This morning 7:30am I was interviewed on BBC TV Asia Business Report about an update of Toshiba’s ongoing crisis, which has been 20 years in the making.

Here some notes in preparation for my interview.

What is Toshiba’s situation now?

Toshiba’s market cap today is YEN 1024 billion = US$ 9.6 billion.

Toshiba is expected today to announce write-off provisions on the order of US$ 6 billion.

Toshiba owes about US$ 5 billion to main banks as follows:

Mizuho YEN 183.4 billion

SMBC YEN 176.8 billion

Sumitomo Mitsui Trust Holdings YEN 131.0 billion

BTMU YEN 111.2 billion

Total YEN 602.4 billion = US$ 5.3 billion

Toshiba is on notice for delisting by the Tokyo and Nagoya Stock Exchanges, and faces the risk of being delisted by March 15, 2017, i.e. in about 4 weeks from now.

Toshiba is trying to raise capital e.g. by seeking investment in the IC/flash memory division, however, Toshiba seeks to keep control, so Toshiba is trying to raise a minority share, or non-voting shares or similar, in order not to lose control.

How did Toshiba get into a situation to potentially need to write off US$ 6 billion?

Toshiba acquired 87% of the US nuclear equipment manufacturer Westinghouse.

While Westinghouse is a famous name, what Toshiba actually acquired seems to have gone through a period of restructuring.

In 2015 Toshiba acquired the construction company SHAW’s assets from the Chicago Bridge & Iron Company CB&I for US$ 229 million plus assumed liabilities. CB&I had acquired SHAW for US$ 3.3 billion in July 2012, and SHAW has on the order of US$ 2 billion annual sales.

Why did Toshiba acquire a company for US$229 million, which has US$ 2 billion annual sales, and which was in 2012 acquired for US$ 3.3 billion? Which factors reduced the value of this company from US$ 3.3 billion to US$ 229 million within the 3 years from 2012 to 2015?

Presumably because there are large liabilities arising from nuclear construction, which Toshiba now seems to have to assume.

What is likely to happen now with Toshiba? Is Toshiba too big to fail?

Difficult to say what will happen. Toshiba is a huge corporate group with about 200,000 employees and many factories in many countries, so clearly Toshiba is not going to disappear without trace.

The immediate risk is that Tokyo Stock Exchange carries out its warning, and delists Toshiba, which will further increase Toshiba’s ability to raise capital. In the case of a delisting, private equity, and/or government might invest and restructure, and Toshiba might be split up. For example, Toshiba’s nuclear Westinghouse division is totally separate from its very successful flash memory division, there is not much business logic in having both under one holding company.

Impact on UK

Toshiba acquired 60% of UK based NuGeneration with the view to build nuclear power stations in the UK. This project requires Toshiba to contribute to the funding of the nuclear project, for which Toshiba would probably need a financially healthy partner.

What is the big picture? How did Toshiba get into this crisis?

Toshiba’s crisis has been building up for 20 years, and is in my view a consequence of corporate governance issues over a long time.

Essentially, Toshiba should have been reformed 20 years ago from the top down.

Japan’s 8 electronics giants have had essentially no growth and no profits for 20 years. This tragedy has been obvious for many years now, and was a big contributing factor for Japan’s government to reform Japan’s corporate governance laws and regulations, see:

Toshiba’s Board of Directors was exchanged in September 2015, and now includes several very capable and experienced Japanese independent Board Directors, but unlike Hitachi, even today neither Toshiba’s Board of Directors, nor Toshiba’s Executive Board include one single foreigner.

One might think that a huge global group like Toshiba with complex businesses around the globe might benefit from a variety of view points and experiences from different countries at Supervisory Board and Executive Board level – not all just from one single country. Japanese corporations including Hitachi, SoftBank, Nissan and a small number of others are now recognizing the benefits of diversity of experience and viewpoints at Supervisory Board and Executive Board level.

We can only hope that Toshiba’s executives and Board Directors have the experience and ability to solve the extremely complex issues deep inside the bowels of the US nuclear construction industry – far away on the other side of the world.

Quarterly financial reports: can they be the trees which obscure long term growth of the forrest?

As a Board Director of a Japanese company traded on the Tokyo Stock Exchange I have to study and approve monthly, quarterly and annual financial reports, and I share responsibility for the future success of the company.

It is obvious that the longterm success and growth of the company is the most important priority for all stake holders. So how useful are quarterly financial reports? Lets look at some recent developments and at an example below from our Report on Japan’s Telecommunications Industries.

Motivated by Professor John Kay’s report, the UK regulator removed the requirement for companies to publish quarterly financial reports.

Mark Zinkula, CEO of Legal & General Investment Management, one of UK’s largest investment management firms, around 8 June 2015 wrote a carefully worded letter to 350 UK company Chairmen, recognizing that each company has different circumstances, and encouraging them to report the most meaningful key metrics and to omit reporting quarterly financial results if these don’t contribute to longterm value creation. You can download Mark Zinkula’s letter as a pdf file here.

The European Union (EU) reduced the reporting requirements including the requirement for quarterly financial reporting.

Will Japan and other important countries such as USA follow this trend as well?

Quarterly financial reports: pro’s and con’s

Essentially all well managed companies have fine grained financial management systems which document the financial position of the company at any moment in time.

As an example, when Kazuo Inamori rebuilt Japan Airlines from bankruptcy, he created a reporting system which calculates the profit/loss of every single flight in real time: i.e. when a Japan Airlines flight from Tokyo arrives in San Francisco, the pilot and everyone else knows before landing in San Francisco whether this particular flight was profitable or not – while before Japan Airlines bankruptcy, profit/loss (mainly losses for the last years leading up to bankruptcy) was determined on a full company basis every 3 months in arrears. Read Kazuo Inamori’s talk here. Clearly Kazuo Inamori thinks that such fine grained profit/loss awareness is a crucial component for Japan Airlines’ revival from bankruptcy.

Its obvious that for today’s IT systems the creation of quarterly financial reports from such fine-grained measurement systems such as Kazuo Inamori had installed at Japan Airlines does not cause much additional effort or costs once the coding is done.

Quarterly financial reports: trees vs. the forrest

Quarterly financial reports can be complicated to understand for highly cyclical industries: lets have a look at the quarterly vs annual reports of Japan’s mobile operators from our Report on Japan’s Telecommunications industries.

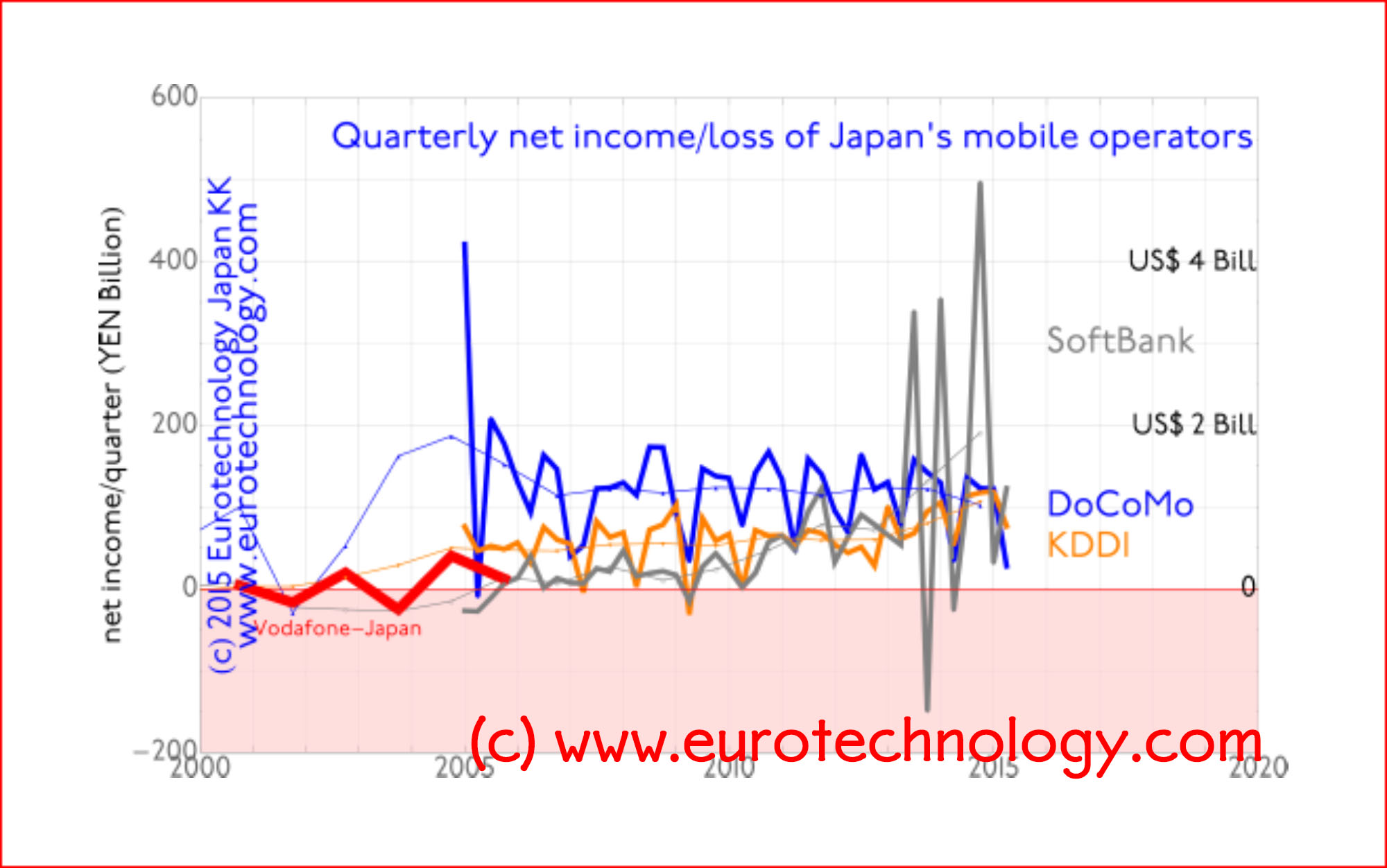

The figures below show exactly the same financial data – the net income (= profit) of Japan’s mobile operators NTT-Docomo, SoftBank and KDDI over the last 10-15 years:

Upper Figure:quarterly net income (thick curves) vs annual net income (thin curves)

Lower Figure: quarterly net income (thin curves) vs annual net income (thick curves)

Net income of Japan’s mobile operators: quarterly results (thick curves) vs annual results (thin curves)Net income of Japan’s mobile operators: quarterly results (thin curves) vs annual results (thick curves)

It is hard to draw conclusions from quarterly income curves above. Most eye-catching is that SoftBank’s quarterly income results became much more fluctuating in the last two years. Its hard to judge the relative performance of Docomo, SoftBank and KDDI from the quarterly income curves.

Annual net income curves give a much clearer picture. Annual figures clearly show that SoftBank caught up and overtook Docomo and KDDI in net profits.

As Mark Zinkula points out that every company and every industry is different. In the case of Japan’s mobile operators, annual figures give a clearer picture.

Will quarterly financial reports become voluntary and go away? They might partly in the UK, and maybe also in other countries. As so often in finance, the UK sets the global trends.

Quarterly financial reports & the Toshiba accounting issues

Quarterly financial reports can be the trees and annual reports the forrest… seeing the forrest can be more important than seeing individual trees

Independent 3rd party committee chaired by former Chief Prosecutor of Tokyo High Court

On 12 June, 2015, Toshiba announced corrections to income reports, and at the same time engaged an independent 3rd party investigation committee headed by former Chief Prosecutor at the Tokyo High Court, Mr Ueda, to investigate. This independent 3rd party committee submitted their report yesterday, and held a Press Conference this evening.

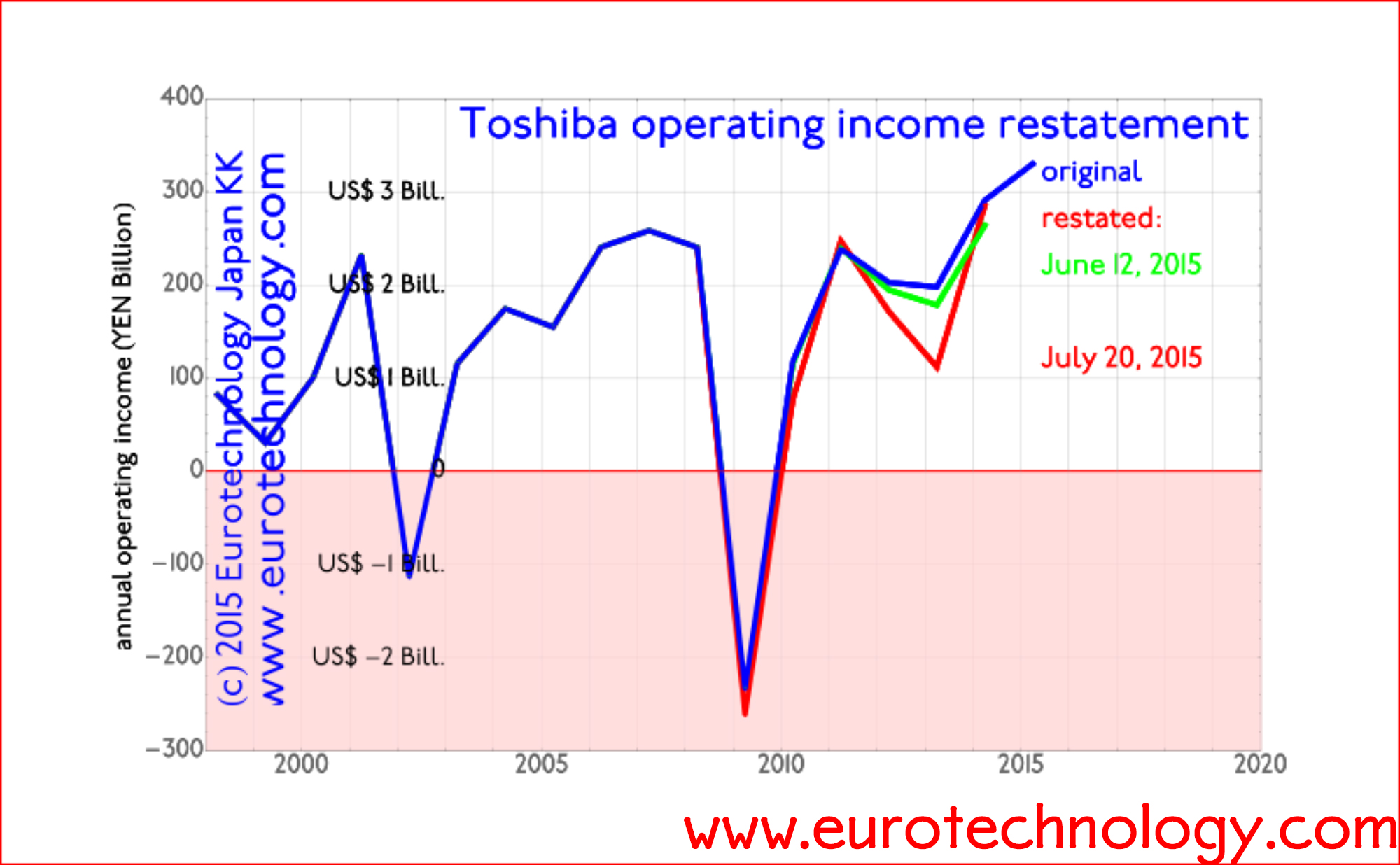

Lets look at the announced Toshiba financial data in detail. The figure below shows:

corrections announced by an internal committee on June 12, 2015 (green curve),

corrections announced by the independent 3rd party committee on July 20, 2015 (red curve).

The combined amount of downward corrections determined by the independent 3rd party committee is YEN 151.8 billion (US$ 1.22 billion) in total.

Lets put this amount into context:

annual sales: approx. YEN 6000 billion (US$ 60 billion)

annual operating income (average over last 17 years): YEN 148 billion (US$ 1.5 billion)

annual net income (average over last 17 years): YEN 19 billion (US$ 190 million)

Therefore the downward correction summed over the years corresponds to:

approx. 2.5% of average annual sales

approx. 103% of average annual operating profits, ie more than a full year of average operating profits

approx. 8 years of net profits

Toshiba – typical for Japan’s large electronics corporations – operates with razor-thin profit margins: Toshiba’s net profit margin averaged over the last 17 years is 0.25%.

Therefore, the downward correction corresponds to 8 years of average net income/profits.

Blue curve shows Toshiba’s initially reported operating income.

Green curve shows corrections determined by an internal examination, announced on June 12, 2015. Corrections amount to approx. YEN 50 billion (= approx. US$ 0.5 billion).

Red curve shows corrections determined by the independent 3rd party commission, chaired by former Tokyo High Court Chief Prosecutor Ueda and announced on July 20, 2015. Corrections amount to YEN 151.8 billion (= approx. US$ 1.22 billion)

Toshiba over the last few weeks published a number of announcements, and corrections to these announcements concerning accounting issues. Toshiba also engaged internal and independent external expert commissions to analyze possible accounting discrepancies, these committees have made preliminary announcements.

At a recent Press Conference, the CEO of the Japan Exchange Group (JXP) which includes the Tokyo Stock Exchange, Mr Atsushi Saito, said that “he feels very much ashamed for Toshiba”, and that “he cannot understand how Toshiba can be so lazy about their accounting”.

To understand Toshiba in the context of Japan’s electronics industry, read our report on Japan’s electronics industry sector:

Japan’s top-8 electronics giants – including Toshiba – have essentially stagnated for the last 17 years with negligible growth and negligible profits. Japan’s top 8 electronics groups combined have sales approximately as large as the economy of The Kingdom of the Netherlands. However, the big difference is, that in the 17 years since 1998, the economy of The Netherlands has approximately doubled, while Japan’s top 8 electronics companies have not grown their sales at all over these 17 years. Expressed in Japanese YEN, the combined sales of Japan’s top 8 electronics companies in FY1998 is about the same as in FY2014.

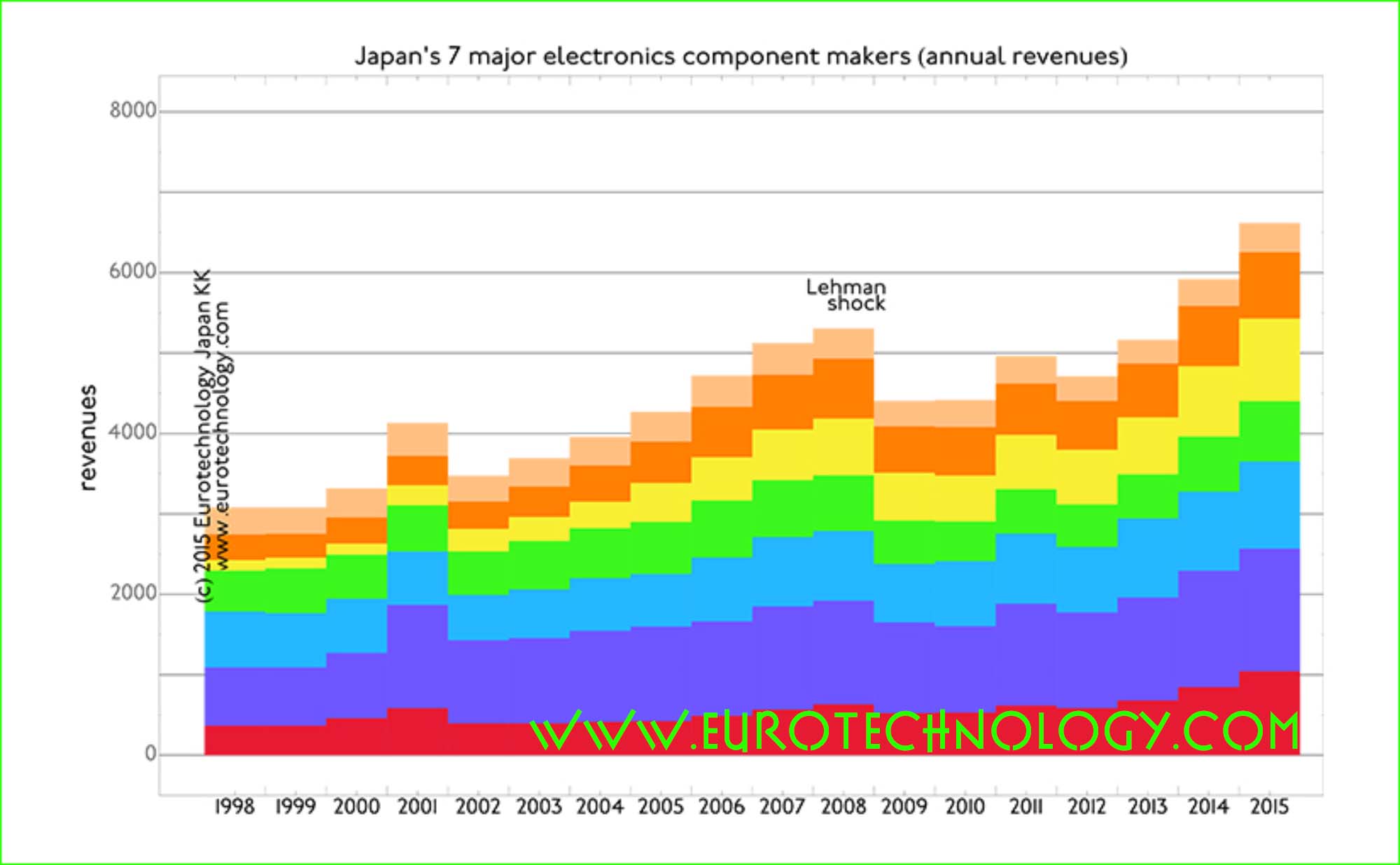

Japan’s electronics parts makers are a very different story: similar to The Netherlands, Japan’s top-7 electronic parts makers have grown to more than twice the size over the 17 years from FY1998 to FY2014. Some of the Japanese electronics parts makers have growth targets which should allow them to overtake Japan’s current incumbent electronics groups!

The stagnation of sales growth combined with almost zero profits over 17 years of Japan’s top 8 electronics groups, of which Toshiba is one, certainly puts much pressure on Japan’s electronics groups to improve performance. This pressure might be the background of accounting issues.

Lets look at the actual Toshiba financial data in detail

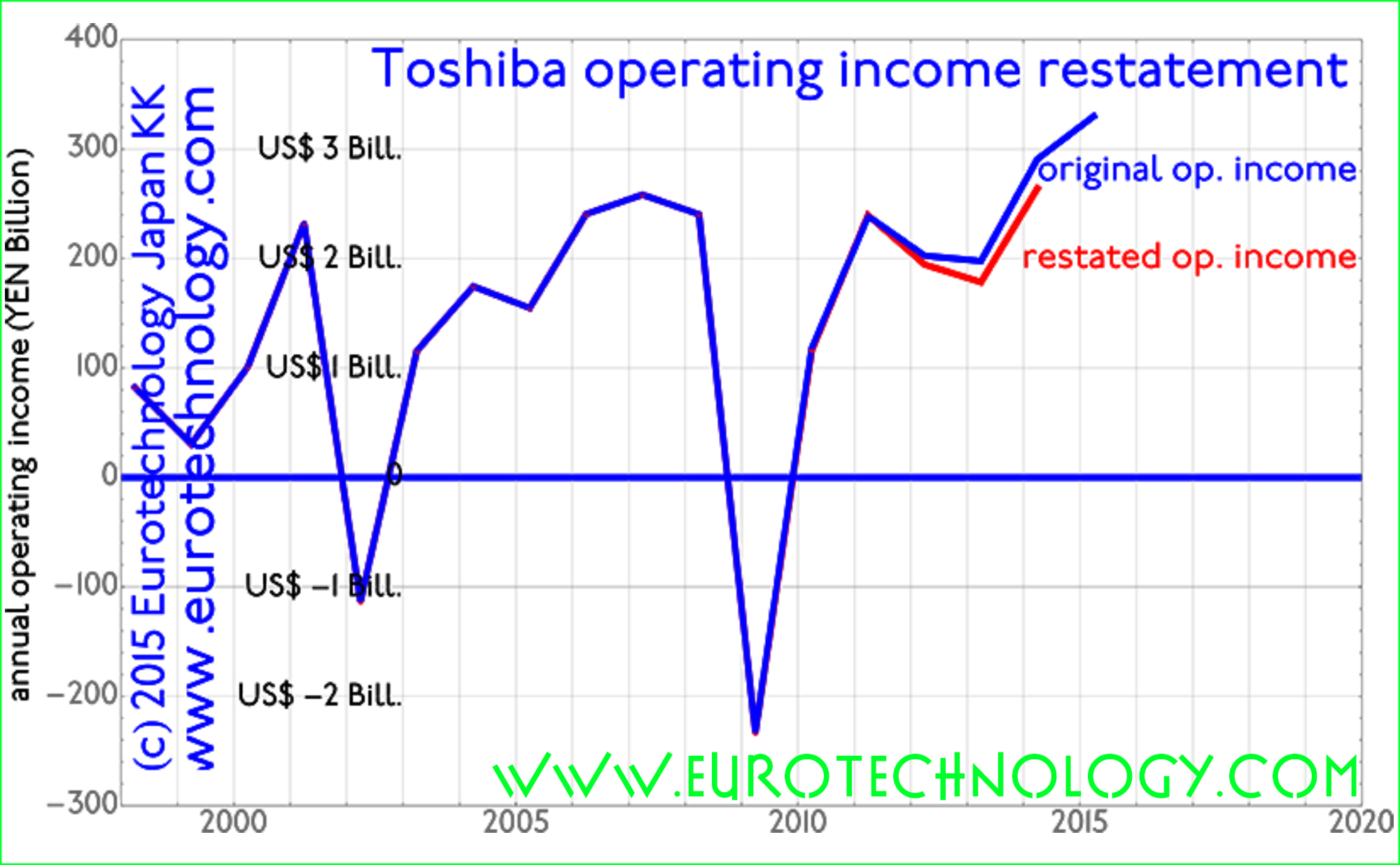

The figure below shows Toshiba’s previously reported operating income/profits (blue curve), and the recently announced preliminary corrections (red curve). The combined amount of downward corrections is about YEN 50 billion (US$ 0.5 billion) in total.

annual sales: approx. YEN 6000 billion (US$ 60 billion)

annual operating income (average over last 17 years): YEN 148 billion (US$ 1.5 billion)

annual net income (average over last 17 years): YEN 19 billion (US$ 190 million)

Therefore the downward correction corresponds to:

approx. 0.8% of average annual sales

approx. 33% of average annual operating profits

approx. 2 1/2 years (31.5 months) of net profits

Toshiba – typical for Japan’s large electronics corporations – operates with razor-thin profit margins: Toshiba’s net profit margin averaged over the last 17 years is 0.25%.

Therefore, the downward correction corresponds to 31.5 months of average net income/profits.

Toshiba accounting corrections amount to approx. 33% of average annual operating income

Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

Only with freedom and democracy, the values of open society and professionalism can the investment chain function effectively

Japan Exchange Group CEO Atsushi Saito: proud of Corporate Governance achievements, but ashamed of Toshiba

The iconic leader of the Tokyo Stock Exchange since 2007, now Group CEO of the Japan Exchange Group gave a Press Conference at the Foreign Correspondents Club of Japan on June 12, 2015, a few days before his retirement, to give an overview of his achievements and to review the status of Japan’s financial markets today.

Atsushi Saito expresses his satisfaction and pride and surprise about the big improvements in corporate governance and the mind change happening in Japan now.

Atsushi Saito has worked as equity analyst in the USA, experienced the US pension fund debate, and when he was pushing for reform of corporate governance in Japan around 1990 was ignored or even criticized. He is surprised to see that these changes he has been keeping pushing for since 1990 are actually implemented now.

Atsushi Saito directly expressed his shame about the accounting problems recently revealed at Toshiba, and contracts Hitachi, which has independent outsiders, women and non-Japanese foreigners on the Board of Directors, with Toshiba which has not. Atsushi Saito directly said: “I am very puzzled why Toshiba is so lazy to check their accounting”.

Atsushi Saito – leading the Tokyo Stock Exchange since 2007

Leading the Tokyo Stock Exchange since 2007, Atsushi Saito aspired to create an attractive investment destination in Tokyo for investors from all over the world with the following achievements:

modernized the trading systems

developed a self regulatory body

merge with Osaka to create Japan exchange group

Reform corporate governance to improve capital efficiency and corporate value of Japanese companies

The most imperative challenge has been left untouched for far too long: reform of corporate governance in Japan to improve capital efficiency and corporate value of Japanese companies.

Recently we introduced the Corporate Governance Code and we see a shift of mindset in Japanese companies.

Structural impediments remain remain in Japan’s financial market

Structural impediments remain remain in Japan’s financial markets, indirect finance from Banks remain a significant force in corporate finance.

Japanese investment bankers continue to fall way behind European and US rivals.

The post financial crisis regime under Basel 3 puts breaks on excessive leverage.

When global economy returns to high growth, we are not able to rely solely on money centered banks – banks will not be able to provide enough capital satisfy demands in a growing world economy.

Foresee demands for international organizations WorldBank, ADB and new AIIB and private equity funds.

With FinTec, we expect unbundling across separate financial service lines

With fintec, combining financial services and technology, we expect increasing unbundling across separate service lines for banking services, between settlement, wire transfers, loans and other services.

We will see more financial services.

Over dependence on main banks, risk aversion, lack of sense of duty by corporate managers led to the death of Japanese equity as an asset class

In Japan, as a consequence of dependence on indirect finance by money centric main banks, deep involvement of the main banks in corporate management, Japanese companies grew increasingly risk averse shied away from dynamic investment, and ultimately damaged corporate value.

There was a demise of the sense of duty by corporate managers use equity capital efficiently, and as a consequence of these factors, we saw a global divestment from Japanese stocks, eventually leading to the death of Japanese equity as an asset class.

Pushing since 1990 for reform of corporate governance in Japan, Atsushi Saito was not only ignored but even criticized

Atsushi Saito working as an equity analyst in the USA, followed the US pension debate, and started to push for reform of corporate governance in Japan around 1990, he was not only ignored but criticized.

Japan’s recent miraculous turn on corporate governance took Atsushi Saito by complete surprise

Today Japan addresses corporate governance, there is a miraculous turn of mindsets and regulatory framework. We saw:

amendment of companies act

corporate gov code

stewardship code

That these changes could happen came as a complete surprise.

Atsushi Saito hopes that this momentum can be maintained, and fiduciary duties of pension fund managers towards beneficiaries will be strengthened to nurture greater professionalism among Japanese institutional investors, similar to The Employee Retirement Income Security Act of 1974, or ERISA act in the USA.

Only with freedom and democracy + values of open society + professionalism can the investment chain function effectively

Only with freedom and democracy, the values of open society and professionalism can investment chain function effectively. This pattern is what defines truly advanced economy

The recent transformation has brought Japan back into the focus of professional investors globally and a new dawn beckons for Japan.

All stakeholders must remain focused to follow through these early signs of change to ensure that Japan welcomes a brighter future.

Questions and answers

Q: Japan not joining the Asian Infrastructure Investment Bank (AIIB) will deprive Japan of opportunities?

A: The Japanese Government did not say that it will not join the AIIB, but today there is no clear set of rules for the AIIB, the governance structure is unclear. To use tax payers money our government needs to be prudent before they make a decision on investment. There are about 20 international banks and similar organizations, 19 of them have clear governance rules. All except AIIB have clear governance rules. In case of AIIB China will have about 30% holding. Probably our Government will wait before making a decision, and Atsushi Saito thinks this is reasonable.

Q: Will Tokyo Stock Exchange enter into international alliance?

A: Stock Exchange business is a very nationalistic business – only USA has multiple exchanges. All other states have one single Exchange totally under control, regulations, culture by single states. Theoretically Exchanges between different countries can merge, but none succeeded. We saw no case in the world were Exchanges from different countries merged successfully, all such cooperations failed.

Q: Plans of Toyota to have non-traded convertable shares?

Its up to their shareholders. Legally they did not violate any rule.

Japan does not have any priority on special stocks.

I see a discrepance in the USA: The US aggressively raises the voice for rights of shareholders, and corporate governance elsewhere. At the same time US companies are the largest issuer of special stocks for special owners, e.g. for Google or Facebook, more than 50-60% of voting power is dominated by the founders of these companies. –

I see a discrepancy, its an ironical discrepancy. I am talking to the leaders of US : US is very nosy about our corporate goverance, protection of shareholders, but how do they protect shareholders of Google or Facebook?

Q: What is your advice for Japanese economy to regain vitality and energy, for Japan to become No. 1 in the world?

A: I am very concerned about efficient capital use and corporate governance. When I was securities analyst in USA, I was always asked about financial data of Japanese corporations.

Fuji Film had huge cash on the balance sheet – their competitor, the yellow-color photo company was always diligent with share holders, paid dividends, did share buy-backs. Fuji spent much R&D on pharmaceuticals and diversification. The Yellow color photo company disappeared, and Fuji Film is very healthy. Accumulation of sleeping capital is useless. But efficient use of capital is crucial.

when GM went bankrupt it was discovered that they had great technology, like electrical car projects which had been stopped. GM had stopped these R&D projects, because shareholders had insisted to stop R&D spending, and pay hire dividends, and ultimately went bankrupt.

Toyota had 3 trillion yen cash. This was heavily criticized. Toyota was secretely developing electric cars – now LEXUS electric car is bestseller in USA.

We are concerned to respect shareholders, but shareholders’ short term wishes are not always best for the company.

Even BlackRock wants long-term enterprise development rather than short term cash benefits.

Q: Impact of weak YEN on Stock Exchange

A: Even with weak yen, our trade balance is negative. Yen rate is not pushing export from Japan. Japan is manufacturing outside of Japan. Trade account is negative, capital account is black, currency account is black. Overseas subsidiaries are sending dividends back to Japan at the yen rate of 120. Its smart return in the capital account. Our industry structure has changed, we are not exporting on the back of weak yen, so we are not criticized.

Q: plans after retirement

A: I decided: no job – I will take rest.

Q: Disclosure. Often financial data are exposed early in Nikkei or Japanese press prior to official disclosure.

A: I am often asked about this. I don’t know how the press gets their information, its a free market for the press. As long as they don’t do any insider trading or use this information privately, I don’t see anything wrong with early public disclosure. Its a competitive issue between journalists, we cannot critisize competition among journalists. Very sharp journalists pick up information, we are not the police we cannot stop them. Its a competitive world – even for journalists.

I live far outside from Tokyo, sometimes journalists wait at the door to my home in the suburbs. I think this is an invasion of my privacy, and I don’t tell them information at my home.

Q: Trust in the stock market, low Japanese retail investor participation.

A: Advanced states have 60-70% own domestic investors, not outside foreign investors.

Foreign professional investors have immediately responded to the logic of our corporate governance reforms. Especially US and UK pension managers have immediately responded to the improved efficiency of our markets. Investment professionals in London, New York, Scotland can evaluate the meaning of our regulatory changes.

Japanese professional or private investors could not understand the improvements we have done, they did not react.

Mutual funds however are at record hights and we have 8 million ELISA private pension investments in Japan now. People start to build their own pensions now, so retail investors are coming into the market.

We have a normal quiet market now here in Japan regarding sales of equities.

Q: Tokyo as a financial center?

A: If you ask the same question to London, they will say that with IT all transactions are global. There may be arbitrage on the prices. If you compare Shanghai and NY, the trading volume in Shanghai is higher than in NY, but Shanghai not a global financial center, because they are not liberalized in capital in and outflow, they are No. 1 only in volume.

The definition of Financial Center of the World has changed.

We want to be one of the better places in financial business globally. We want to offer convenient and friendly conditions for financial people to come to Tokyo, as one of the centers for financial business.

Tax plays a very important role to define financial centers. London or NY or Tokyo cannot follow a city state like Singapore. We cannot have the same tax system. Tokyo is far bigger than Singapore.

“Global financial center” is a vague subject for me.

Q: Do current prices accurately reflect corp performance. Foreign investors: speculative short-term gains? will foreign investors pull out when Bank of Japan money flush ends?

A: I don’t think the Japanese market is overheating at all. I think the short term speculators have already left Japan.

Long term investors have long asked for change in Japan, Japan did not listen, but now for the first time Japan is listening and changing, and I am feeling longterm investors are understanding this change. We have long term investors here now in Japan.

Q: is high-frequency trading a danger for Stock Exchange?

A: Flash Crash in US was due to the diversity of exchanges. There are 50-60 markets in US. Flash Crash artificially made, not becaue of speed of trading.

Our rules for pricing system here in Japan, we learnt this since the Edo era, we cannot have flash crash, we limit the price changes, we are cooling the trading. Our system of pricing is different than in the USA.

We have many high-frequeny traders from abroad, and they appreciate our system. US high frequency traders critized us up to 10 years ago, but today they appreciate our pricing system here in Japan, they want to learn our Stock pricing system. This has really been a big change for us.

Q: False accounting at Toshiba. Impact on trust in Japan’s stock market.

A: I feel very ashamed for Toshiba. Toshiba should be the mentor or leader of Japanese industry – not the opposite.

Hitachi is a huge contrast to Toshiba. Hitachi aggressively introduced outside board members, foreign and women board members. Hitachi is investigated by outside and foreign board members.

Toshiba is a total contrast to Hitachi.

I am very puzzled by that – why is Toshiba so lazy to check their accounting.

We hope that auditors and accounting houses are more professional and more serious. They told us that their subsidiaries have different accounting system. They must have intentionally checked that point.

My answer: my feeling is one of shame. We should definitely not repeat this type of thing.

Q: Why do Japanese company accumulate so much cash reserves.

A: One reason is that Japanese labor laws compel Japanese companies to have reserves to pay for restructuring. We introduced changes in corp governance, and many companies now use the cash for M&A to acquire foreign companies, or e.g. Fanuc has increased dividends.

I am optimistic for Japanese companies, because they are using cash more efficiently now.

Japan’s electronics giants: as large as the economy of Holland, but 17 years of stagnation. No growth & no profits.

Daniel Loeb: SONY’s uninvited guest gives Japan’s business culture a jolt

Japan’s electronics giants combined are as large as the economy of Holland, but did not grow for about 17 years, and on average lost money all these years: no growth – no profits.

SONY abruptly created global headlines (e.g see New York Times), because US activist investor Daniel Loeb publicly encourages SONY’s CEO to speed up change. Mr Loeb’s Third Point LLC fund is SONY’s biggest shareholder at this time – surprising many, maybe even surprising SONY’s CEO, Mr Hirai. Mr Loeb’s encouragement was well timed: Mr Hirai’s will present SONY’s new strategy on May 22.

As we analyzed in our newsletter a few days ago and in more detail in our Electronic Industry Report, which was picked up by EE-Times and by the BBC, SONY recently earns its income, and offsets losses from the electronics and mobile phone businesses, mainly from asset sales and from subsidiary SONY-Finance – which sells life-insurance and credit cards. Therefore many believe that iconic SONY is undervalued, and needs much deeper and more fundamental change.

Japan’s iconic Big-8 electronics giants posses amazing technologies and engineers. However, their current situation is very much less than amazing, indicating huge opportunities. A few days ago the Big-8 all announced their results for FY2012, which ended on March 31, 2013 – lets look at the results together here.

long slow path to recovery for Japan’s “Big-8” electronics giants

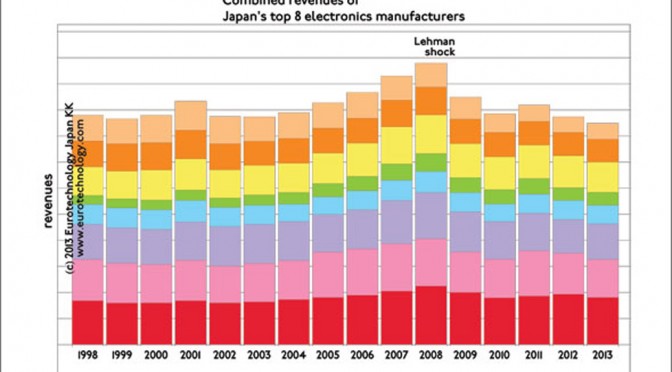

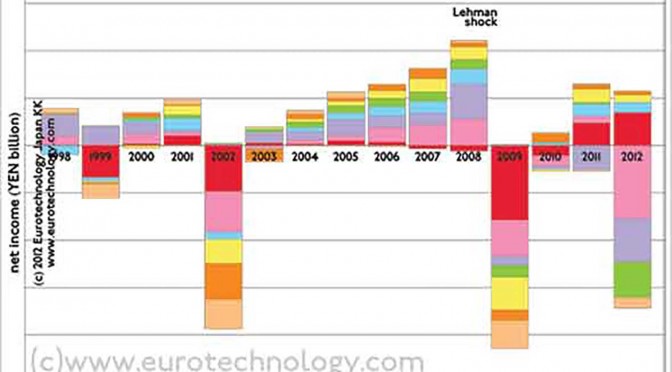

Japan’s electronics giants: Averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year

Subtracting losses from profits, and averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year (US$ 1 Billion losses/year)

For the last two financial years the Big-8 created net losses as follows:

Financial Year ended combined net losses

FY2012 March 31, 2013 YEN 1143 Billion (US$ 11 Billion)

FY2011 March 31, 2012 YEN 909 Billion (US$ 8.9 Billion)

Hitachi’s smart transformation

Hitachi’s smart transformation (find an overview in our report) indicates that change can bring rapid improvement.

Japan’s “Big-8” electronics makers combined are about the size of Holland’s economy – with one difference: Holland’s economy grows, but Japan’s electrical giants shrink and lose money at the same time

No growth

No growth: combined revenues of the Big-8 fell by YEN 1510 Billion (US$ 15 Billion) in the 15 years between FY1997 and FY2012 (assuming constant value YEN)

Many expect that “smart transformation” and globalization, and opening-up to the global society – combined maybe with a rejuvenation of “the Japanese model”, can release the potential for growth, which has been held back for 15 years.

In our electronic industry report we compare the Big-8 electronics companies with the Big-7 electronic parts manufacturers and show that their situation is much better, however the parts manufacturers face decreasing margins, also indicating the need for changing the business models and/or operations.

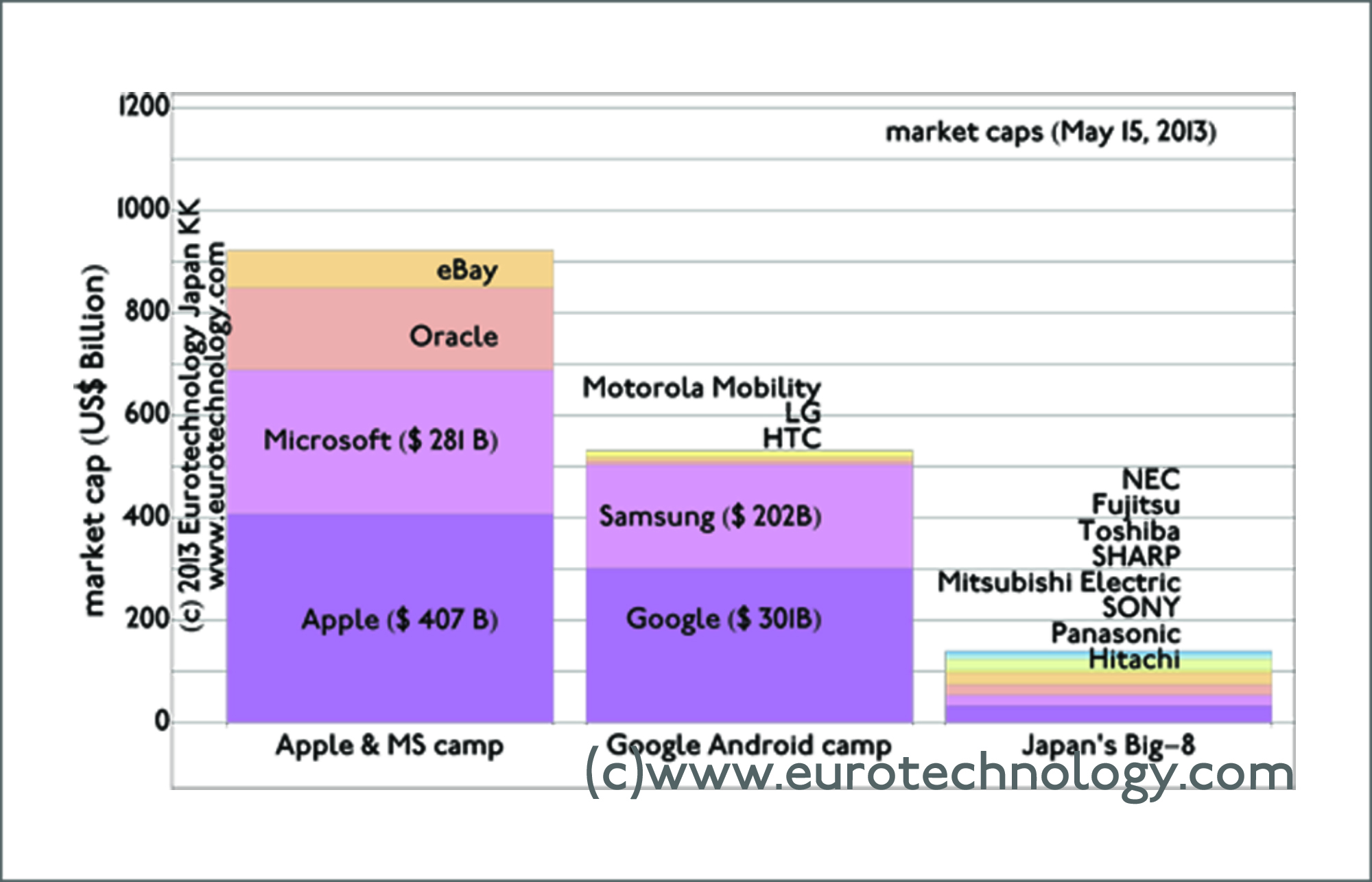

Japan’s “Big-8” may be seen as undervalued

Japan’s Big-8 electronics makers combined have far lower market capitalization than Apple, Microsoft, Google or Samsung

We produced the figure above for the presentation at the Foreign Correspondents Club in Tokyo about the “Apple-Samsung Patent War and Impact on Japans Industries”. We used the figure above to visualize the might of the Apple and Google/Samsung camps vs Japan’s Big-8 today. 15 years ago, the power of Apple vs Samsung vs Japan’s Big-8 was exactly opposite.

There is no reason why Japan’s electronics sector cannot regain global strength and value – IF absolutely necessary changes are made. This situation represents outstanding opportunities, which no doubt are attracting Mr Loeb and his Third Point fund, and others.

Understand Japan’s electronics sector: top 8 giants, and top electronic component makers

Study our report “Japan electronics industries: mono zukuri” (approx. 230 pages, pdf file)

Japan’s top 8 electronics companies combined are as large as the Netherlands economically, but have shown zero growth and zero income over the last 14 years – thus represent “sleeping giants” – or dinosaurs, depending on the point of view, and depending on whether these companies succeed to reinvent themselves.

We have updated our report on “Japan’s electronic manufacturers: mono zukuri” to analyze Japan’s electronics manufacturing sector, and to explain who the winners and who the losers are. Read a short summary in this newsletter below.

apan’s electronics companies combined are as large as Holland economically

Japan’s top electronics companies combined are as large as the Netherlands economically, but have not shown any revenue growth over the last 14 years

Japan’s electronics sector still today is largely guided by national industrial policy, and by the management principles created long ago by charismatic founders such as Matsushita and Ibuka.

Intellectual Japan: smart transformation at Hitachi led by the CEO and by the Chief Transformation Officer CTrO

Hitachi’s “Chief Transformation Officer” (“CTrO”) at a recent presentation, explained that until 2 years ago Hitachi benchmarked its financial data purely domestically – until 2 years ago, Hitachi only compared performance with competitors such as Panasonic and Toshiba.

Only 2 years ago, Hitachi started to benchmark performance with global competitors such as GE and Siemens.

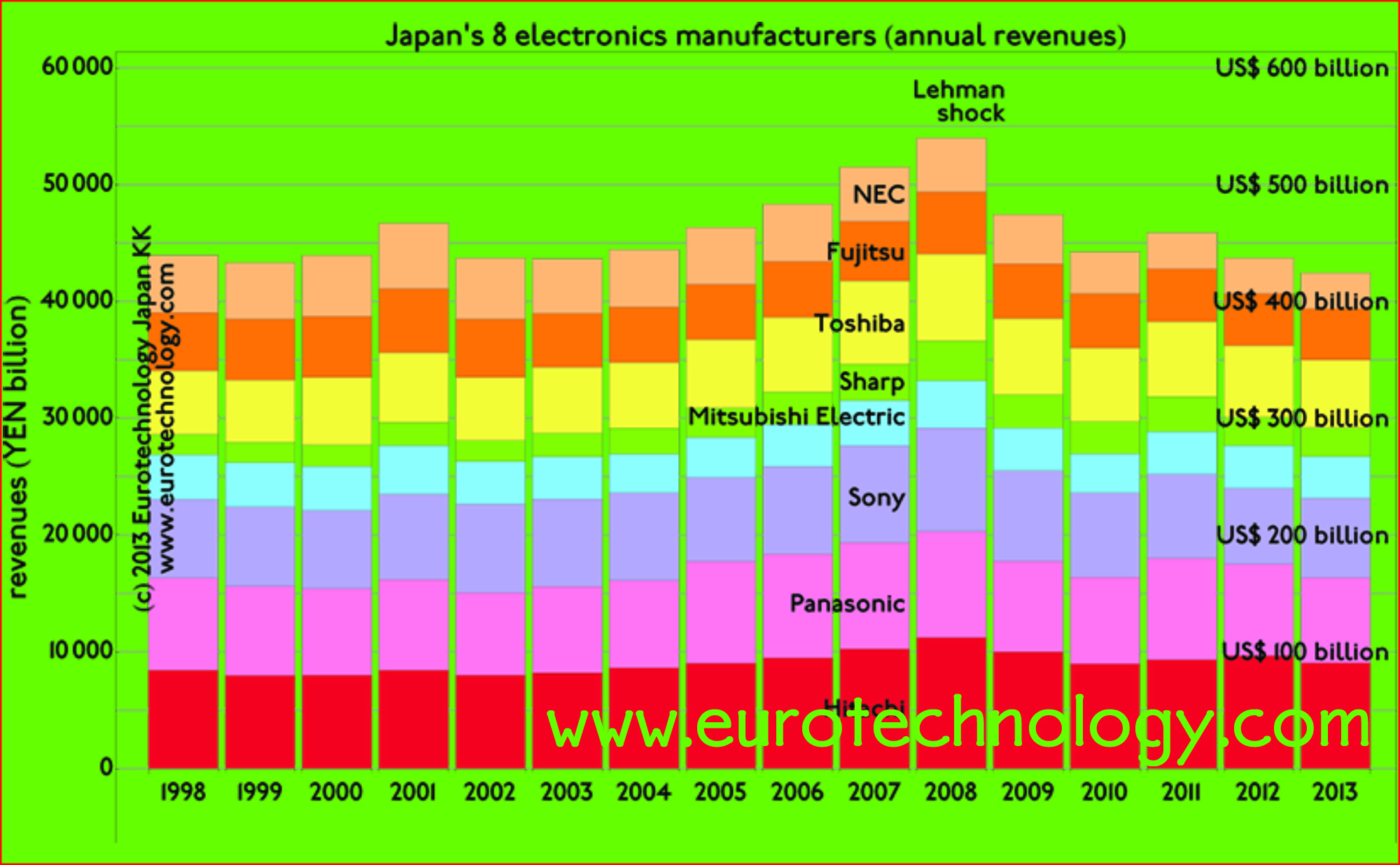

Japan’s top 8 electronics companies combined lose YEN 50 billion/year since 1998

Japan’s top 8 electronics companies lost an average of YEN 50 billion/year over the last 14 years

Intellectual Japan: electronic component makers

Japan’s electronics component makers, such as Kyocera or Murata, which is on the official supplier list of Apple, report positive income – although margins are declining and the component industry sector is much smaller than the top 8 electronics manufacturers.

Drastic transformation is necessary to revive Japan’s electronics industry sector. Drastic change will happen one way or another and represents important opportunities. More details in our electronics industry report

Over the last 15 years, their combined annual sales growth was zero, and their combined annual loss was YEN 50.6 billion/year (= US$ 0.6 billion/year).

Compelling evidence that new business models for Japan’s electronics sector present a huge opportunity – as explained in this BBC interview.

Sales growth of Japan’s “Big-8” electrical manufacturers vs top 7 electronics component makers

Contrasting Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC) with Japan’s 7 electronic parts makers (Murata, Kyocera, TDK, Alps, Nidec, Nitto, ROHM)

Over the last 14 years since FY1997, the combined growth in revenues (=sales) of Japan’s “Big-8” electronics groups was zero. The compound annual growth rate (CAGR) of Japan’s top 7 electronic parts makers combined was +3.1%.

Net income/losses of Japan’s “Big-8” electronics giants vs top-7 electronics components makers

Net income (profit) of Japan’s “Big-8” electronics groups vs top-7 electronics parts makers

Over the last 14 years since FY1997, Japan’s “Big-8” electronics groups combined showed average losses of YEN 50.6 billion/year (=US$ 0.6 billion/year), while Japan’s top 7 electronic parts makers combined earned YEN 196 billion/year (= US$ 2.4 billion/year).

Net income/losses of Japan’s top electrical groups

Net after tax income of Japan’s “Big-8” electronics groups

This figure shows net after tax income for Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC), for the years since FY1997. For 5 of these 14 years the industry sector reported combined losses, which in total exceeded the profits achieved in good years. As a result, averaged over all 14 years, the industry sector shows combined losses on the order of US$ 0.6 billion/year.

Creating new business models for this very large industry sector (of similar economic size as the Netherlands) is a huge opportunity.

et income/losses of Japan’s top-7 electronic component makers

Net income of Japan’s top 7 electronic parts makers

Japan’s top 7 electronic parts makers are in a much better financial situation than Japan’s electrical groups.

Over the last 14 years since FY1997, this industry sector only showed a net overall loss one single time – in the year following the Lehman shock, but showed combined net profits during all other years, resulting in average annual net profits on the order of US$ 2.4 billion/year.

BBC interview: “New business models for Japan’s electrical groups needed”

Why does it make sense to compare electronics giants with game companies? In many areas, especially home electronics and personal portable devices these two sectors compete for exactly the same consumer spending budgets and mind share.

We also take a look at specialist ROHM, which used to have outstanding margins because of the focus on highly specialized electrical and electronic components. ROHM’s shareholder proposals recently made headlines.

Germany based Siemens and Japanese giants Panasonic and Hitachi in the 1990s all had net margins close to zero. However, while Panasonic and Hitachi maintained their margins close to zero since the 1990s, Siemens clearly aims for US level margins – and achieved a slow and steady upward trend.

Very dramatic restructuring would be necessary to bring Japan’s electric giants onto such a path. I think it is quite obvious exactly which restructuring is necessary. I also believe that if carried out it will actually create more employment in Japan than maintaining the existing structure of Japan’s electrical industry sector. However, actually carrying such restructuring will require superhuman effort… will this happen?

Resistor maker ROHM

Rohm is another interesting story – and a fascinating Kyoto-culture company (with headquarters not so far from superstar Nintendo). Rohm was founded in 1958 by today’s CEO Sato Kenichiro to make resistors, and he later changed the name to R.ohm and then ROHM – today 80% of products are semiconductors. With increasing competition ROHM’s initially very high margins melted away. To counter the trend towards commoditization, ROHM invests heavily in R&D with technology centers around the world. Last week ROHM made global headlines: US fund Brandes had proposed a US$ 157 million share buy back, which was rejected at the shareholder meeting. Looking at ROHM’s margin over the years, its clear that action is required to bring margins again from today’s zero to the previous 20% level. I can sympathize with shareholders who think that a Shuji Nakamura / Nichia-type R&D breakthrough would be more likely to deliver such a comeback rather than a share buy back.

Note that not all shareholder proposals by US or European funds are rejected summarily at Japanese company shareholder meetings… some well prepared proposals have actually been accepted successfully.

Margins of Panasonic, Hitachi, Rohm with Siemens and GE

Starting from similar positions in the 1990s:

GE, Siemens, Hitachi and Panasonic all four had almost the same size in terms of annual sales back in the 1990s – today GE is twice the size of Hitachi or Siemens and 2.5 the size of Panasonic

Today, GE is about twice the size as Hitachi or Siemens, and about 2.5 the size of Panasonic. It seems that successful globalization is a necessary factor to achieve GE-style growth – necessary, but not sufficient… (see: our analysis of dramatic differences in globalization of Japan’s electric groups). The current crisis is a big opportunity for further growth by strong companies.

Revenue growth of Hitachi and Panasonic compared with SIEMENS and GE

Japan’s top 20 electronics companies combined are about as large as The Netherlands economically, and have big impact on the world economy. Our analysis shows how dramatically Japan’s electronics companies have been hit by the current crisis (except for Nintendo). We suggest that full recovery to 2008 (FY2007) levels may take until 2016 – about seven years in terms of income, and about 3-4 years in terms of revenues.

The crisis has thrown Japan’s electrical companies back to 2002 in terms of combined annual net incomes. It has taken Japanese electricals 7 years to climb from the 2002 crisis to the 2008 (FY2007) boom. Since Japan’s electrical companies have made relatively soft adjustments, but not a full fundamental industry restructuring yet, we think that it is likely that developments will proceed along a similar path as in the past: following such an analysis we think that it will take about 7 years from 2009 (ie. until 2016) for Japan’s electrical companies to work their way back up to 2008 net income levels. (Find detailed financial data and analysis in our report on Japan’s electronics industries)

net income of Japan’s electronics companies

Back to FY2003:

Combined annual sales for the financial year ending March 31, 2010, are at a similar level as in FY 2003, ie Japan’s electrical industry has been taken back 6 years in terms of revenue growth. Again, since a dramatic and fundamental industry restructuring has not yet taken place, we believe that we can expect it will take about 4 years for Japan’s electronics industry to grow again to 2008 (FY2007) size in terms of annual revenues.

net revenues of Japan’s electronics companies

The crisis spreads the field…

During the “good” years of FY1997 – FY2007 the differences between top and bottom performing electrical companies became steadily smaller: the field narrowed.

This figure shows that during the current crisis the spread between best and worst performing companies became more than twice as wide. The crisis clearly differentiates winners (Nintendo) from losers in terms of operating margins.

operating margins of Japan’s electronics companies