Japan’s iconic electronics groups combined are of similar size as the economy of The Netherlands

Parts makers’ sales may overtake iconic electronics groups in the near future – they have already in terms of profits

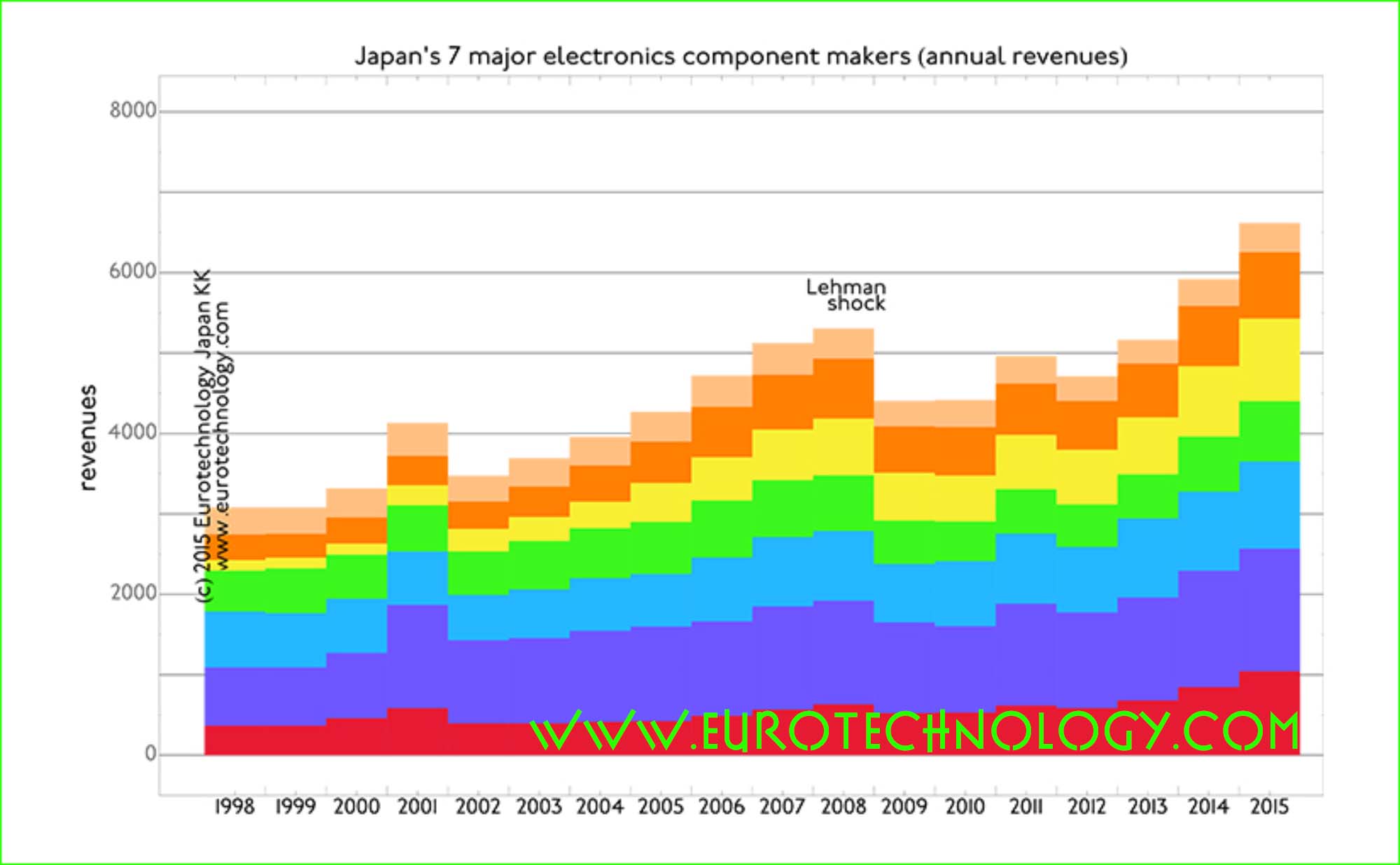

In our analysis of Japan’s electronic industries we compare the top 8 iconic electronics groups with top 7 electronics parts makers over the period FY1998 to FY2014, which ended March 31, 2015 for most Japanese companies. Except for Toshiba, all Japanese major electronics companies have now officially reported their FY2014 results.

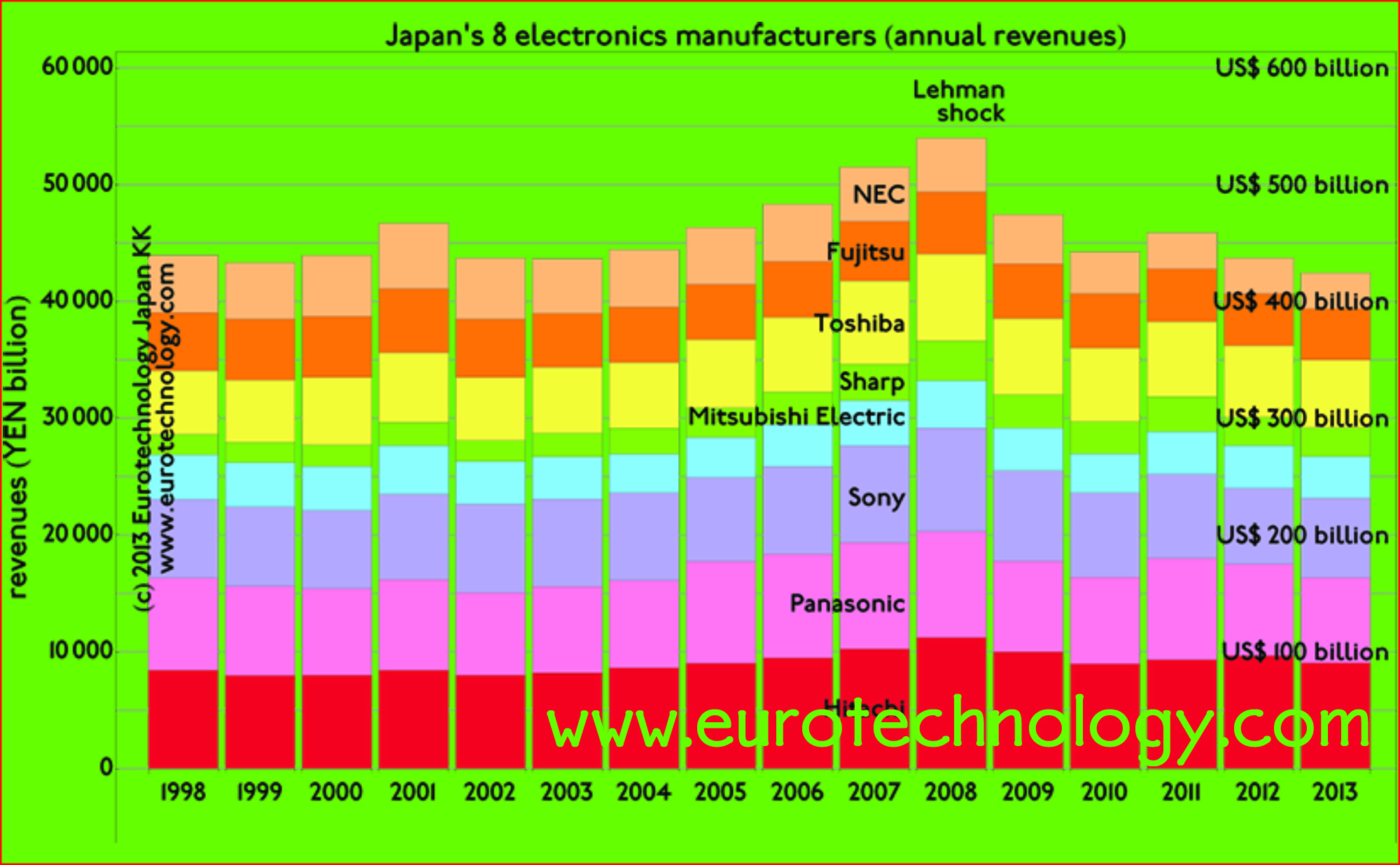

Japan’s iconic 8 electronics groups (Hitachi, Toshiba, Panasonic, Fujitsu, Mitsubishi Electric, NEC, SONY and SHARP) combined are as large as the economy of The Netherlands – but while the economy of The Netherlands doubled in size between 1998 and 2015, the sales/revenues of Japan’s iconic 8 electronics groups combined showed almost zero growth (annual compound growth rate = 0.4%) and almost zero income (profits).

Japan’s top 7 electronics parts makers on the other hand – similar to the Netherlands – more than doubled their combined revenues (sales) over the 17 years from FY1998 to FY2014, and earned healthy and increasing profits.

While several of Japan’s iconic electronics groups are fighting for survival, Japan’s parts makers have very ambitious growth plans – some of them may well overtake the traditional electronics conglomerates in sales – they have already in terms of profits. And they aggressively acquire around the world.

Detailed data and analysis in our Report on Japan’s electronics sector

Japan’s electronics giants: as large as the economy of Holland, but 17 years of stagnation. No growth & no profits.

Daniel Loeb: SONY’s uninvited guest gives Japan’s business culture a jolt

Japan’s electronics giants combined are as large as the economy of Holland, but did not grow for about 17 years, and on average lost money all these years: no growth – no profits.

SONY abruptly created global headlines (e.g see New York Times), because US activist investor Daniel Loeb publicly encourages SONY’s CEO to speed up change. Mr Loeb’s Third Point LLC fund is SONY’s biggest shareholder at this time – surprising many, maybe even surprising SONY’s CEO, Mr Hirai. Mr Loeb’s encouragement was well timed: Mr Hirai’s will present SONY’s new strategy on May 22.

As we analyzed in our newsletter a few days ago and in more detail in our Electronic Industry Report, which was picked up by EE-Times and by the BBC, SONY recently earns its income, and offsets losses from the electronics and mobile phone businesses, mainly from asset sales and from subsidiary SONY-Finance – which sells life-insurance and credit cards. Therefore many believe that iconic SONY is undervalued, and needs much deeper and more fundamental change.

Japan’s iconic Big-8 electronics giants posses amazing technologies and engineers. However, their current situation is very much less than amazing, indicating huge opportunities. A few days ago the Big-8 all announced their results for FY2012, which ended on March 31, 2013 – lets look at the results together here.

long slow path to recovery for Japan’s “Big-8” electronics giants

Japan’s electronics giants: Averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year

Subtracting losses from profits, and averaged over the last 15 years, Japan’s Big-8 created net losses of YEN 104 billion/year (US$ 1 Billion losses/year)

For the last two financial years the Big-8 created net losses as follows:

Financial Year ended combined net losses

FY2012 March 31, 2013 YEN 1143 Billion (US$ 11 Billion)

FY2011 March 31, 2012 YEN 909 Billion (US$ 8.9 Billion)

Hitachi’s smart transformation

Hitachi’s smart transformation (find an overview in our report) indicates that change can bring rapid improvement.

Japan’s “Big-8” electronics makers combined are about the size of Holland’s economy – with one difference: Holland’s economy grows, but Japan’s electrical giants shrink and lose money at the same time

No growth

No growth: combined revenues of the Big-8 fell by YEN 1510 Billion (US$ 15 Billion) in the 15 years between FY1997 and FY2012 (assuming constant value YEN)

Many expect that “smart transformation” and globalization, and opening-up to the global society – combined maybe with a rejuvenation of “the Japanese model”, can release the potential for growth, which has been held back for 15 years.

In our electronic industry report we compare the Big-8 electronics companies with the Big-7 electronic parts manufacturers and show that their situation is much better, however the parts manufacturers face decreasing margins, also indicating the need for changing the business models and/or operations.

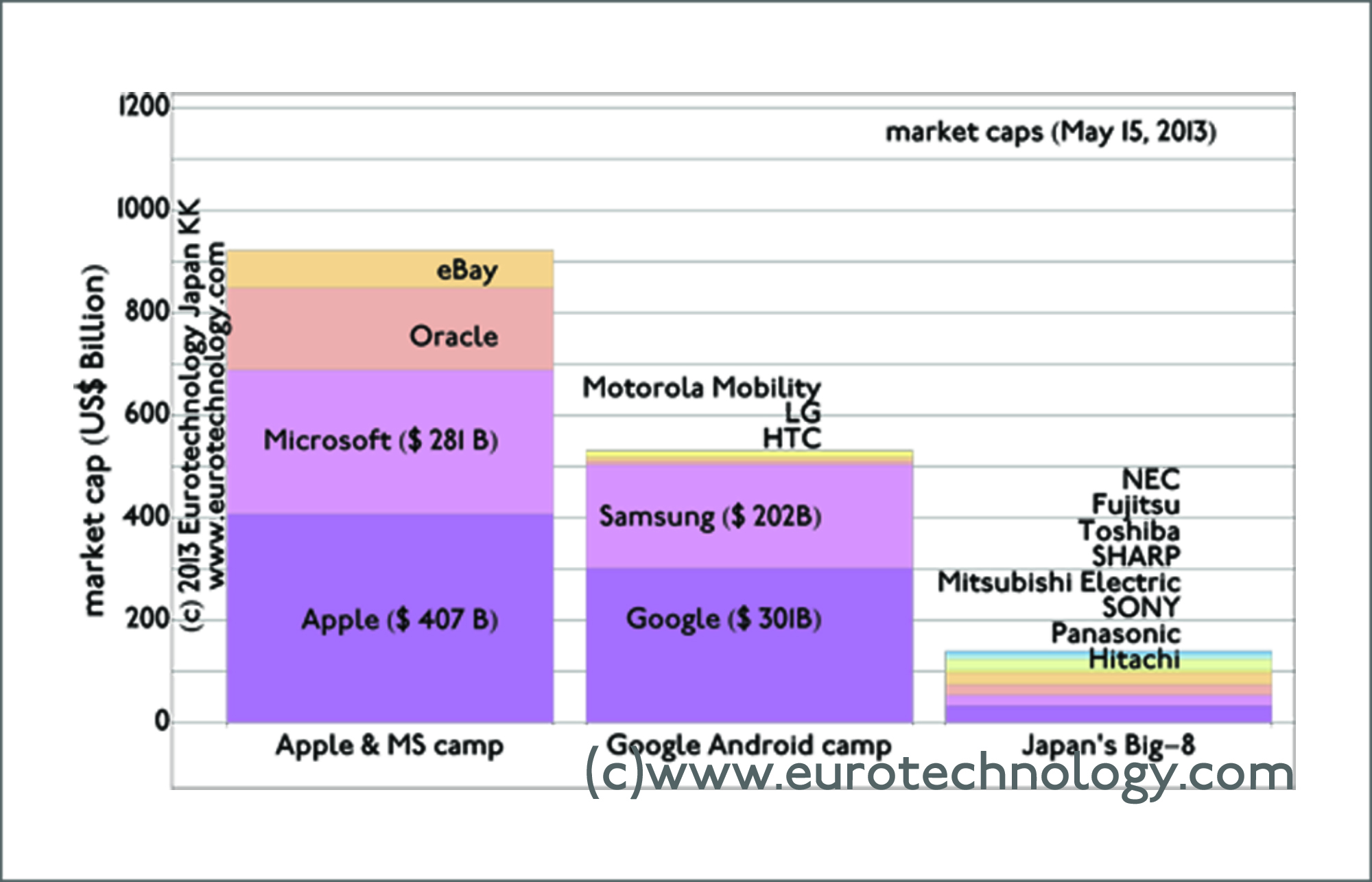

Japan’s “Big-8” may be seen as undervalued

Japan’s Big-8 electronics makers combined have far lower market capitalization than Apple, Microsoft, Google or Samsung

We produced the figure above for the presentation at the Foreign Correspondents Club in Tokyo about the “Apple-Samsung Patent War and Impact on Japans Industries”. We used the figure above to visualize the might of the Apple and Google/Samsung camps vs Japan’s Big-8 today. 15 years ago, the power of Apple vs Samsung vs Japan’s Big-8 was exactly opposite.

There is no reason why Japan’s electronics sector cannot regain global strength and value – IF absolutely necessary changes are made. This situation represents outstanding opportunities, which no doubt are attracting Mr Loeb and his Third Point fund, and others.

Understand Japan’s electronics sector: top 8 giants, and top electronic component makers

Study our report “Japan electronics industries: mono zukuri” (approx. 230 pages, pdf file)

Japan’s top 8 electronics companies combined are as large as the Netherlands economically, but have shown zero growth and zero income over the last 14 years – thus represent “sleeping giants” – or dinosaurs, depending on the point of view, and depending on whether these companies succeed to reinvent themselves.

We have updated our report on “Japan’s electronic manufacturers: mono zukuri” to analyze Japan’s electronics manufacturing sector, and to explain who the winners and who the losers are. Read a short summary in this newsletter below.

apan’s electronics companies combined are as large as Holland economically

Japan’s top electronics companies combined are as large as the Netherlands economically, but have not shown any revenue growth over the last 14 years

Japan’s electronics sector still today is largely guided by national industrial policy, and by the management principles created long ago by charismatic founders such as Matsushita and Ibuka.

Intellectual Japan: smart transformation at Hitachi led by the CEO and by the Chief Transformation Officer CTrO

Hitachi’s “Chief Transformation Officer” (“CTrO”) at a recent presentation, explained that until 2 years ago Hitachi benchmarked its financial data purely domestically – until 2 years ago, Hitachi only compared performance with competitors such as Panasonic and Toshiba.

Only 2 years ago, Hitachi started to benchmark performance with global competitors such as GE and Siemens.

Japan’s top 8 electronics companies combined lose YEN 50 billion/year since 1998

Japan’s top 8 electronics companies lost an average of YEN 50 billion/year over the last 14 years

Intellectual Japan: electronic component makers

Japan’s electronics component makers, such as Kyocera or Murata, which is on the official supplier list of Apple, report positive income – although margins are declining and the component industry sector is much smaller than the top 8 electronics manufacturers.

Drastic transformation is necessary to revive Japan’s electronics industry sector. Drastic change will happen one way or another and represents important opportunities. More details in our electronics industry report

Over the last 15 years, their combined annual sales growth was zero, and their combined annual loss was YEN 50.6 billion/year (= US$ 0.6 billion/year).

Compelling evidence that new business models for Japan’s electronics sector present a huge opportunity – as explained in this BBC interview.

Sales growth of Japan’s “Big-8” electrical manufacturers vs top 7 electronics component makers

Contrasting Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC) with Japan’s 7 electronic parts makers (Murata, Kyocera, TDK, Alps, Nidec, Nitto, ROHM)

Over the last 14 years since FY1997, the combined growth in revenues (=sales) of Japan’s “Big-8” electronics groups was zero. The compound annual growth rate (CAGR) of Japan’s top 7 electronic parts makers combined was +3.1%.

Net income/losses of Japan’s “Big-8” electronics giants vs top-7 electronics components makers

Net income (profit) of Japan’s “Big-8” electronics groups vs top-7 electronics parts makers

Over the last 14 years since FY1997, Japan’s “Big-8” electronics groups combined showed average losses of YEN 50.6 billion/year (=US$ 0.6 billion/year), while Japan’s top 7 electronic parts makers combined earned YEN 196 billion/year (= US$ 2.4 billion/year).

Net income/losses of Japan’s top electrical groups

Net after tax income of Japan’s “Big-8” electronics groups

This figure shows net after tax income for Japan’s “Big-8” electronics groups (Hitachi, Panasonic, Sony, Mitsubishi-Electric, Sharp, Toshiba, Fujitsu, NEC), for the years since FY1997. For 5 of these 14 years the industry sector reported combined losses, which in total exceeded the profits achieved in good years. As a result, averaged over all 14 years, the industry sector shows combined losses on the order of US$ 0.6 billion/year.

Creating new business models for this very large industry sector (of similar economic size as the Netherlands) is a huge opportunity.

et income/losses of Japan’s top-7 electronic component makers

Net income of Japan’s top 7 electronic parts makers

Japan’s top 7 electronic parts makers are in a much better financial situation than Japan’s electrical groups.

Over the last 14 years since FY1997, this industry sector only showed a net overall loss one single time – in the year following the Lehman shock, but showed combined net profits during all other years, resulting in average annual net profits on the order of US$ 2.4 billion/year.

BBC interview: “New business models for Japan’s electrical groups needed”

We also take a look at specialist ROHM, which used to have outstanding margins because of the focus on highly specialized electrical and electronic components. ROHM’s shareholder proposals recently made headlines.

Germany based Siemens and Japanese giants Panasonic and Hitachi in the 1990s all had net margins close to zero. However, while Panasonic and Hitachi maintained their margins close to zero since the 1990s, Siemens clearly aims for US level margins – and achieved a slow and steady upward trend.

Very dramatic restructuring would be necessary to bring Japan’s electric giants onto such a path. I think it is quite obvious exactly which restructuring is necessary. I also believe that if carried out it will actually create more employment in Japan than maintaining the existing structure of Japan’s electrical industry sector. However, actually carrying such restructuring will require superhuman effort… will this happen?

Resistor maker ROHM

Rohm is another interesting story – and a fascinating Kyoto-culture company (with headquarters not so far from superstar Nintendo). Rohm was founded in 1958 by today’s CEO Sato Kenichiro to make resistors, and he later changed the name to R.ohm and then ROHM – today 80% of products are semiconductors. With increasing competition ROHM’s initially very high margins melted away. To counter the trend towards commoditization, ROHM invests heavily in R&D with technology centers around the world. Last week ROHM made global headlines: US fund Brandes had proposed a US$ 157 million share buy back, which was rejected at the shareholder meeting. Looking at ROHM’s margin over the years, its clear that action is required to bring margins again from today’s zero to the previous 20% level. I can sympathize with shareholders who think that a Shuji Nakamura / Nichia-type R&D breakthrough would be more likely to deliver such a comeback rather than a share buy back.

Note that not all shareholder proposals by US or European funds are rejected summarily at Japanese company shareholder meetings… some well prepared proposals have actually been accepted successfully.

Margins of Panasonic, Hitachi, Rohm with Siemens and GE

Starting from similar positions in the 1990s:

GE, Siemens, Hitachi and Panasonic all four had almost the same size in terms of annual sales back in the 1990s – today GE is twice the size of Hitachi or Siemens and 2.5 the size of Panasonic

Today, GE is about twice the size as Hitachi or Siemens, and about 2.5 the size of Panasonic. It seems that successful globalization is a necessary factor to achieve GE-style growth – necessary, but not sufficient… (see: our analysis of dramatic differences in globalization of Japan’s electric groups). The current crisis is a big opportunity for further growth by strong companies.

Revenue growth of Hitachi and Panasonic compared with SIEMENS and GE