Here is the answer: the first mobile phone with qr-code reader was the J-SH09 produced by SHARP for Japan’s J-Phone mobile operator (today’s Softbank) and came on sale in August 2002 – seven years ago.

More details and more than 100 case studies of qr-code applications in our QR-Code report

The total solar eclipse could be seen clearly today around 11:13am in Tokyo – however in Tokyo the coverage was not total. Here is a picture taken with a standard Canon digital camera:

Japan introduced the mobile internet with i-Mode in 1999, while i-Phone and friends are now getting the rest of the world hooked onto the mobile internet.

Games used to be played in game parlors, and some of Japan’s game giants were originally and still are game parlor machine makers – a round of Dance-Dance-Revolution anyone? Next came consoles, cassettes and handhelds, taking the growth momentum out of game parlors, and establishing a pattern of growth by generations (today we are in the 7th Generation). Nintendo broke the cozy generation pattern where pixels and MHz increased in predictable ways from Generation to Generation without much other fundamental change. Nintendo took games sideways into the blue oceans of motion sensors and to the silver generation, women and other previously non-gaming majorities, while Xbox and SONY kept slugging out the generation game.

We have been analyzing the Tokyo Game Show for many years – at the 2004 Tokyo Game Show, when SONY gave previews of the PSP – actually, I was personally much more interested in DoCoMo’s huge exhibition village setting a stage for about 15 mobile phone gaming partners.

Since i-Mode started mobile phone games in 1999, online and mobile phone games combined have essentially outgrown the video game software sector in 2009, and are certain to grow much more in coming years – the iPhone is not slowing mobile phone based gaming down…. Those who only count video game cassettes and consoles, certainly don’t see the rapid mobile and online growth – and complain about shrinking markets.

Is Nintendo now being blind-sided by mobile phones and app-stores?

I don’t think so: not blind-sided – but strongly affected. Actually, Nintendo’s CEO and games developer Shigeru Miyamoto tell us they want to make their DSi’s central to everybody’s lives – with built in cameras, payments, app-stores, navigation. Essentially everyone on planet earth has a mobile phone, or will soon have one, or two. Many of todays phones in people’s hands can’t yet play games nicely – but DoCoMo’s phones do – and iPhones do also. Thats why we already see a lot of mobile gaming in Japan. Imagine the day when most mobile phones on planet earth can play games nicely? Will that day come?

Will people upgrade to a DSi? or to a PSP? or to a better mobile phone? Apple and DoCoMo are both proof that people do pay for downloading games from i-Mode or i-Tunes app-stores – and that’s exactly the growth we see in the Figure – you don’t see that growth if you count only the number of game cassettes and consoles sold. In any case we may not see an 8th generation console – people might upgrade their phones instead – or use Skype on their PSP.

Exponential growth: The number of e-cash payments per month increases by a factor of 10 about every 4 years

E-money transactions (including mobile e-cash) grow exponentially in Japan, and we expect to see 1 Billion e-money transactions/month around 2014 (this figure would be much bigger if contactless train travel tickets were included). e-Money now represents about 2% of all cash (banknotes + coins) in circulation in Japan, a recent examination of e-money by the Bank of Japan shows. More below, and a detailed analysis in our mobile payment and e-money report, where we combine the newest data from the Bank of Japan with our own research data.

Exponential growth: The number of e-cash payments per month increases by a factor of 10 about every 4 years

We expect 1 billion e-money transactions per month around 2014. Green curve shows payments with Suica, Pasmo and Edy (not including train travel). The blue curve shows data for all e-money transactions researched by the Bank of Japan.

Total number of e-money transactions in Japan per month

Research by the Bank of Japan shows that e-money has reached the level of 2% of all cash in circulation (bank notes and coins).

Why does it make sense to compare electronics giants with game companies? In many areas, especially home electronics and personal portable devices these two sectors compete for exactly the same consumer spending budgets and mind share.

Mobile phone payments with RFID start in Japan in 2003

i-Mode mobile payments started in Japan in 1999

10 years ago – 1999 – the global mobile payment revolution started in Japan: with i-mode introducing an essentially Japan-only highly successful micropayment system for online content and brick-and-mortar based m-commerce, and SONY’s Edy starting e-cash experiments in Tokyo’s Osaki district. In 2003 SONY’s Felica IC semiconductor chips were combined with mobile phones to introduce the first “wallet phones” (“saifu keitai”). Today the majority of mobile phones in Japan are wallet phones.

For the last 10 years, Japan has been a laboratory for mobile payments and e-cash, conducting a test on 125 million population on which mobile payment and e-cash models work and which don’t. -> We can all learn from Japan’s 10 years of experimentation which mobile payment business models are likely to work, and which might fail!

Edy stands for Euro, Dollar, Yen… expressing the hope for global success – Intel Capital believes in this success and has invested in the company that runs Edy: BitWallet (initially backed by SONY and now acquired by Rakuten).

Which are the most effective e-cash systems?

While SONY has distributed the largest number of cards, in our view the world’s largest (by payment volume) and most effective e-cash and mobile payment system is operated by the world’s largest railway company: SUICA and mobile SUICA.

Edy, SUICA and other e-cash usage in Japan

the world’s most effective railway company in our view also operates the world’s most effective mobile commerce system: The Express Card / EX-IC system.

We also take a look at specialist ROHM, which used to have outstanding margins because of the focus on highly specialized electrical and electronic components. ROHM’s shareholder proposals recently made headlines.

Germany based Siemens and Japanese giants Panasonic and Hitachi in the 1990s all had net margins close to zero. However, while Panasonic and Hitachi maintained their margins close to zero since the 1990s, Siemens clearly aims for US level margins – and achieved a slow and steady upward trend.

Very dramatic restructuring would be necessary to bring Japan’s electric giants onto such a path. I think it is quite obvious exactly which restructuring is necessary. I also believe that if carried out it will actually create more employment in Japan than maintaining the existing structure of Japan’s electrical industry sector. However, actually carrying such restructuring will require superhuman effort… will this happen?

Resistor maker ROHM

Rohm is another interesting story – and a fascinating Kyoto-culture company (with headquarters not so far from superstar Nintendo). Rohm was founded in 1958 by today’s CEO Sato Kenichiro to make resistors, and he later changed the name to R.ohm and then ROHM – today 80% of products are semiconductors. With increasing competition ROHM’s initially very high margins melted away. To counter the trend towards commoditization, ROHM invests heavily in R&D with technology centers around the world. Last week ROHM made global headlines: US fund Brandes had proposed a US$ 157 million share buy back, which was rejected at the shareholder meeting. Looking at ROHM’s margin over the years, its clear that action is required to bring margins again from today’s zero to the previous 20% level. I can sympathize with shareholders who think that a Shuji Nakamura / Nichia-type R&D breakthrough would be more likely to deliver such a comeback rather than a share buy back.

Note that not all shareholder proposals by US or European funds are rejected summarily at Japanese company shareholder meetings… some well prepared proposals have actually been accepted successfully.

Margins of Panasonic, Hitachi, Rohm with Siemens and GE

Starting from similar positions in the 1990s:

GE, Siemens, Hitachi and Panasonic all four had almost the same size in terms of annual sales back in the 1990s – today GE is twice the size of Hitachi or Siemens and 2.5 the size of Panasonic

Today, GE is about twice the size as Hitachi or Siemens, and about 2.5 the size of Panasonic. It seems that successful globalization is a necessary factor to achieve GE-style growth – necessary, but not sufficient… (see: our analysis of dramatic differences in globalization of Japan’s electric groups). The current crisis is a big opportunity for further growth by strong companies.

Revenue growth of Hitachi and Panasonic compared with SIEMENS and GE

Japan’s top 20 electronics companies combined are about as large as The Netherlands economically, and have big impact on the world economy. Our analysis shows how dramatically Japan’s electronics companies have been hit by the current crisis (except for Nintendo). We suggest that full recovery to 2008 (FY2007) levels may take until 2016 – about seven years in terms of income, and about 3-4 years in terms of revenues.

The crisis has thrown Japan’s electrical companies back to 2002 in terms of combined annual net incomes. It has taken Japanese electricals 7 years to climb from the 2002 crisis to the 2008 (FY2007) boom. Since Japan’s electrical companies have made relatively soft adjustments, but not a full fundamental industry restructuring yet, we think that it is likely that developments will proceed along a similar path as in the past: following such an analysis we think that it will take about 7 years from 2009 (ie. until 2016) for Japan’s electrical companies to work their way back up to 2008 net income levels. (Find detailed financial data and analysis in our report on Japan’s electronics industries)

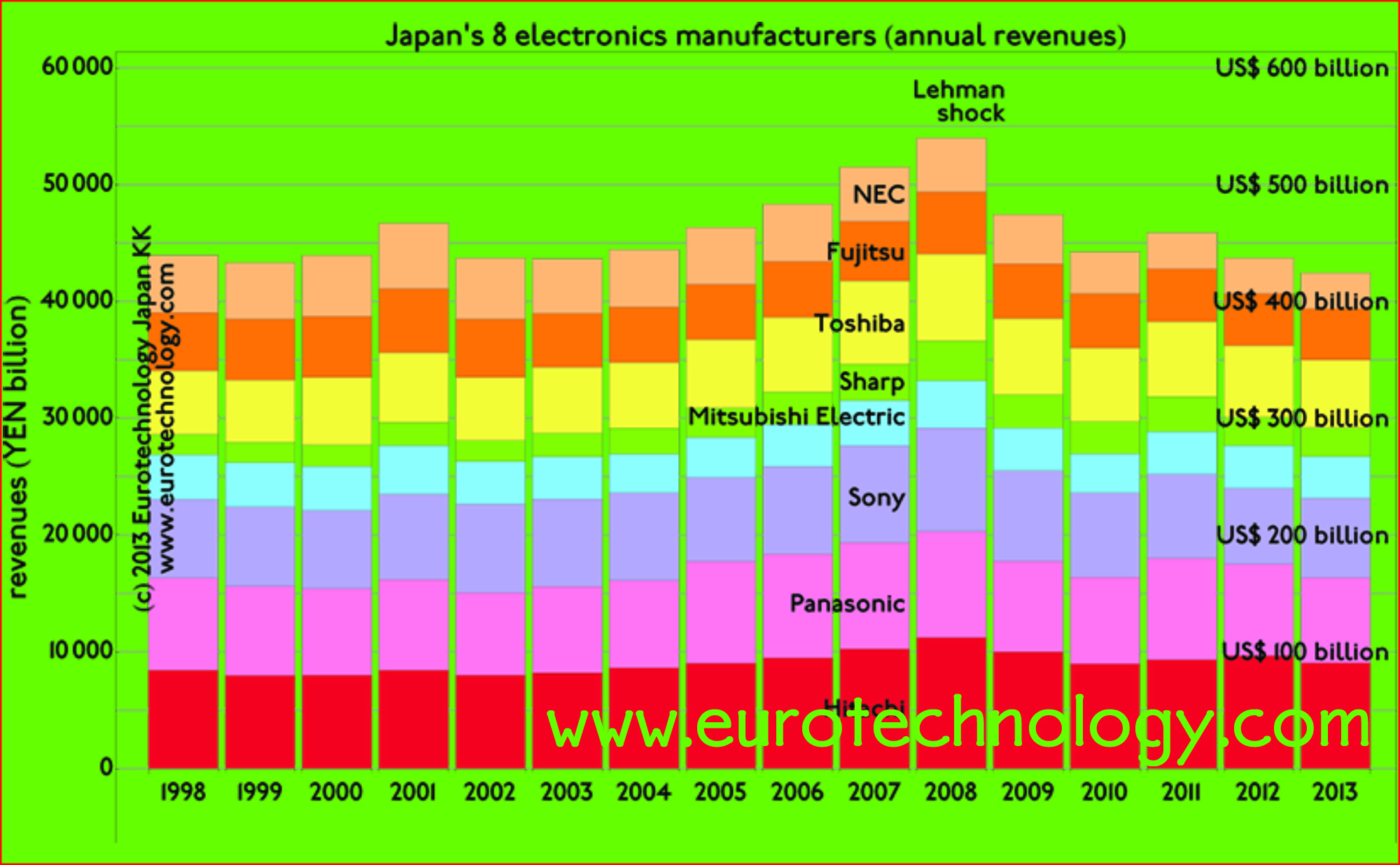

net income of Japan’s electronics companies

Back to FY2003:

Combined annual sales for the financial year ending March 31, 2010, are at a similar level as in FY 2003, ie Japan’s electrical industry has been taken back 6 years in terms of revenue growth. Again, since a dramatic and fundamental industry restructuring has not yet taken place, we believe that we can expect it will take about 4 years for Japan’s electronics industry to grow again to 2008 (FY2007) size in terms of annual revenues.

net revenues of Japan’s electronics companies

The crisis spreads the field…

During the “good” years of FY1997 – FY2007 the differences between top and bottom performing electrical companies became steadily smaller: the field narrowed.

This figure shows that during the current crisis the spread between best and worst performing companies became more than twice as wide. The crisis clearly differentiates winners (Nintendo) from losers in terms of operating margins.

operating margins of Japan’s electronics companies