 – NEC’s business shrunk from YEN 5000 billion in FY1998 to YEN 3000 billion in FY2012, while on average reporting annual net losses of YEN 39 billion (US$ 390 million)/year over these 15 years.

During the 15 years FY1998-FY2012, NEC revenues declined from YEN 5000 Billion to YEN 3000 Billion, while reporting on average annual net losses of YEN 39 Billion/year. Source: our research report on Japan’s electronic industries. Purchase and download here: https://www.eurotechnology.com/store/j_electric/

Positive and negative aspects of Japan’s Galapagos issues

European Institute of Japanese Studies Academy Seminars presents

Speaker: Dr. Gerhard Fasol, President, Eurotechnology Japan K.K.

Wednesday, June 13, 2012, 18:30 – 21:00

Embassy of Sweden, Alfred Nobel Auditorium

Stockholm School of Economics, European Institute of Japanese Studies

About the talk:

In the last 20 years, several global revolutions were created in Japan, including the LED lighting revolution(1), mobile internet(2), electronic money(3). However, in each case Japan failed to capture much of the global value created by these revolutions. Dr. Fasol will talk about what is holding back Japan from capturing more global value from its unique creativity and how Western companies can do better in Japan, and avoid the most well-known traps

About the speaker:

For the last 15 years, Gerhard Fasol has worked with more than 100 investment fund managers in Japan, advising them on technology inflections, initiated and managed business development and assisted M&A projects. Dr. Fasol is currently working with several US and European companies in these areas, helping them onto successful paths in Japan. Dr. Fasol has been an Advisory Board member to the Chairman of JETRO and the only foreigner on Japan’s “Post Galapagos working group”.

Gerhard has an extensive business and academic career, as manager of one of Hitachi’s R&D labs, University Lecturer in Physics at Cambridge University. He also served as Director of Studies at Trinity College Cambridge, Research Scientist at the Max-Planck-Institute for Solid State Science in Stuttgart, and invited Professor at the Ecole Normale Superieure in Paris, was one of the first working on spin-electronics and magnetic memories in Japan, and has won a Sakigake research program from Japan’s Science and Technology Agency while faculty member in Electrical Engineering at the University of Tokyo. Gerhard graduated with a PhD in Solid State physics from Cambridge University and Trinity College, Cambridge, UK.

Gerhard Fasol lecture at Stanford University: “New opportunities vs old mistakes – foreign companies in Japan’s high-tech markets”

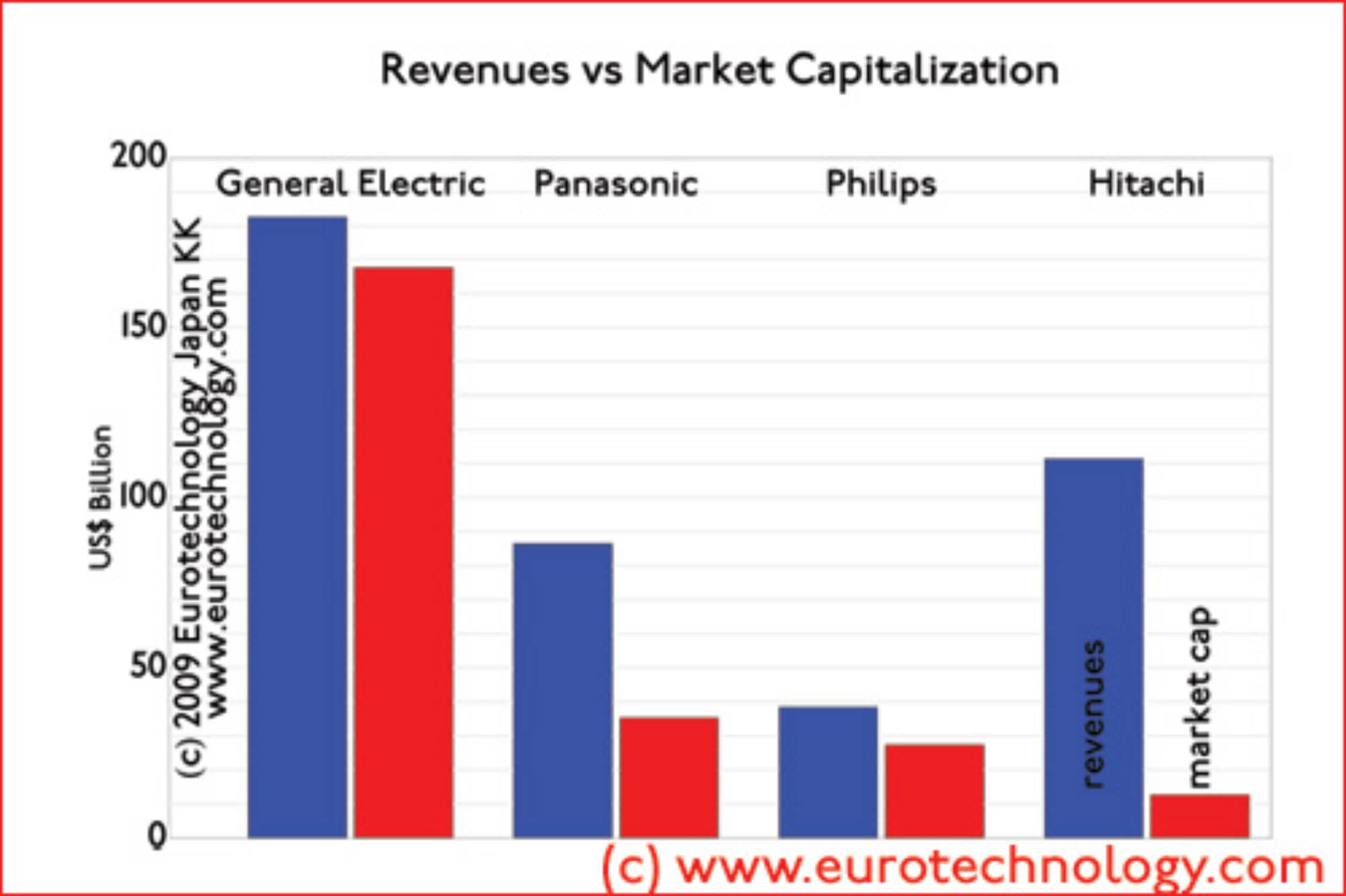

Japan’s electronics giants market caps are remarkably low

General Electric’s market cap is about 13 times higher that of Hitachi

Some of Japan’s electrical corporations have remarkably low market capitalizations: General Electric has 1.6 x more sales than Hitachi, but has 13.3 x the market capitalization. Philips has 1/3 x Hitachi’s sales, but has 2.2 times higher market cap.

Low market values do not help big recent public share offerings: Hitachi raising YEN 250.7 Billion (US$ 2.8 Billion), Toshiba raising YEN 298.7 Billion (US$ 3.3 Billion), and NEC raising YEN 115.5 Billion (US$ 1.3 Billion).

Low valuations increase the pressure for change in Japan’s electrical sector, and the SANYO-Panasonic merger is an indication of changes to come.

In the “post-Galapagos committee” we are working with some of Japan’s brightest leaders on understanding the reasons and on how to drive this change.

Benchmarking Japan’s electrical companies – Philips= 1/3 x Hitachi’s sales and 2.2 x Hitachi’s market cap:

GE= 1.6 x Hitachi’s sales and 13.3 x Hitachi’s market cap

Japan Galapagos effect: “Why do Japanese companies make so beautiful mobile phones with fantastic functions, and have almost no global market share?”

I asked this question back in 2003 to NTT-DoCoMo’s CEO Dr. Tachikawa (see my article “Leadership questions of the week” in Wallstreet Journal of June 12, 2006, page 31), and offered several proposals to Dr. Tachikawa, of which he accepted one.

A related question is: “why can Samsung, LG and Apple beat Japan’s initially far more advanced mobile phone makers, and why have Japan’s phone makers taken no effective action to build global business in order to avoid extinction?”

Now six years after my initial presentation to DoCoMo’s CEO, I have been invited as the only non-Japanese to work on Japan’s “Post-Galapagos Committee”. For most of this year our small group of industry CEOs, academics, government officials and other leaders have been working on understanding the reasons for Japan’s “Galapagos effect” and how to overcome it.

The “Galapagos effect” has not been created by a single factor. Instead a collection of choices by the management teams of Japan’s electrical conglomerates have prevented leverage of their domestic success stories into global success stories. These choices can be overcome. In our “Post-Galapagos committee” we have worked all-year on how to overcome these choices.

Unfortunately the “Galapagos effect” is only one symptom of the crisis of Japan’s electrical giants: most have shown little or no growth in sales over the last 10 years, while at the same time margins tend to be small or negative. Over the same period, General Electric has increased sales by a factor of about three, while at the same time earning healthy margins.

Overcoming this crisis will create many opportunities. If at least some of the conclusions of our “Post Galapagos Committee” can be realized, then our committee’s hard and totally voluntary work during most of this year and many late nights will not be wasted.

For an analysis of Japan’s electrical industry sector see our

We also take a look at specialist ROHM, which used to have outstanding margins because of the focus on highly specialized electrical and electronic components. ROHM’s shareholder proposals recently made headlines.

Germany based Siemens and Japanese giants Panasonic and Hitachi in the 1990s all had net margins close to zero. However, while Panasonic and Hitachi maintained their margins close to zero since the 1990s, Siemens clearly aims for US level margins – and achieved a slow and steady upward trend.

Very dramatic restructuring would be necessary to bring Japan’s electric giants onto such a path. I think it is quite obvious exactly which restructuring is necessary. I also believe that if carried out it will actually create more employment in Japan than maintaining the existing structure of Japan’s electrical industry sector. However, actually carrying such restructuring will require superhuman effort… will this happen?

Resistor maker ROHM

Rohm is another interesting story – and a fascinating Kyoto-culture company (with headquarters not so far from superstar Nintendo). Rohm was founded in 1958 by today’s CEO Sato Kenichiro to make resistors, and he later changed the name to R.ohm and then ROHM – today 80% of products are semiconductors. With increasing competition ROHM’s initially very high margins melted away. To counter the trend towards commoditization, ROHM invests heavily in R&D with technology centers around the world. Last week ROHM made global headlines: US fund Brandes had proposed a US$ 157 million share buy back, which was rejected at the shareholder meeting. Looking at ROHM’s margin over the years, its clear that action is required to bring margins again from today’s zero to the previous 20% level. I can sympathize with shareholders who think that a Shuji Nakamura / Nichia-type R&D breakthrough would be more likely to deliver such a comeback rather than a share buy back.

Note that not all shareholder proposals by US or European funds are rejected summarily at Japanese company shareholder meetings… some well prepared proposals have actually been accepted successfully.

Margins of Panasonic, Hitachi, Rohm with Siemens and GE

Starting from similar positions in the 1990s:

GE, Siemens, Hitachi and Panasonic all four had almost the same size in terms of annual sales back in the 1990s – today GE is twice the size of Hitachi or Siemens and 2.5 the size of Panasonic

Today, GE is about twice the size as Hitachi or Siemens, and about 2.5 the size of Panasonic. It seems that successful globalization is a necessary factor to achieve GE-style growth – necessary, but not sufficient… (see: our analysis of dramatic differences in globalization of Japan’s electric groups). The current crisis is a big opportunity for further growth by strong companies.

Revenue growth of Hitachi and Panasonic compared with SIEMENS and GE

It is well known that mobile internet, mobile payments and mobile content business and many other areas of mobile broadband are much more developed in Japan and South Korea than in other countries.

NOKIA and Vodafone and some other western mobile phone companies had the opportunity to take part in Japan’s mobile payment systems, mobile TV solutions and many other mobile businesses – instead they preferred not to do so and to withdraw from Japan’s mobile market.

Similarly it seems that mobile payments, mobile TV developments outside Japan are being developed from scratch without much regard to what has been learnt in Japan in debugging such mobile businesses both from the technology viewpoint as well as the usability, security, convenience etc viewpoints.

Lets discuss if the “not invented here syndrome” could be a factor.

u-Japan follows i-Japan and e-Japan to take Japan to the forefront of global IT developments

Presentation at the EU-Japan Center for Industrial Cooperation, 12 October 2006

Title: “Japan’s Mobile Phone Industry and u-Japan”

Date and Time: Thursday, 12th October 2006, 17:00-19:00

Location (tentative, please check closer to the date for changes):

Main Conference Room 4F, EU-Japan Centre for Industrial Cooperation, Tokyo

Agenda: u-Japan and Japan as the mobile internet pioneer

Japan’s mobile phone and broad-band markets are about 3-6 years ahead of Europe: new services are typically invented or first brought to market in Japan, 3-6 years earlier than in Europe. Internet in Japan is generally much faster and much cheaper than in Europe. For this reason and because of it’s size, Japan’s telecom markets are full of opportunities for European companies with the right products and the right strategy, and for investors with the necessary knowledge.

Japan’s mobile phone industry is notoriously difficult to understand for Europeans because it’s market logic is very different from Europe’s, and because the pace of innovation and structural change is much faster, and because of the language barriers.

This talk will explain the driving forces behind recent dramatic changes in Japan’s mobile telecom sector, and will explain new changes that the “ubiquitous-Japan” (“u-Japan”) policy will bring in the near future.

Do you need to know what Europe’s mobile phone and internet markets will look like in 2010 or 2015? – Come to this talk and you will get a good look into Europe’s IT future about 5 years ahead, as well as Japan’s telecom markets today.

Background: Japan – the mobile internet pioneer, and Vodafone’s departure from Japan

The EU Technology Attaches were particularly interested in the impact on Europe by the termination of by far the biggest ever European investment in Japan. Clearly it is also important to determine, what other European companies can learn from Vodafone’s experience.

Eurotechnology Japan KK has been awarded a contract by the European Union to benchmark Japan’s telecom sector vs EU and make recommendations.

More about Japan’s telecom sector

Read our report on Japan’s telecommunications markets

The European Institute of Japanese Studies (EIJS Academy in Tokyo) of the Stockholm School of Economics will hold a seminar in Tokyo-Marunochi on Thursday, February 16, 2006:

Topic: “Why are Mobile Phones (Keitai) so hot in Japan? – and How European companies in all sectors can profit from Keitai”

Speaker: Gerhard Fasol

Gerhard Fasol “Why are keitai so hot in Japan?” Embassy of Sweden

Agenda:

Japan created the most passionate and most advanced mobile communications (keitai) market in the world. Recently, almost all innovations in mobile communications have been developed or brought to market first in Japan. Fasol’s talk will explain why this is, and how European companies in all fields, from retail to publishing can profit by building keitais into their business models.

Date: Thursday, February 16, 2006

Time:

6.15 – 7.00 p.m. Drink and Snack (served before the lecture)

7.00 – 9.00 p.m. Lecture and Discussion

Place:

Marubiru Conference Square, Room 2 (Tel: 03-3217-7111) 8th floor of Marubiru, 2-4-1 Marunouchi, Chiyoda-ku, Tokyo One-minute walk from JR Tokyo Station, Marunouchi South Exit

Fee: JPY2,000 per person, payable at the door Free for students, please bring your student ID Free for those who are from sponsoring companies

Advance registration required: Please sign up (via email) or fax to (FAX 03-3212-1530) for the attention of Ms. Futagawa (EIJS Tokyo Office.)