Global No. 1 (Applied Materials) and No. 3 (Tokyo Electron) plan merger

Subject to regulatory approval in different jurisdictions

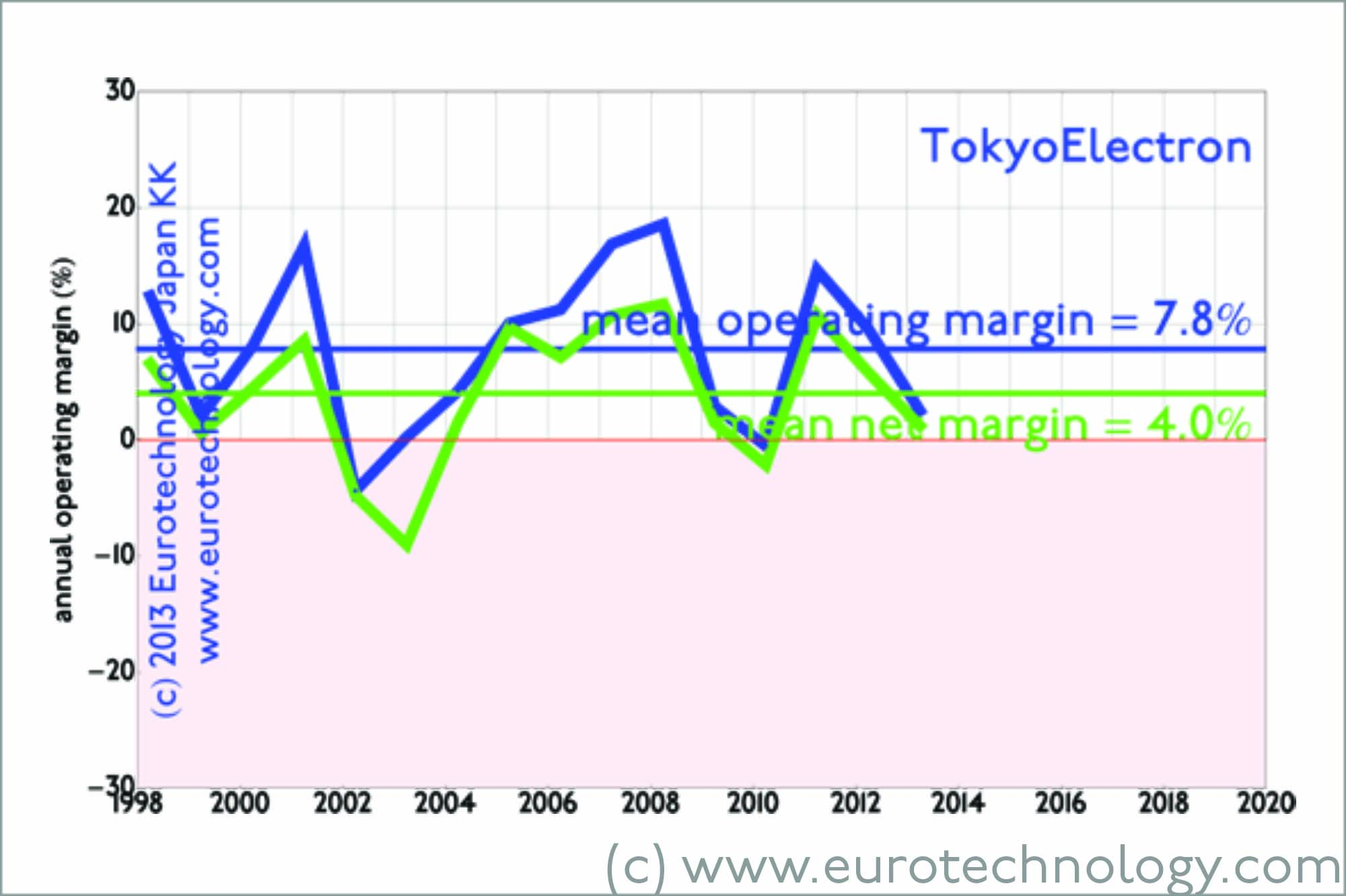

Global No. 1 (Applied Materials) and No. 3 (Tokyo Electron) semiconductor manufacturing equipment makers on September 24, 2013 announced their “merger of equals” – creating a company with a nominal market capitalization of US$ 31.5 Billion, in one of the largest mergers of a Japanese company with a foreign company ever. I was this morning interviewed by BBC to comment – here additional background material and comments.

Summary of the Tokyo Electron & Applied Materials merger:

A new company will be created:

- combined market capitalization of US$ 31 billion and about 24% market share

- dual headquarters in Tokyo and Santa Clara, incorporated in The Netherlands

- Chairman=Tetsuro Higashi (Tokyo Electron)

- CEO=Gary Dickerson (Applied Materials)

- CFO=Bob Halliday (Applied Materials)

- ownership – corresponds almost exactly to the market capitalization ratio:

- 68% Applied Materials shareholders

- 32% Tokyo Electron shareholders

Anti-trust approval still outstanding:

Anti-trust authorities in several jurisdictions are likely to examine this planned merger, however it seems likely that there will be no major problems, since the product portfolios of both companies are quite complementary.

Currently Applied Materials has about 14% market share of semiconductor manufacturing equipment and Tokyo electron about 10%, thus about 76% of the market are supplied by competitors.

Of course the “pricing power” of the combined company could increase in certain cases, which could be also a driving force for this merger.

Market shares of IC manufacturing equipment market pre merger

- Applied Materials: US$ 5.5 billion (14.4%)

- ASML: US$ 4.9 billion (12.8%)

- Tokyo Electron: US$ 4.2 billion (11.1%)

- Lam Research: US$ 2.8 billion (7.4%)

- KLA-Tencor: US$ 2.5 billion (6.5%)

Market shares of IC manufacturing equipment market post merger

- Applied Materials + Tokyo Electron: US$ 9.7 billion (25.5%)

- ASML: US$ 4.9 billion (12.8%)

- Lam Research: US$ 2.8 billion (7.4%)

- KLA-Tencor: US$ 2.5 billion (6.5%)

“Merger of equals” – really?:

Yes and no. Ownership of the merged company is split between shareholders of Applied Materials (68%) and Tokyo Electron (32%) according to current market capitalization ratio, and both CEO and CFO will be from Applied Materials. This is a clear message to Japanese corporations that market capitalization does matter dramatically. As we have shown in previous posts, the market capitalization of Japanese electronics companies today is dramatically low (considering revenue size, the glorious past and future potential) – so in any similar merger “of equals” even Japanese electronics giants could be the junior partner. This point was also addressed in a recent presentation by Hiroshi Mikitani. These sensitive issues were extremely skillfully and successfully handled by Renault and Nissan. Carlos Ghosn has said in this context that he believes a full acquisition would not have been successful.

“One of the largest mergers between a Japanese and a foreign company” – if executed and successful

There is some confusion on this point in the news articles that I have seen. The current market capitalization of Tokyo Electron is approx. US$ 10.07 billion.

By far the largest acquisition of a Japanese company by a foreign company was the acquisition of the Japan Telecom Group by Vodafone. Since this acquisition was done (and later undone) by a large number of separate transactions, it is difficult to put a specific size on this acquisition. Our estimation is that this acquisition was on the order of US$ 20 billion or higher – and was not successful longterm, some reasons are outlined here.

Large scale acquisitions of Japanese companies by foreign companies include:

- Japan Telecom Group acquisition by Vodafone (undone: now part of SoftBank)

- Nikko Cordial acquisition by Citigroup (undone: now SMBC-Nikko)

- Japan Leasing acquired by GE

- Nissan Motor partnership with Renault (minority stake, not acquisition)

Applied Materials and Tokyo Electron – Tax:

Tokyo Electron + Applied Materials plan a joint holding company in The Netherlands. One reason is to have a neutral location following the spirit of “merger of equals”, but tax also plays a role:

- Projected tax rate for new holding company on profits in The Netherlands: 17%

- Current tax rate on profits for Applied Materials: 28%

- Current tax rate on profits for Tokyo Electron: 37%

Applied Materials and Tokyo Electron – Cultural issues:

Not to be underestimated. In our view success of this merger is not guaranteed at all, and will depend to some extent to skillful management of the bridging cultural issues.

Our report on Japan’s electronics industries – mono zukuri:

pdf file, approx. 235 pages, 100 figures

Copyright (c) 2013 Eurotechnology Japan KK All Rights Reserved