Will Abenomics succeed?

Stanford Economics Professor Takeo Hoshi thinks that there is a 10% chance that Abenomics will succeed to put Japan on a 2%-3% economic growth path, while the most likely outcome will be 1% economic growth. Read our notes of Professor Hoshi’s talk in detail here.

Can Japanese companies globalize?

“Globalization” of course is not an aim in itself. In Europe and USA there are plenty of companies which are very successful and not globalized. However, Japan could capture much more global value from technology and creativity by creating more global companies: the shining example is SoftBank.

When four experts including myself briefed the President of Germany about Japan, we all agreed on Japan’s extraordinary creativity. At the same time there are many difficulties for Japan to capture global value from this creativity.

Read legendary Masamoto Yashiro’s viewpoints about globalization at a recent Tokyo University brainstorming event by the President of Tokyo University (Masamoto Yashiro was Chairman of Exxon-Japan, of Citibank-Japan, and Shinsei-Bank, and Board Member of the Construction Bank of China). Masamoto Yashiro says that a change of mind-set is urgently needed.

Overseas direct investment is one way for Japanese companies to globalize. Japanese companies have been investing strongly in EU, just a few days ago Sompo Insurance/ NKSJ Holdings acquired the UK Canopius Group for about US$ 1 billion.

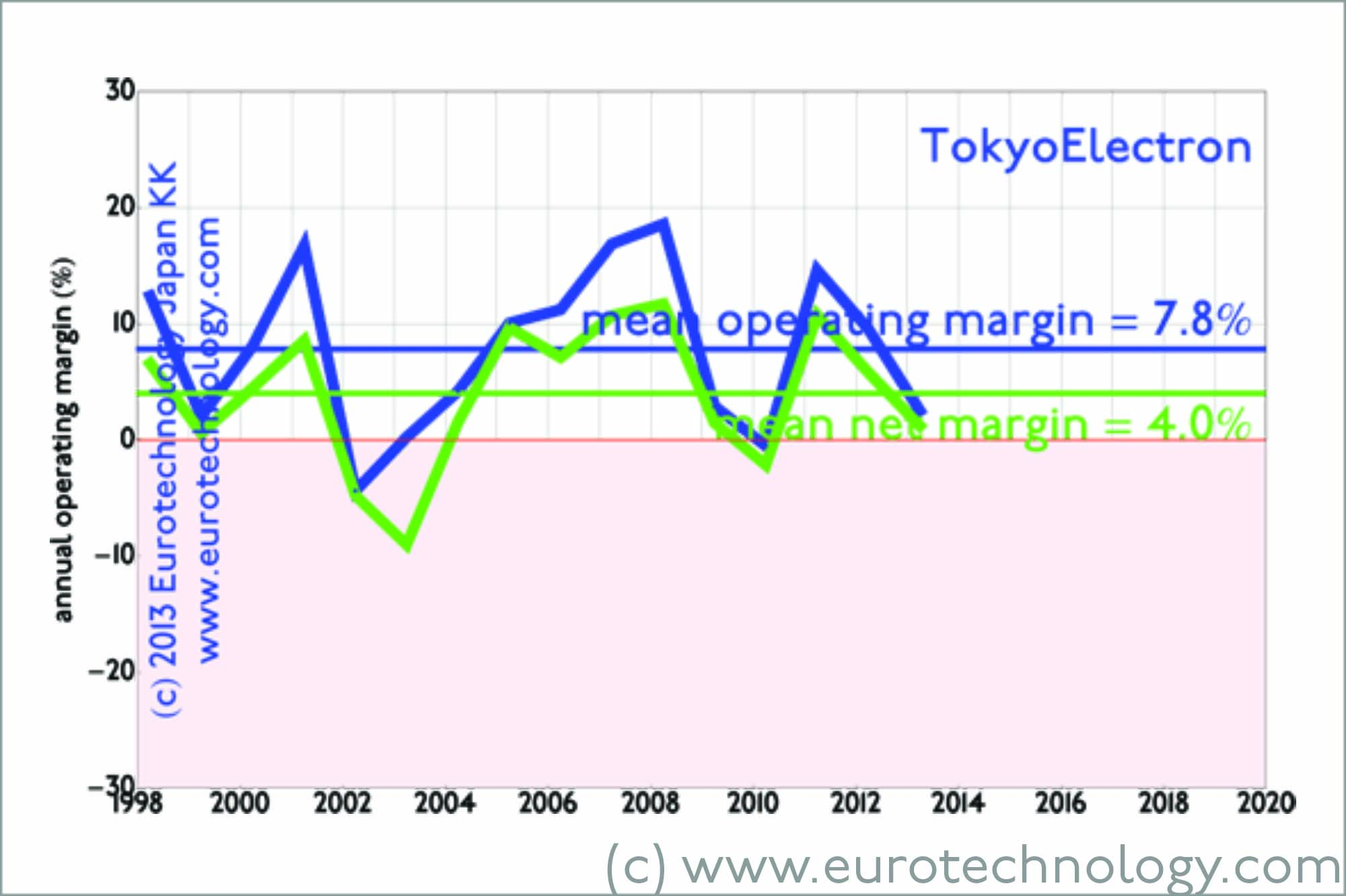

Other recent mergers globalizing Japan are, TowerJazz acquiring three Panasonic IC fabs, and the merger of Applied Materials and Tokyo Electron, another is GungHo and SoftBank investing in SuperCell, and GungHo has now been even floating the idea of moving corporate headquarters to Finland!

Disruption for Japan’s Energy markets

Until March 11, 2011, Japan’s energy markets were essentially frozen in the structures created in 1952, which again resulted from the war-time nationalization of Japan’s electricity sector (see our Energy Report). Japan’s electricity markets alone are worth about US$ 200 million per year – and this market is now in disruption.

Recently I was invited to brief the Energy Minister of Canada, Mr Joe Oliver, and Sweden’s Trade Minister Dr. Ewa Björling about Japan’s energy markets. My briefings are based on our analysis, which you can find in our Energy Report, and Renewable Energy Report.

The liberalization of Japan’s energy markets will create winners and losers – comparing the financial performance of Japan’s electricity companies and gas companies is an indication of things to come. Actually, only Japan’s electricity markets are being liberalized currently, liberalization of Japan’s gas markets is still for the future.

Disrupting Japan’s game sector

Japan’s game makers have essentially created the global game market, and are ripe for disruption by smart phones and tablets one would think. Indeed, just three Japanese newcomers Gree + DeNA + GungHo alone (there are many more) create more annual net income than Japan’s top 9 game makers combined! The origin of this disruption by newcomers in Japan however is not created by Western companies, and not by smart phones, but goes back to the creation of i-Mode in February 1999 (and some months later EZweb and Jsky). Recently the world is slowly waking up to the fact, that Japan’s game markets is one of the world’s biggest, if not the biggest… and hard for foreign companies to penetrate, unless done correctly…

We wish you a very Happy New Year!

Copyright 2013 Eurotechnology Japan KK All Rights Reserved